Follow the Shorts, Invest in Solar

The solar industry is coming back from the dead. Margins are rising and investments in R&D are paying off. In the past year the number of shares of solar manufacturers sold short has fallen significantly, signaling that even investors skeptical of green energy are seeing improving prospects for the industry.

Short interest matters

In 2009 a number of researchers published a paper called The Good News In Short Interest. They looked at stocks traded between 1988 and 2005, finding that low short interest in heavily traded stocks was commonly associated with statistically and economically significant abnormal returns. It would not be a good idea to make investment decisions based on one number, but their findings confirm that short interest can be a useful metric for investors.

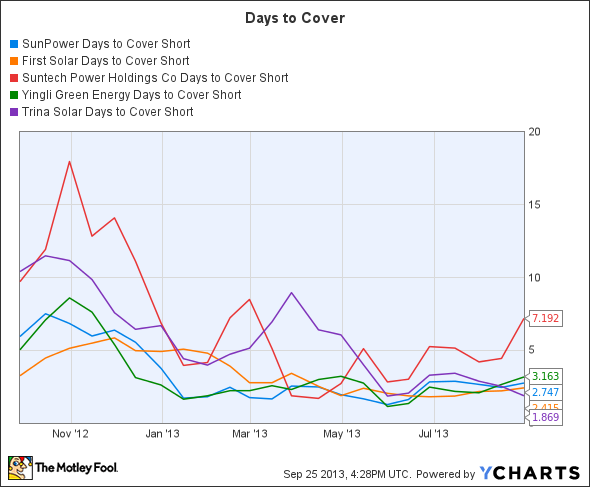

SPWR Days to Cover Short data by YCharts

The solar industry

The days to cover ratio looks at the average daily volume of a stock, and calculates how many days would be required to cover all short positions. In the past year big U.S. solar manufactures like SunPower and First Solar have seen their short ratios fall significantly.

Based on the fundamentals, short sellers have good reason to back away from these stocks. In the second quarter of 2013 SunPower's Japanese sales increased 30% quarter over quarter, and its European, Middle Eastern, and African regions' overall gross margin recovered from -32.2% to 9.7%. These numbers show that SunPower is growing and it is able to generate profit throughout the global market.

First Solar is somewhat of an exception in the industry. It sports a positive profit margin of 10.5%. As of the second quarter of 2013 it was able to keep its capacity utilization at 75% and bring its cost per watt down to $0.67. Stronger capacity utilization is a sign that oversupply problems are being dealt with and First Solar will hopefully be able to bring its total cost per watt down even further, through more effective use of its existing plants.

One long-term challenge for First Solar is its concentration in the utility market. Right now utility scale systems are selling quite strongly, but utilities are starting to get into the distributed rooftop market where SunPower is better situated, thanks to its highly efficient and smaller systems.

China

Chinese manufacturers have some catching up to do. They consistently spend less on R&D than their U.S. rivals, stunting their potential growth. The solar industry is driven by falling costs on panels and rising efficiencies. The Chinese have tried to win the cost war by reducing unit costs through economies of scale, but as U.S. firms continue to improve efficiencies the Chinese are facing stiffer competition.

There is a good reason that the Chinese firms Suntech and Yingli Green Energy have the highest days to cover ratios. Suntech is stuck with a total debt-to-equity ratio of 2.84, substantially greater than SunPower's ratio of 0.95. Yingli Green Energy is in an even worse position. Its total debt-to-equity ratio is 11.59. Even Suntech's Chinese competitor Trina Solar is doing better, with a total debt-to-equity ratio of 1.59.

The solar industry as a whole is recovering, but many Chinese firms are saddled with overproduction and setbacks from reduced European subsidies. Trina's gross margin of 1.8% and Yingli's gross margin of 0.2% point to these challenges.

Earlier this year Suntech's debt load forced it to declare bankruptcy. It is currently restructuring and there is talk of major debt for equity swaps, making its stock best avoided for the time being.

Conclusion

The solar industry is on the upturn thanks to falling prices and rising efficiencies. Falling short interest in strong U.S. firms like SunPower and First Solar is a positive sign. Even investors willing to bet against green energy are seeing more upside in some solar manufacturers. For the majority of investors Chinese manufactures are still too risky to consider, thanks to their high debt loads.

How to profit from energy

There are many different ways to play the energy sector, and The Motley Fool's analysts have uncovered an under-the-radar company that's dominating its industry. This company is a leading provider of equipment and components used in drilling and production operations, and poised to profit in a big way from it. To get the name and detailed analysis of this company that will prosper for years to come, check out the special free report: "The Only Energy Stock You'll Ever Need." Don't miss out on this limited-time offer and your opportunity to discover this under-the-radar company before the market does. Click here to access your report -- it's totally free.

The article Follow the Shorts, Invest in Solar originally appeared on Fool.com.

Joshua Bondy has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.