A Company Obsessed with Efficiency

Mondelez International sells biscuits, gum, candy, beverages, cheese, and more in 165 countries. It spun off Kraft last October so it could focus on high-growth emerging markets. Since the spinoff, Mondelez has performed OK on the top line, and not so well on the bottom line (more on this below). However, these trends are to be expected after such a significant change. What's more important is the company's future.

Organic growth

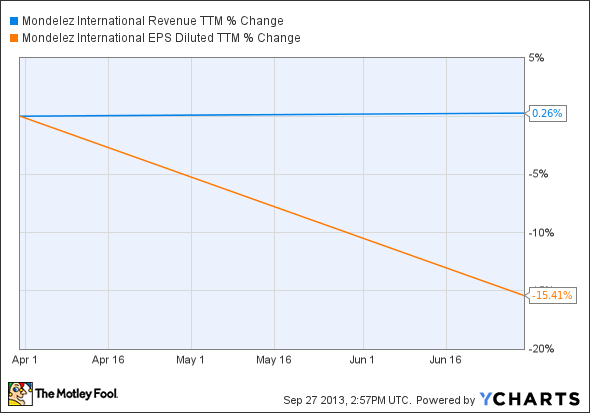

If you look at the top and bottom-line performances for Mondelez over the last six months, then you're not likely to be impressed:

MDLZ Revenue TTM data by YCharts

But in the second quarter, organic net revenue (excluding the Kraft spinoff) increased 3.8% to $8.7 billion. Looking at diluted EPS, Mondelez saw a 25.9% bump to $0.34, as the repurchase of 3.2 million shares aided this number. Going forward, management is looking to boost profits.

Efficiently focused

Mondelez is consistently divesting under-performing businesses, such as its salty snacks business in Turkey, confectionery business in South Africa, dinners and sauces grocery business in Germany and Belgium, and its canned meat business in Italy. Taken separately, these are all small divestments. As a whole, they make an impact.

Mondelez is also focused on margin expansion through supply chain reduction, which, over the next three years, is expected to deliver:

$3 billion in gross productivity

$1 billion in incremental cash

$1.5 billion in net productivity

60 to 90 basis point or bps, annual improvement in operating margin

Mondelez plans on paying for growth in emerging markets with margin expansion in mature markets. Monedelez International exceeded its own expectations in North America, and is now expecting a 500 bps improvement in operating margin by 2016, as opposed to the original expectation of 2017. A 250 bps improvement by 2016 in Europe is still on track.

For the 2013 fiscal year, Mondelez expects organic net revenue growth between 5% and 7%. The share repurchase program was increased to $6 billion from $1.2 billion, which will help the bottom line. And the quarterly dividend was recently raised 8%. Needless to say, Mondelez takes care of its shareholders.

Other tasty investment options

Mondelez International might have its power brands like Oreo, Nabisco, Chips Ahoy!, Cadbury, Milka, and Club Social, but its brand portfolio still isn't as broad or popular as Nestle's , which consists of Nescafe, Perrier, Baby Ruth, Butterfinger, Kix, Nesquik, Stouffer's, Toll House, and more.

Groupe Danone is a competitor to both Mondelez International and Nestle in dairy. Danone is best known for its yogurts, and it recently acquired YoCrunch, which, ironically, comes with Oreo toppings (as well as M&M toppings) via licensing agreements. If you follow Danone, then you're aware of the recent Chinese bribery claims. Regardless of what happens, it will likely be a short-term event that won't affect long-term performance.

Revenue numbers for Mondelez were provided above. Since Mondelez has been on its own for less than a year, annual numbers can't be provided. However, you can take a quick look at annual revenue and EPS numbers for Nestle and Danone to help determine if one of these companies might be the right investment for you:

Nestle | 2008 | 2009 | 2010 | 2011 | 2012 |

|---|---|---|---|---|---|

Revenue (in millions) | $101,819 | $99,396 | $105,443 | $94,708 | $98,372 |

Diluted EPS | $4.49 | $2.69 | $2.43 | $3.27 | $3.60 |

Revenue still hasn't recaptured 2008 levels, and earnings per share have been volatile. On the bright side, Nestle consistently delivers large profits.

Danone | 2008 | 2009 | 2010 | 2011 | 2012 |

|---|---|---|---|---|---|

Revenue (in millions) | $22,393 | $20,894 | $22,588 | $26,906 | $26,840 |

Diluted EPS | $0.91 | $0.68 | $0.73 | $0.76 | $0.71 |

Danone has surpassed 2008 revenue levels, which indicates increased demand, but revenue declined in 2012. Earnings per share performance has been inconsistent, but Danone expects growth in 2014.

All three companies are relatively similar on a fundamental basis:

Company | Forward P/E | Net Margin | ROE | Dividend Yield | Debt-to-Equity Ratio |

|---|---|---|---|---|---|

Mondelez International | 19 | 6.74% | 5.69% | 1.70% | 0.57 |

Nestle | 17 | 11.41% | 18.55% | N/A | 0.45 |

Danone | 17 | 8.22% | 15.93% | N/A | 1.00 |

Thanks to solid fundamentals, brand diversification, strategic marketing, and effective management, all three companies are likely to be long-term winners. If you're looking for dividend payments, then Mondelez is your only option in this group, as it currently yields 1.70%. With a debt-to-equity ratio of 0.57, the dividend should remain intact.

What to expect from Mondelez

Mondelez International should be able to grow the top line via geographic expansion in emerging markets. At the same time, it considers itself "laser-focused" on supply chain improvements. Furthermore, Mondelez is shareholder-friendly, meaning it likes to return capital to shareholders with dividends and buybacks. While nothing is guaranteed, especially considering the company's new solo adventure, upside potential outweighs downside risk.

Follow the smart money

With so much of the financial industry getting bad press these days, it may be a greedy when others are fearful moment. Not surprisingly, some of Warren Buffett's biggest investments are in the space. In the Motley Fool's free report, The Stocks Only the Smartest Investors Are Buying, you can learn about a small, under-the-radar bank that's too tiny for Buffett's billions. Too bad, because it has better operating metrics than his favorites. Just click here to keep reading.

The article A Company Obsessed with Efficiency originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.