Can This High-Flying Tech Player Continue to Run?

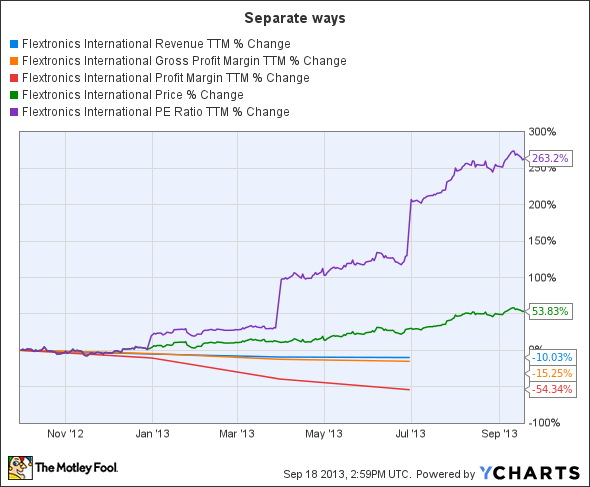

Investors seem to be optimistic about the prospects of electronics manufacturing services provider Flextronics International . The stock is trading close to its 52-week high after an impressive run this year. However, revenue and profit have been declining and Flextronics' solid run up of more than 50% this year means that it has become relatively expensive.

FLEX Revenue TTM data by YCharts

Getting better

But then, it looks like Flextronics' business is gradually improving as evidenced by an upbeat guidance for the ongoing quarter. When Flextronics reported earnings in July, the company guided for revenue of $6.10 billion to $6.40 billion, while analysts were expecting $6.11 billion. Also, the company's earnings guidance of $0.19 to $0.22 per share was ahead of the $0.18 per share expectation.

Flextronics has been enjoying great catalysts of late -- it is assembling Google's Moto X smartphone and also Microsoft's Xbox. These are probably the reasons why Flextronics called for greater-than-expected growth in its high velocity business.

Two big movers

The high velocity solutions business was up 31% sequentially in the previous quarter on the back of the Google/Motorola partnership and another 25%-30% improvement is expected in the ongoing quarter. The Moto X is the first phone from Google since its Motorola acquisition and the company has been shipping 100,000 new phones every week from a facility near Dallas.

Also, as reported by Reuters, Motorola management states that Flextronics' Texas facility is capable of producing "tens of millions" of phones a year, depending on demand. Google is focusing on the "Made in the USA" theme for the Moto X and as The Wall Street Journalreports, Google might spend more than $500 million to market the device across the world.

The Moto X has been well-received and the fact that it is available on all five major carriers in the U.S. is another advantage. With Flextronics being a key partner in Google's Motorola venture, the success of the Moto X and future devices will be an advantage for the contract electronics manufacturer.

Then there's the Xbox One, which is expected to be another driver and help Flextronics achieve above-average growth rates over the next few quarters. Microsoft's console refresh comes after eight years and the company is going all out after Sony's PlayStation 4.

Microsoft bungled the launch earlier this year and it had to backtrack on its requirement of gamers connecting to the Internet at least once a day. Moves like these, and also the fact that Microsoft boosted the GPU of the console as well, seem to have put the Xbox One back into the good graces of gamers.

That's probably why analysts appear to be more positive about the prospects of the Xbox One as compared to the PS4. For instance, as reported by GamesIndustry International, Baird analyst Colin Sebastian is of the opinion that the Xbox One's shipments might be two to three times greater than the PS4.

Hence, it's pretty clear that Flextronics has strong tailwinds behind it and investors are counting on the shipments of these marquee devices to drive revenue.

More growth

In addition to these catalysts, Flextronics' medical, automotive, and defense and aerospace businesses have been providing robust growth. The High Reliability Solutions segment, which includes the above-mentioned businesses, grew 20% in the previous quarter from last year. Flextronics witnessed strong demand from medical and automotive end markets and is on track to exceed $3 billion in revenue in the current fiscal year from this segment.

The Integrated Network Solutions segment, accounting for 44% of revenue, is benefiting from positive trends in telecom and networking. As telecom carriers roll out faster networks in the U.S. and around the world and more data centers are built, this segment should continue to benefit. Telecom equipment makers, such as Ciena, have been delivering terrific results and robust guidance of late and so it is not surprising that Flextronics is also expecting further improvements.

The bottom line

It's clear that investors are more or less correct in being bullish about Flextronics, but at almost 30 times earnings, it is no more a value play. In comparison, rival Jabil Circuit trades at half its multiples; this gives us an idea as to how far investors have bid up Flextronics.

But analysts seem to be pretty optimistic about Flextronics' prospects, and as such, the forward P/E comes down to a very reasonable 9 times earnings. Considering the catalysts that the company has, it may be able to meet expectations going forward.

Hardware, Software, Content, or Services? Where To Invest?

The tech world has been thrown into chaos as the biggest titans invade one another's turf. At stake is the future of a trillion-dollar revolution: mobile. To find out which of these giants is set to dominate the next decade, we've created a free report called "Who Will Win the War Between the 5 Biggest Tech Stocks?" Inside, you'll find out which companies are set to dominate, and we'll give in-the-know investors an edge. To grab a copy of this report, simply click here -- it's free!

The article Can This High-Flying Tech Player Continue to Run? originally appeared on Fool.com.

Harsh Chauhan has no position in any stocks mentioned. The Motley Fool recommends Google. The Motley Fool owns shares of Google and Microsoft. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.