Will This Company Continue to Clean House?

Roomba, Scooba, Braava, Looj, Vero, and Packbot. No, these aren't new dance crazes--rather, they're just a few of iRobot's popular products. These robots vacuum, sweep, and wash floors, clean gutters and pools, and even go on reconnaissance missions for the military. These products are well ahead of their time, and the company's potential is high. However, "potential" is the key word.

Recent performance

In the second quarter, iRobot's revenue jumped 17% to $130.4 million year over year. Net income increased to $8.3 million versus $7.4 million in the year-ago quarter. This growth wasn't just seen domestically, but internationally as well. For instance, domestic revenue improved 25.9%, and international revenue received a 17.7% bump.

Up until this point, it would seem that everything is rosy, and there's reason to be bullish on iRobot. However, while home robot revenue skyrocketed 20% year over year, defense revenue fell 6%. The impressive performance in home robots was mostly due to effective advertising in the domestic market, the introduction of the Braava (floor-sweeping robot) internationally, and the increased availability of the Roomba (floor-vacuuming robot). iRobot shipped 15.5% more Roomba robots than it did in the year-ago quarter.

As you might have guessed, home robots have been the key growth driver for iRobot. Total home robots shipped for the quarter were 492,000, versus 426,000 in the year-ago quarter. This improvement actually holds more weight than some people might realize. Today's consumer is value-conscious, which has led to many consumer goods companies seeing volume declines.

The bad news for iRobot is the weakening performance in defense. In the second quarter, iRobot shipped 424 defense & security robots versus just 42 in the year-ago quarter. However, the average selling price for these 424 units was just $20,000, versus an average selling price of $140,000 in the year-ago quarter. This is because iRobot has shipped more of its more-affordable FirstLook robots.

Selling and marketing expenses increased 24.1% to $22.3 million, another negative. Don't let this sway your opinion or confidence, though; this was a necessary step, as most of the money was put toward marketing and branding. While you might know about iRobot because you follow the stock market, it's not likely that most people you know are even aware of its presence. If you ask them about it, they might ask if you're referring to the movie. Therefore, iRobot must improve its brand recognition, which can only be done through marketing.

iRobot's biggest threat is its competition, which means iRobot must consistently innovative and increase its presence in new and existing markets. The following two competitors are very different in nature, but they reflect iRobot's presence in two different markets.

Cleaning houses and cleaning house

Every home needs to be cleaned. These homes can be cleaned using robots, as previously discussed, or they can be used using more traditional methods, such as with products like Swiffer, Bounty, and Mr. Clean--ust a few of the products that Procter & Gamble offers.

Procter & Gamble is a much larger and more established company than iRobot, making it more of a defensive/dividend-paying play than a growth play. For instance, Procter & Gamble currently trades at 17 times earnings, whereas iRobot trades at 33 times earnings. In other words, if you want growth potential, you're going to have to pay for it. Procter & Gamble also yields 3.10%, whereas iRobot doesn't offer any yield, which is normal for a growth stock. Both companies have displayed quality debt management--iRobot and Procter & Gamble sport debt-to-equity ratios of 0.00 and 0.46, respectively.

On the other end of the spectrum, the defense side, is Northrop Grumman . In his article "Roomba Turns 11: Where Should iRobot Go From Here?," Foolish contributor Steve Symington points out that Northrop Grumman is attempting to steal market share from iRobot with its six-wheeled CUTLASS, an unmanned ground vehicle. However, iRobot's Warrior robot offers more speed and lifting power. These two companies will battle it out with tightly gripped mechanical fists going forward.

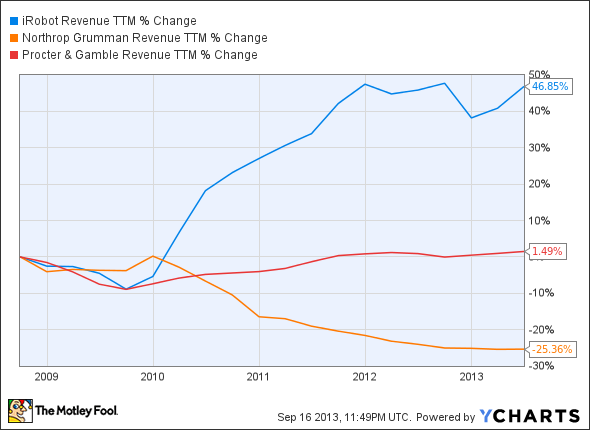

Let's take a look at top-line growth over the past several years for these companies:

IRBT Revenue TTM data by YCharts

And bottom-line growth:

IRBT EPS Diluted TTM data by YCharts

While there are conflicting trends on the top and bottom line, it's easy to determine that iRobot has delivered solid performances on both the top and bottom line, which indicates strong management. Furthermore, investors have shown more interest in iRobot than Procter & Gamble and Northrop Grumman recently:

However, Procter & Gamble and Northrop Grumman yield 3.10% and 2.50%, respectively. Both are also likely to be long-term winners, as they have been for decades.

The bottom line

iRobot might not pay a dividend, but its past innovations prove that it has the potential to become a big player for the military down the road. Imagine getting in on Lockheed Martin before it was a household name? That's the potential of iRobot. Additionally, thanks to iRobot's successes and strong fundamentals, it could be an acquisition target. And even if the defense aspect doesn't pan out and there is no acquisition, iRobot is seeing strong growth in Home Robots.

iRobot is a volatile stock, and considerable downside moves are possible, but long-term potential rewards seem to outweigh downside risks.

The Motley Fool's chief investment officer has selected his No. 1 stock for this year. Find out which stock it is in the special free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

The article Will This Company Continue to Clean House? originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool recommends iRobot and Procter & Gamble. The Motley Fool owns shares of Lockheed Martin. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.