Should You Shred This Paper Investment?

Did you ever have a teacher or parent who said, "If (enter name here) jumped off the Brooklyn Bridge, would you do it?"

When it comes to International Paper , many investors are jumping off the Brooklyn Bridge -- figuratively speaking. There's one primary reason for this, but investors might be overlooking some important facts.

Investor Panic

On September 11, 2013, International Paper announced that it would be closing its Courtland, Alabama paper mill. International Paper attempted to find solutions to keep the plant open, as its employees weighed heavily on the company's mind. However, when you're publicly traded, you have to be fiscally responsible. Unfortunately, International Paper will cut 1,100 employees by the end of the first quarter in 2014.

When a company cuts employees, it reduces expenses, which often leads to stock appreciation. The International Paper situation is different because the primary reason for the layoffs relates to a dying industry, opposed to broader economic weakness. According to International Paper, the paper industry has been in decline since 1999, and that trend is accelerating.

E-commerce via the internet has grown at a rapid rate since the turn of the Millennium. As more businesses operate electronically, demand for freesheet paper products has plummeted. Put simply, not as many businesses and people, use envelopes, labels, printers, or copiers as in the past. Of course, they're still used, but when it comes to investing, it is all about future growth.

The closure of the Courtland, Alabama paper mill acted as a warning sign to investors that International Paper might be heading in the wrong direction. However, according to International Paper, its paper business is still valuable, and thanks to manufacturing and supply chain strategies, the company is well positioned. It will continue to serve the North American uncoated freesheet market.

On the very next day, International Paper announced a $1.5 billion stock buyback over the next two to three years, and it hiked its dividend 17%. The company also stated that it is confident in its long-term profitability and free-cash flow generation. These are important points that shouldn't be overlooked. And if you think International Paper might be in serious trouble, you might be mistaken.

No Reason to Panic

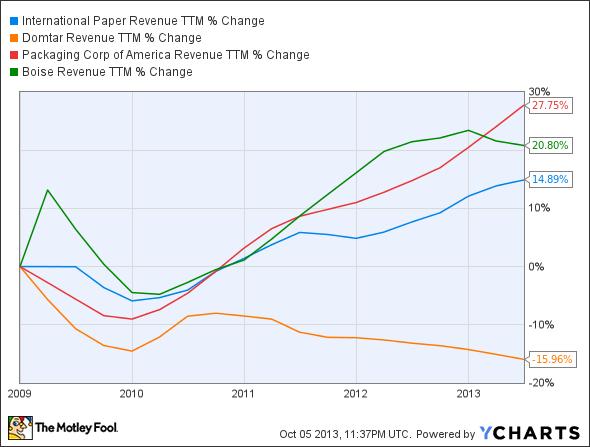

International Paper isn't just in the paper business. Its industrial packaging and consumer packaging businesses give it strong growth potential and diversification. Consider the top and bottom-line performances for International Paper and peers Domtar , Packaging Corporation of America , and Boise .

IP Revenue TTM data by YCharts

International Paper might not have been the top performer of the group, but it certainly held its own.

IP EPS Diluted TTM data by YCharts

International Paper is consistently profitable, which is what Foolish investors want to see.

Let's compare some key metrics:

Company | Forward P/E | Net Margin | ROE | Dividend Yield | Debt-to-Equity Ratio |

|---|---|---|---|---|---|

International Paper | 10 | 3.68% | 13.71% | 3.20% | 1.73 |

Domtar Corporation | 12 | 1.56% | 3.00% | 2.70% | 0.42 |

Packaging Corporation of America | 16 | 7.49% | 22.89% | 2.80% | 0.77 |

Boise | 14 | 0.55% | 1.79% | 0.00% | 1.03 |

International Paper is trading at just 10 times forward earnings. Considering the company's revenue and earnings-per-share performances, as well as the key metrics in the chart above, that looks like a bargain. You might have noticed the high debt-to-equity ratio. If International Paper continues to divest its underperforming assets, this number should improve. That fact, combined with management's confidence in the future, should keep the generous 3.20% dividend safe.

Domtar is up 25% over the past month, primarily because of International Paper's mill closing, which increases Domtar's market share. You might be wondering why this is such a big positive since the paper industry is in decline, but with Domtar, it goes a little deeper. It relates to the company's recently improved diversification after acquiring Associated Hygienic Products (exposure to the disposable diaper market) and Xerox's paper and print media business in the United States and Canada.

Impressively, despite these acquisitions, Domtar has still managed its debt load. But unfortunately, Domtar has been fading on the top and bottom line for years.

Investors are also excited about Packaging Corporation of America, especially after it acquired Boise. This is expected to increase Packaging Corporation of America's containerboard capacity by 42%, its corrugated products volume by 30%, while also improving sales mix, and cutting transportation and SG&A costs.

That said, some investors and analysts feel the price of $1.995 billion, or $12.55 per share, was too high. Packaging Corporation of America argues that this deal will increase cash flow, which will allow the company to pay down debt and reward shareholders. As far as Boise is concerned, the stock won't move much after the acquisition news, and downside potential now outweighs upside risk if the deal didn't pass regulatory approval.

The Bottom Line

Based on International Paper's consistent performance, strong fundamentals, diversification, focus on reducing costs, ability to generate cash flow, and generous yield, the stock looks to be oversold. If you choose to invest, keep in mind that it could get worse before it gets better. But ultimately, International Paper is a solid company that isn't going anywhere.

Looking For More Long-term Investment Ideas?

Every good investor wants to build that perfect portfolio that they can set and forget forever. Fortunately, it's easier than anyone ever knew. We've uncovered the pillars of such a portfolio today and we're willing to share The Motley Fool's 3 Stocks to Own Forever. Simply stated, we think they're the best stocks for true long-term investors to know about, and you can uncover them for free today, instantly; just click here now.

The article Should You Shred This Paper Investment? originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.