Is This Auto-Parts Retailer Worth Buying?

AutoZone , the largest auto-parts retailer in the U.S., has been a steady performer so far this year with shares up almost 21%. This might not sound great given that the S&P 500 index has done better, but the auto-parts retailer has been consistent in its performance. Over the years, AutoZone has slowly but steadily managed to increase revenue and earnings, while share price appreciation has been quite decent as well.

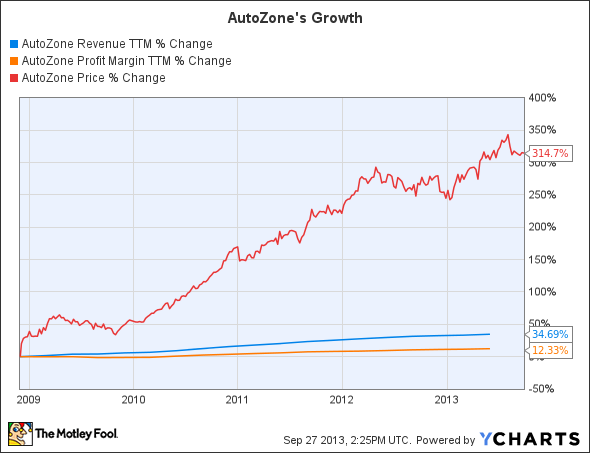

AZO Revenue TTM data by YCharts.

Its recently released second-quarter results (covered in detail by my Foolish colleague Eric Volkman) were positive, as AutoZone managed to post growth in same-store sales this time, up 1% in the quarter. In comparison, they were down 0.1% in the third quarter, so same-store sales moving into positive territory is a good sign. However, same-store sales for the full fiscal year were flat.

The commercial opportunity

AutoZone expects better times in fiscal 2014. The company expects growth across all its business lines and it has been taking a few steps to improve its business further. AutoZone has been expanding both retail and commercial sides of its business. It opened 153 new stores in fiscal 2013 and introduced 368 new commercial programs.

AutoZone now runs its commercial program in 71% of its stores in the U.S. This means that the company is in a good position to benefit from the growth of the commercial market for auto parts. According to AutoZone's peer Advance Auto Parts , the commercial market is worth $40 billion and is growing at twice the rate of the do-it-yourself segment.

AutoZone is in a solid position to capture the commercial market because of its wider store coverage and aggressive deployment of commercial programs. Advance Auto has also been making some moves to make its presence felt in the commercial segment, but it would probably take quite some time for it to catch up with AutoZone.

Advance Auto has been focusing on improving the sourcing and distribution of parts to commercial customers and acquired 124 stores from BWP Distributors earlier this year. In addition, Advance Auto management also stated on the previous conference call that the company is strengthening its sales force to win over more commercial customers.

It might be possible that Advance Auto's expansion might take some wind out of AutoZone's commercial business. But AutoZone's superior store network of 5,200 stores, as compared to Advance Auto's 4,000 stores, could work in its favor since it will be able to provide service to a wider customer base.

Store and hub improvements

AutoZone has also been expanding its store count, and it opened 92 stores in the previous quarter. The company is focused on expanding its business in Mexico as well, where it had 362 stores at the end of the last quarter. Management is satisfied with the performance of stores in Mexico, and that's why the country saw 21 new store openings during the quarter.

Apart from expanding its store network further, AutoZone is also looking to make the availability of parts more efficient. As such, the company has been improving the location of its hubs and expanding their size. It has now remodeled a total of 92 hubs for greater efficiency.

The average age of vehicles in the U.S. is increasing despite an increase in sales of new cars this year. According to market research firm Polk, the average age of vehicles on American roads is now 11.4 years -- an all-time high. This means that aftermarket retailers such as AutoZone will continue to find takers for their products and services as consumers look to keep their older vehicles in good shape.

Debt and valuation

With all that said, AutoZone's debt is a concern. As I pointed out in a previous article, the cash that the company generates is used to repurchase shares instead of repaying debt. For instance, in the previous quarter, it generated $519 million of operating cash flow and spent $560 million repurchasing shares.

AutoZone's debt stands at $4 billion and has increased $420 million from the year-ago period in the previous quarter. In comparison, Advance Auto and even O'Reilly Automotive , which is a faster-growing player, have considerably lower debt levels. Moreover, at 16 times trailing earnings, AutoZone is slightly more expensive than Advance Auto, which is turning around at a faster rate.

O'Reilly is the most expensive of the lot with its trailing P/E at 23 times, but the company's earnings have been growing at a fast clip. In the previous quarter, O'Reilly saw earnings jump 21% from the year-ago period while same-store sales improved an impressive 6.5%. The company's solid strategies and good execution have helped it perform better than its peers.

To expand its business further, O'Reilly is moving into markets such as California, where it doesn't have a strong presence. With earnings expected to grow at an annual rate of 17% for the next five years, O'Reilly looks like a good bet.

The bottom line

AutoZone's dominance in the fast-growing commercial market and its superior store network are positives that cannot be ignored. The company is also looking to shore up its distribution networks by remodeling its hubs, and the higher average age of vehicles should also assist its growth. Its debt is the only sticking point for me, but for investors who can ignore the debt situation, AutoZone might turn out to be a good investment.

2 automakers to consider investing in

There's good reason to believe that the most successful investors over the next few decades will be those with exposure to China's massive and growing population of domestic consumers. And there are few things that these consumers are likely to purchase with more enthusiasm than cars and trucks. In this brand-new free report, our analysts get out in front of this trend by identifying two automakers that are poised to surge along with China's middle class. If you want to be among the smart investors who get rich from this growing trend, then you'd be well advised to instantly download our free report on the topic by clicking here now.

The article Is This Auto-Parts Retailer Worth Buying? originally appeared on Fool.com.

Fool contributor Harsh Chauhan has no position in any stocks mentioned. The Motley Fool owns shares of O'Reilly Automotive. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.