Is It Time to Abandon Coal Miners?

China has banned the construction of new coal plants around Beijing, the Yangtze Delta region near Shanghai and in the Pearl River Delta region of Guangdong. Also, the EPA is hoping to decrease the amount of greenhouse gases that power plants can release and make coal more expensive, though these new standards will not be set in stone until June 1, 2015. These changes are putting pressure on coal miners, but some are better positioned to endure the pain.

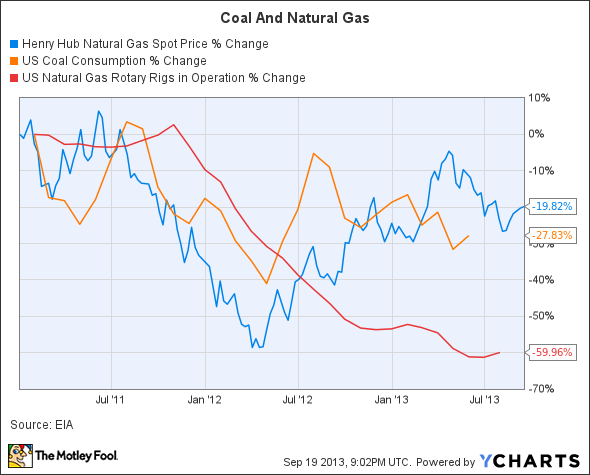

The positive news

When natural gas prices went down to $2 per million British thermal units, coal demand collapsed. Right now the opposite trend is occurring, as U.S. utilities are switching from natural gas to cheap coal. Given the collapse in natural gas rigs, prices should continue to rise.

Henry Hub natural gas spot price data by YCharts

The world's disdain for nuclear energy has boosted coal demand in many nations. In Japan alone the top six utilities are hoping to boost their coal consumption by 24% in 2013 and 2014. It is easy and cheap to take coal, put it on a boat and ship it across the Pacific, but the same cannot be said for natural gas. In 2011 high LNG costs helped push Japan into its first trade deficit in 31 years.

One miner to avoid

Not all coal is created equal. Higher quality coal offers fewer pollutants and relatively low extraction costs. Coal mined in older regions is generally more expensive due to falling mine yields.

James River gross profit margin quarterly data by YCharts

James River Coal operates a number of older mines in the Central Appalachia region where it made an average of $1.74 per ton in the second quarter of 2013.It is practically impossible to run a profitable company with these numbers. The company does have some Midwest assets with better margins, but the bulk of its production comes from the Appalachia region.

Going forward there is no reason why James River Coal would stop being a risky miner. It is a high-cost producer with very low gross margins.

The middle ground

Alpha Natural Resources has better margins than James River Coal, but it is still hurting. In the second quarter of 2013 production fell by 20%, though its metallurgical production remained steady. On the upside, Alpha Natural Resources has a number of export facilities on the East Coast. It is one of few firms with good export capacity, as it owns 41% of U.S. Dominion Terminal Associates.

This firm's debt load is also a positive. It has a total debt to equity ratio of just 0.7.It is important to note that at the end of 2012 only 16% of its reserves were found in the cheaper Powder River Basin.

Overall Alpha Natural Resources is a medium quality miner. The majority of its operations are found in expensive regions, but it is has strong export capacity and in the long run it will be able to gain better prices for its coal.

Arch Coal has traditionally maintained strong margins, but the Appalachia region is hurting its bottom line. In the second quarter of 2013 the company posted an operating margin of $-4.68 per ton in the Appalachia region.

The company's other assets in the Powder River Basin and the Western Bituminous region helped to even out its total earnings, but nevertheless there are hidden risks. If the company continues to lose money in the Appalachia region, it will need to close down mines and cut its costs in all areas.

Its balance sheet is another negative. The company has a large debt load and a total debt to equity ratio of 1.9. It cut its quarterly dividend from $0.11 to $0.03 as margins fell, and it would not be surprising if its dividend falls further.

A better option

Peabody Energy has played the coal game quite well. Before the market crashed it spun off its Eastern U.S. operations into a new firm called Patriot Coal. Patriot is currently in bankruptcy and Peabody may face a $150 million charge related to Patriot's liabilities, but overall this is a small issue.

Looking at Peabody's adjusted EBITDA, all of the company's mining segments posted profits in the second quarter of 2013. The market is prone to discount Peabody anytime negative Chinese news comes out, but in the long term India holds more hope for Peabody, due to its chronic coal deficit.

Peabody is a good miner to watch because of its profitable Australian assets and relative lack of exposure to high cost regions in the U.S. Regardless, its balance sheet and debt load must be watched.

Conclusion

Many miners like James River Coal are stuck with high-cost mines and limited export ability. Peabody is the exception as it has already sold off a number of poor quality mines and has profitable export operations in Australia. Alpha Natural Resources is a runner up thanks to its precious export facilities. There is no doubt that coal is in a tough spot, but some companies offer more opportunity than others.

Investing for expensive oil

Think the days of $100 oil are gone? Think again. In fact, the market is heading in that direction now. But for investors that are positioned to profit from the return of $100 oil, it can't come soon enough. To help investors get rich off of rising oil prices, our top analysts prepared a free report that reveals three stocks that are bound to soar as oil prices climb higher. To discover the identities of these stocks instantly, access your free report by clicking here now.

The article Is It Time to Abandon Coal Miners? originally appeared on Fool.com.

Joshua Bondy has a position in Peabody Energy Corp . The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.