Is Copper Worth Your Time?

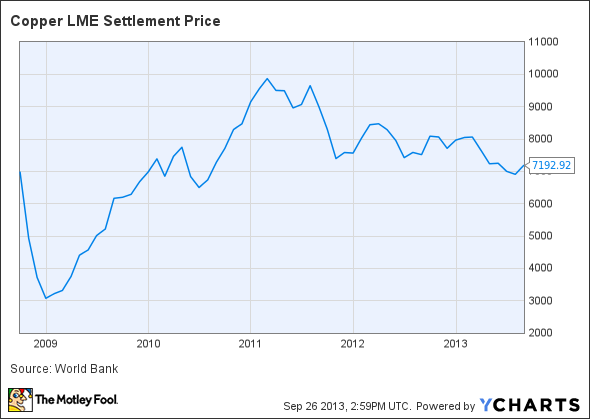

The price of copper has been falling, and so have shares of copper miners. The bad news is that the International Copper Study Group expects further discrepancies between supply and demand. It projects that the growth rate of global refined copper usage will be at least 1.2 percentage points below total refined copper production's growth rate in 2013 and 2014. Some miners are still worth looking at, but you need to dig down and take a long-term view.

Copper LME Settlement Price data by YCharts

The big picture

Construction is one of the biggest drivers of copper demand, and slowing industrialization in the emerging markets is creating a bear market. The copper industry needs to realize that falling growth rates in China will decrease future demand, and fewer mines need to be opened. Downward pressure on copper prices may be a blessing in disguise, as it will help decrease the number of new mines brought online.

The miners

Southern Copper is one of the stronger pure copper plays. The company owns a number of mines in Mexico and Peru. As of the second quarter of 2013 its operating cash costs net of by-products averaged $1.09 per pound of copper, while LME copper price per pound fell slightly to $3.24. This means that Southern Copper does have some breathing room, even if prices fall farther.

One of the biggest threats for Southern Copper is cost inflation. It should be able thrive in the medium term, but it needs to keep costs under control as global consumption growth slows. Maintaining healthy cash flow is challenging, and new environmental regulations recently forced the company to spend $570 million to improve sulfur capture in one of its Peruvian smelters.

Regardless, the firm needs to maintain its capex. It has a number of projects that should come online by the end of 2014 and 2015. Long-term investors should not be surprised if investment spending compresses earnings growth for the next couple of quarters.

Freeport-McMoRan Copper & Gold is one of the most interesting plays within the copper market. It recently broke the mold when it decided to merge with the oil and gas firm, Plains Exploration & Production. The merger reduces Freeport's dependency on the volatile metal prices, but it also means that management must navigate two very different industries.

In May a mining accident forced Freeport to close its Eastern Indonesian operations for a government inspection. Its facilities have been restarted, but its 2013 copper production is expected to be reduced by 230 million pounds of copper, and its gold production is expected to fall by 250,000 ounces. Varying ore grades have temporarily compressed its margins in its Grasberg mine, but in the 2014 to 2016 period the company expects margins will bounce back.

Considering Freeport's 2013 accident and the temporary fall in Grasberg's margins, investors can expect stronger earnings in in the next couple years.

Taseko Mines is a relatively small miner that owns Canada's second largest open pit copper mine. The company is not profitable, but it is working on a number of interesting projects. Investing in undeveloped mines is risky, but Taseko mitigates these risks by focusing on projects in Canada where resource nationalization is a very small threat.

It is working to get its New Prosperity mine in British Columbia approved. Ottawa already rejected Taseko's proposal once due to environmental concerns. After a $300 million redesign the company is hopeful that it will get the mine approved and eventually be able to push its earnings into the black.

Taseko is an interesting company to watch, but it is still a small firm developing billion dollar projects in a world of compressed commodity prices.

Teck Resources is a large diversified miner with significant interests in copper, energy, and metallurgical coal. Its 2012 copper cash costs after by-products were an economical at $1.56 per pound. In light of recent price declines in copper and other commodities it has put off $650 million in capex for its Quintette mine. As of the second quarter of 2013 it hopes to cut $250 million more in annual costs.

Teck's ability to put off capex, engage in cost cutting and still turn a profit shows the benefit of investing in a large and diversified miner. Even with lower commodity prices Teck has options. The downside is that the company is trading at high valuations with a price-to-earnings ratio around 21.

Conclusion

Copper has taken a downturn, but some of the larger miners like Freeport-McMoRan and Southern Copper are worth looking at. Freeport had a number of temporary difficulties in 2013 that make it a good deal right now. Southern Copper's earnings will probably be compressed for the next year as it waits to finish a number of projects. If the market decides to punish the stock for a lack of short-term growth, buying it in the midst of the downturn could be quite profitable.

Keep on digging

Looking for more commodities-based ideas? Download the free report, The Tiny Gold Stock Digging Up Massive Profits. The Motley Fool's analysts have uncovered a little-known gold miner they believe is poised for greatness; find out which company it is and why its future looks bright -- for free!

The article Is Copper Worth Your Time? originally appeared on Fool.com.

Joshua Bondy has no position in any stocks mentioned. The Motley Fool owns shares of Freeport-McMoRan Copper & Gold. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.