The Dirty Secret Holding Back the U.S. Economy

Loans, specifically bad loans, got the U.S. into the current financial crisis, otherwise known as the Great Recession, or the "new normal" we're all dealing with today. That's perhaps overly simplifying it, but it is essentially the root of the problem.

Believe it or not, though, it's loans that will spur the economy back to the level of growth we all want.

Am I crazy?

Maybe. But not about this. For those of you with 30 minutes to spare -- check out this video posted over at EconomicPrinciples.org. It gives a truly brilliant and succinct explanation of how credit (think bank loans) fits into the grand scheme of our economy.

I'll attempt here to give you the Cliffs Notes:

The economy is based on transactions -- that is to say, people exchanging a good or service for some amount of money.

When you spend money to purchase that good or service, your money is income for someone else.

More spending, therefore, equals more income.

As long as income rises at the same or greater rate as debt, the economy can, in theory, continue to grow (and at a faster pace than without credit -- more credit equals more spending power, which equals higher income).

Where things get hairy is when the debt load rises faster than incomes. When that happens, banks no longer see borrowers as being creditworthy, and they stop making loans. Fewer loans means fewer transactions, which means less income across the board. This becomes a self-fulfilling prophecy, as banks will continue to tighten as times continue to worsen.

How can we break the cycle? The incredibly oversimplified version is that it breaks when banks begin lending money again (for a more thorough and brilliantly succinct explanation, watch the video -- seriously, its worth 30 minutes of your time).

I'm not talking about making subprime home loans to individuals with no income or, for that matter, making huge, unsecured loans to Nigerian princes. I'm talking about making sound loans to creditworthy individuals and businesses based on repayment ability and character. Making loans that have a viable first and second source of repayment.

More loans, more transactions, more income

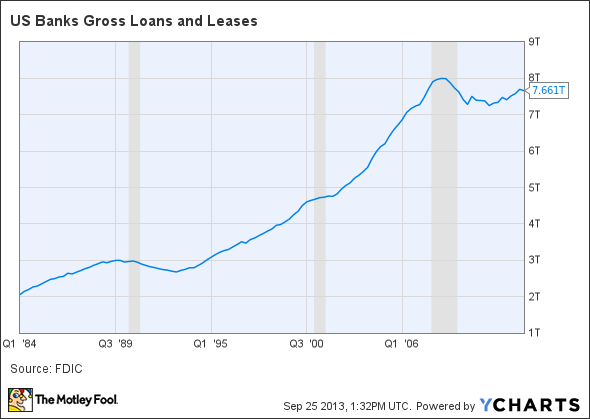

Check out this chart of the total loans and leases outstanding at U.S. banks since 1984. Declining or stagnant loans outstanding are a very clear marker of each of the past three recessions.

U.S. Banks Gross Loans and Leases data by YCharts.

Since 2007, total loans sharply declined and then more or less flatlined. Fewer loans means fewer transactions, which means slow growth. The question, then, is why?

More than any other factor, and despite their best intentions, Congress and regulators are holding back the economy.

What does government have to do with bank loans?

Easy -- there is too much complexity in regulations that are attempting to be one-size-fits all. It's suffocating the industry.

For example: 800+ page legislation, 2,000+ page implementation rules, 75 pages just to explain one liquidity ratio! Fools, this is the reality for banks today.

This complexity is taking resources away from making loans. Its stymieing creative thinking and limiting credit products. Its preventing individuals and businesses from getting access to the credit they need to reboot the economy. It's making it too hard to originate new loans, it's limiting transactions, and it's slowing growth.

Forget the trillion-dollar megabanks on Wall Street. Think instead about the community and regional banks on Main Street. The banks who would, under normal circumstances, consider giving your local hardware store a loan to expand, who would sit down with you if times got tough and give you advice on your mortgage options instead of calling in a "Special Assets" group in New York City, San Francisco, or Charlotte.

Cliff McCauley, executive vice president at Cullen/Frost Bankers testified to this point before the House Financial Services Committee, saying:

"The resulting carnage of this exercise in excess [The Financial Crisis] has cost our constituency dearly in the form of increased regulatory scrutiny and costs, competition with enormous entities that are perceived by the public as 'too big to fail', declining collateral values, an artificially low interest rate environment, and a plethora of other frustrating -- and expensive -- consequences."

Cullen/Frost, to be clear, is no small fry. At $19 billion in total assets, this bank is a leading institution in the greater Texas region in terms of both market presence and conservative, old-school banking.

Ignacio Urrabazo, president of a $500 million subsidiary bank owned by International Bancshares Corporation , reiterated the sentiment in front of the committee, saying:

"As seen in prior economic cycles and prior periods of crises, policymakers and the regulators overreact to these cyclical problems. Congress's holistic approach to fix everything in the financial sector has created unnceccesary and inflexible rules. The Dodd-Frank Act in my view is a perfect example of horrible overreach. The Dodd-Frank bill which is 848 pages long, is an outline directed at bureaucrats and it instructs them to make still more regulations and to create more bureaucracies -- it can in fact become a multi-headed monster."

International Bancshares is an $11.6 billion holding company. Again, like Cullen/Frost, this holding company has scale, but nothing like that of Bank of America or other megabanks. Without that kind of scale, banks are being forces to misallocate resources to deal with regulatory compliance instead of making safe and sound new loans.

Let's give some context, here: Bank of America reported a net profit of $5.5 billion for the six months ending June 30, 2013. That's a lot of money by any standard, but consider that this is after the bank spent nearly $2.7 billion on legal expenses alone over the same period. Bank of America will eventually fully recover from the crisis and adapt to this regulatory environment. Scale like this can absorb 2,000+ pages of new regulatory rules and remain competitive; community and regional banks have a much more difficult time.

It's time for the bankers to get back to banking

The real losers in this situation are you and me. It's the small business owners. It's the unemployed. It's now been over five years since Lehman Brothers collapsed. The greed and malfeasance that led us to this point is tragic and unfortunate, but our current course of action is doing little to move the economy forward. It's time for banks to get back to making loans. And it's time for regulators and Congress to help them do it.

Like it or not, the very banks that got us into this mess will be the key driver to get us out again.

Have you missed out on the massive gains in bank stocks as they've bounced from the doldrums of 2008? There's good news: It's not too late. Bargains of a lifetime are still available, but you need to know where to look. The Motley Fool's new report "Finding the Next Bank Stock Home Run" will show you how and where to find these deals. It's completely free -- click here to get started.

The article The Dirty Secret Holding Back the U.S. Economy originally appeared on Fool.com.

Fool contributor Jay Jenkins has no position in any stocks mentioned. The Motley Fool recommends Bank of America. The Motley Fool owns shares of Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.