Clicks Beat Bricks in This Hot Sector

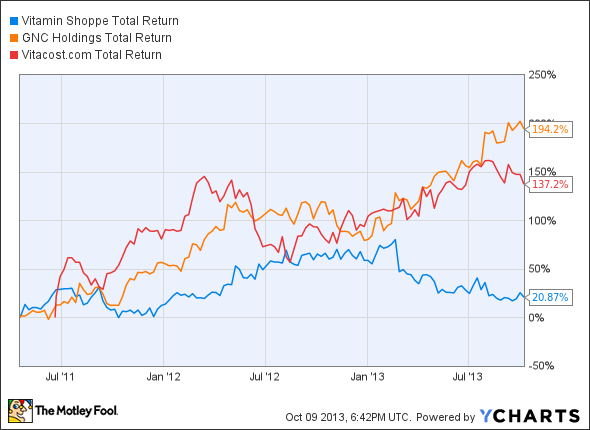

The health and wellness rising tide is lifting all supplement companies these days with 64% of Americans downing vitamins. But there's one simple reason that Vitacost.com (NASDAQ: VITC), and GNC Holdings (NYSE: GNC)have both surged so much higher than rival Vitamin Shoppe (NYSE:VSI). In a word, e-commerce.

VSI Total Return Price data by YCharts

Clicks beat bricks

Small cap Vitacost.com is an online retailer of health and wellness products in North America with 44,000 plus stock keeping units, or SKUs, and 1.8 million active customers.

It is still finding its way between promotional activity to attract customers and raising gross margin. In its second quarter, it gained 247,000 new customers at the cost of 150 basis points year-over-year and 80 basis points for the quarter. Vitacost.com's gross margin now stands at 22.3%.

International sales grew 97% and inventory decreased as the company experienced quicker turnover thanks to fulfillment center improvements. Revenue and active customer base compound annual growth rates since 2007 are 27% and 30% respectively.

Vitacost.com doesn't consider GNC a rival, as it has 11 times the number of SKUs, although it does actually compete against GNC's LuckyVitamin.com. Going forward the company is increasing its higher margin proprietary product line; the ratio now stands at 78% third party and 22% proprietary. It has also started bundling similar products to increase e-basket total ticket.

Growing its clicks

GNC, a health and wellness retailer, has 6,200 US retail locations and franchise operations in 55 countries for a total of 8,200 locations.

It may have a lot of bricks but it's rapidly growing clicks with its 2011 LuckyVitamin.com purchase. The buy is already paying off with $56 million in revenue for 2012.Expanding GNC's global online footprint is one step closer with this October's acquisition of UK based Discount Supplements, a nutritional e-tailer. Discount Supplements brings with it one third of UK health and wellness online market share.

Bricks aren't doing badly, either. All three GNC operating segments: manufacturing/wholesale, retail, and franchise saw double digit gains in revenues in 2012 for total 2012 revenue of $2.43 billion, a 17.3% increase.

At the Goldman Sachs Global Retailing Conference the company boasted about deleveraging debt from a net debt/ adjusted EBITDA ratio of 6.1x in 2007 to 2.0x by 2012. Other highlights presented were 30 consecutive quarters of comp sales growth, a compound annual growth rate of 10.7% for consolidated revenue, and 23.3% growth for cumulative EBITDA since 2005.

GNC offers a 1.10% yield at a 20% payout ratio.The company bought back $181 million worth of shares so far this year and generated $104.2 million in free cash flow in the first half.

Compelling risk/reward

Vitamin Shoppe has been this group's worst performer. This shouldn't be surprising as it had been the most bricks and mortar oriented of these names. Sterne Agee downgraded the company in September citing decreasing bricks and mortar traffic and new store productivity.

However, it has made significant progress on e-commerce. Their site, which features 20,000 SKUs, generated 18.5% sales growth yoy in the second quarter making eight quarters of double digit e-commerce growth. This offset an anemic 2.3% same store sales number in the second quarter.

As of the second quarter their website is at capacity but the company expects their new distribution center will be up to speed within eighteen months. They will then be able to fully leverage their Super Supplements website acquisition, part of their 2012 Super Supplements buy which added 31 bricks and mortar stores in the Pacific Northwest. Their new Super Supplements e-business added 5.5% to the online sales growth number.

Vitamin Shoppe has been growing EPS, 9.1% in the last quarter alone, and reported 31 straight quarters of positive same store comp sales growth. Unfortunately for them, comps were stronger in 2012 (8.3% yoy) and they are still digesting the Super Supplements buy. Gross margin as a percentage of sales contracted from 35% to 34.8% yoy. But the company exited the quarter with $54.8 million in cash and cash equivalents and no long term debt.

Vitamin Shoppe is still growing bricks for a total by year end of 50 new stores but down from their 3,700 square foot model to 3,000 square feet per store.

The Foolish takeaway

Vitacost has yet to balance margins and promotion as it grows its customer base. However, they ares making progress and its international growth is white hot. I also like that it is increasing its proportion of proprietary products and that the new fulfillment center is up and running.

GNC is simply best of breed and its two website purchases show it knows where its bread is buttered. As far as it has run it can probably run higher.

Vitamin Shoppe will be working through distribution issues for several quarters. While it has a clean balance sheet I have to like Vitacost and GNC more.

The article Clicks Beat Bricks in This Hot Sector originally appeared on Fool.com.

AnnaLisa Kraft has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.