A Consistent Winner in Teen and Young Adult Apparel

The teen and young adult apparel market hasn't been performing well of late. At the same time, this market isn't suddenly going to fade away into oblivion--after all, most teens and young adults still want to look fashionable. Therefore, an investment opportunity must exist somewhere. Buckle might present just such an opportunity.

Mixed results

Mixed results aren't often going to excite a reader looking for an investment, but Buckle's performance compared to peers is impressive.

In the second quarter, net sales jumped 7.9% to $232.5 million. Diluted earnings per share also improved to $0.52 from $0.49. Most importantly, comps registered 3.2% growth. On a comps basis:

Number of units sold per transaction: up 3.5%

Average retail price per piece: up 1.2%

Number of transactions: down 1.6%

The above numbers indicate that Buckle isn't generating as much traffic as in the past. This is likely due to a decline in mall traffic, which is where most Buckle stores are located. The good news is that once Buckle has people in its stores, those shoppers seem to be interested in what's being sold. They're not just buying more items than one year ago, but they're spending more due to price increases.

Based on the current situation, it's possible that Buckle will need to market and promote more, which would cut into margins and hurt the bottom line. However, this is just speculation.

In the second half of the year, Buckle plans on opening one new store and remodeling and/or relocating six others. This could aid the top line. Buckle is confident that it will generate enough cash flow to cover these expenses, as well as technological upgrades, dividend payments, annual bonuses, and changes in inventory.

In 2012, Buckle opened 10 new stores and remodeled 21 others, and the company expects a similar trend in the future. This is a positive for Foolish investors--after all, investing in companies that stick to realistic growth plans is always a good idea. If you're concerned about growth potential, then you will be happy to know that Buckle still doesn't have much big-city exposure. While it's possible that a Buckle retailer operates near you, it's not likely. This is a positive, simply because it shows that the potential for growth exists.

Prior to moving on, it should be noted that Buckle saw online-sales growth of 5.3% to $16.8 million in the second quarter year-over-year. This is a big positive since online sales come at a much lower cost.

Buckle vs. peers

Buckle competes with many other retailers targeting teens and young adults, two of which are Quiksilver and Tilly's .

Quiksilver is more of a wholesale and international company, with a focus on the surf and skate market. However, Quiksilver does have an established retail presence overseas. It sponsors athletes in the surf and skate markets for brand recognition purposes. But unlike Buckle, Quiksilver has had difficulty delivering profits, consistently reporting losses on an annual basis. Quiksilver plans on reducing overhead to improve profitability, but it has a steep hill to climb.

Like Buckle, Tilly's has managed to deliver profits. And while second-quarter sales improved 17% year-over-year and online sales saw a 30% bump, comps declined 0.5%. Tilly's expects comps to grow in the low-single digits moving forward, and with strong brands like Billabong and Hurley, this should be possible. A lot will depend on the company's marketing.

Looking at these three companies on a fundamental basis, Buckle clearly stands out:

Forward P/E | Net Margin | ROE | Dividend Yield | Debt-to-Equity Ratio | |

|---|---|---|---|---|---|

Buckle | 15 | 14.47% | 44.14% | 1.50% | 0.00 |

Quiksilver | 30 | (2.37%) | (8.32%) | N/A | 0.03 |

Tilly's | 15 | 5.79% | 25.97% | N/A | 2.28 |

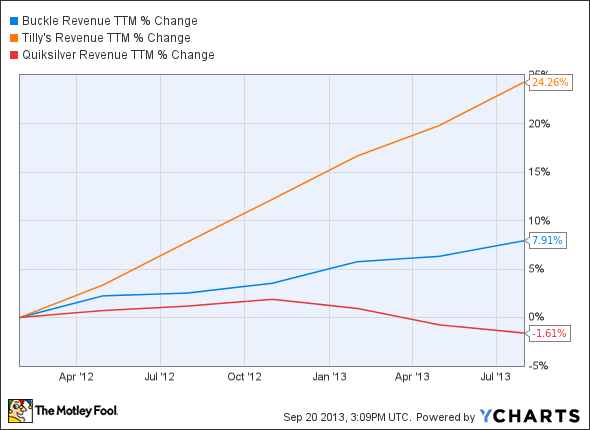

Buckle offers a good valuation, turns more profit and investor dollars into profit than its peers, pays a dividend, and has no debt. If you're still not a believer, consider revenue growth comparisons over the past five years:

Buckle revenue trailing-12 months data by YCharts

And EPS growth comparisons:

Tilly's EPS diluted trailing-12 months data by YCharts

The bottom line

As a retailer, Buckle is highly sensitive to consumer confidence. And considering a beta of 2.2, this isn't the right investment for the faint of heart. However, if you remove external circumstances from the picture, you will find a fundamentally sound company with a methodical and realistic growth plan. While Buckle isn't the top investment option in retail, it has good potential to be the best long-term investment option in the aforementioned group.

Even more potential in retail

The retail space is in the midst of the biggest paradigm shift since mail order took off at the turn of last century. Only those most forward-looking and capable companies will survive, and they'll handsomely reward those investors who understand the landscape. You can read about the 3 Companies Ready to Rule Retail in The Motley Fool's special report. Uncovering these top picks is free today; just click here to read more.

The article A Consistent Winner in Teen and Young Adult Apparel originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool recommends The Buckle. The Motley Fool owns shares of The Buckle. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.