Profit from the High Demand for Jewelry

Zale is a specialty retailer of fine jewelry that has 1064 stores and 630 kiosks across North America. If you have ever walked through a mall, then you're familiar with the name Zale. With strong brand name recognition and the company swinging to a profit in fiscal-year 2013, you would think Zale should present a quality investment opportunity. While this is a possibility, there are several reasons why one much larger jewelry company should present a better long-term investment opportunity.

Recent results

Zale saw net earnings of $10.0 million in fiscal year 2013 versus a net loss of $27.3 million in fiscal year 2012. The improved performance was primarily due to a 60 bps improvement in gross margin (thanks to stable commodity costs) and a $21.5 million decline in interest expenses. However, SG&A expenses increased $14.0 million; these expenses are expected to remain high since they're necessary to help drive growth.

2013 was impressive, and it might indicate the beginning of a turnaround on the bottom line. However, keep in mind that other than in 2013, Zale has reported losses since 2008.

It has been difficult for Zale to keep costs down through the years, but the company is now committed to divesting underperforming stores, as shown by its 84 store closures in 2013. Zale is primarily focused on closing Gordons and Mappins brand stores, which saw comps declines of 3.6% and 6.7%, respectively.

Impressively, despite these store closings revenue still managed to increase to $147.7 million from $146.8 million in 2012. With overall comps growing at a 3.3% clip, this indicates that demand for Zale merchandise increased. In fact, that strong demand has been seen at Zale (4.9% comps growth), Outlet (3.3% comps growth), Peoples (5.7% comps growth), and Piercing Pagoda (1.3% comps growth).

Zale also increased exclusive and branded merchandise to 11% of fine jewelry revenue from 8% of fine jewelry revenue in 2012, expanded its multichannel business model (giving consumers more opportunities to shop), and reduced its outstanding debt by $43 million.

Looking ahead

Zale aims to drive profitable growth and increase shareholder value by driving revenue growth through positive Zale and Peoples comps. This is expected to be done through continued expansion of exclusive and branded merchandise. Another expected tailwind is lower commodity costs.

In fiscal year 2014, Zale expects capex between $40 and $45 million, higher than its capex spending of $23 million in fiscal year 2013. As mentioned earlier, this spending is necessary in order to help fuel growth. The capital will primarily be spent on store openings, refurbishments, and point-of-sale upgrades. Though Zale will be looking to open new stores, this will only be for its stronger brands. It will still close 50-55 stores, primarily Gordons and Mappins locations.

Zale has a simple yet effective strategy: it is aiming for growth with its stronger brand stores while improving the bottom line by divesting its underperforming brand stores. On paper, this game plan should work, but unexpected external events can throw a monkey wrench into a company's plans. That's why you might consider a larger and safer option when it comes to investing in jewelry stores.

Peer comparisons

It's clear that Zale has potential going forward, but while past performance doesn't guarantee future results, it's often a very good indicator of management capabilities. With that in mind, consider the revenue performance for Zale compared to that of Tiffany , as well as Signet Jewelers , over the past five years:

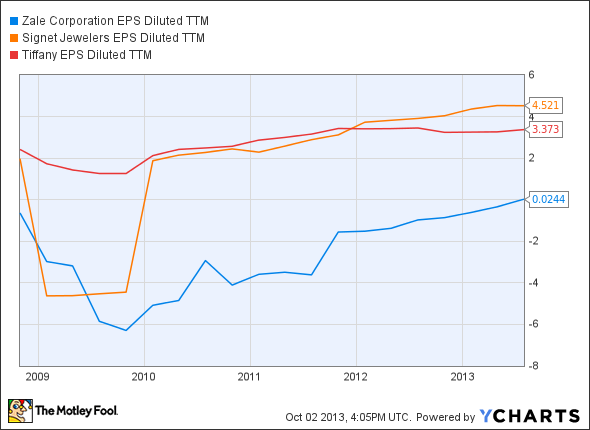

Zale grossly lags its peers in this area. Now consider bottom-line performance over the past five years:

ZLC EPS Diluted TTM data by YCharts

Once again, Zale lags its peers. However, it's certainly headed in the right direction, and that's what investors want to see.

Tiffany is likely to be a safer investment primarily because of its brand recognition. It's one of the best-known names in jewelry all over the world, which leads to pricing power. And Tiffany is performing well in the America's, Asia-Pacific, and even Europe. In the second quarter, Tiffany's net sales increased 4% year over year, with comps improving 5%. Tiffany also upped its full-year earnings-per-share guidance to $3.50-$3.60 from $3.43-$3.53.

Since Signet Jewelry looks impressive on both the top and bottom lines, you might be aching for more information. Signet Jewelry has a strong presence in the U.K., but sales have been weak across the pond, which, combined with higher costs (cuts into margins), has led to reduced guidance for the current quarter. However, Topeka just rated it a Buy with a price target of $83, likely based on the company's long-term potential.

At the podium

Though Zale might be capable of a turnaround, the company's track record is somewhat concerning. Growing the top line while also divesting underperforming locations in order to improve the bottom line will be challenging, but it is possible. Unless you seek unnecessary risk, Tiffany would be the most logical long-term investment option of the three aforementioned companies based on brand recognition, pricing power, consistent top and bottom-line performance, comps growth, international expansion, and upped guidance.

Even better than investing in jewelry

Have you missed out on the massive gains in bank stocks over the past few years? There's good news: It's not too late. Bargains of a lifetime are still available, but you need to know where to look. The Motley Fool's new report "Finding the Next Bank Stock Home Run" will show you how and where to find these deals. It's completely free -- click here to get started.

The article Profit from the High Demand for Jewelry originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.