How Investors Missed the Run in Lowe's

The recent quarterly report by Lowe's sent the stock surging to multiyear highs. Most investors were caught off guard, as results from competitors didn't suggest the results would be this strong. So what metric could've helped investors see this strong performance coming?

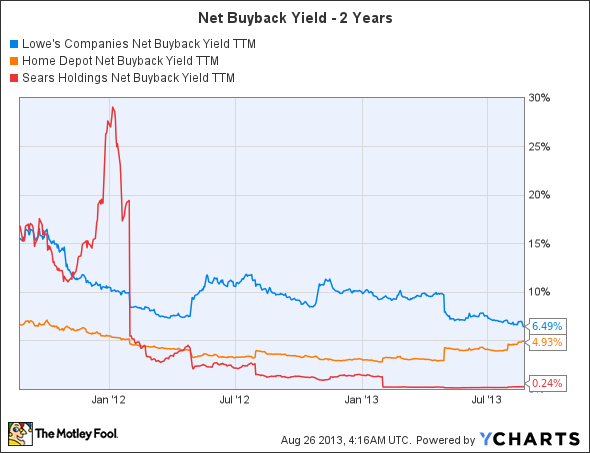

One metric commonly ignored during the weak stock years that began in 2000 and ended with the financial crisis was the net buyback yield. The net buyback yield is calculated by adding the net buybacks over the previous four quarters and dividing by the current market cap. Investors have commonly favored the dividend yield and ignored the buyback as the decade of weak stock results tended to negatively skew the benefits of reducing the share count.

The second-largest home improvement retailer in the world has 1,758 stores in the United States, Canada, and Mexico. The company is only second to Home Depot in the home improvement category and competes against Sears Holdings in many categories, such as appliances. Last year, were investors attracted to the higher dividend with Home Depot looking in the wrong direction? Could investors paying attention to the huge net buybacks at Lowe's have predicted the strong stock rebound over the last year?

Bigger buybacks, bigger returns

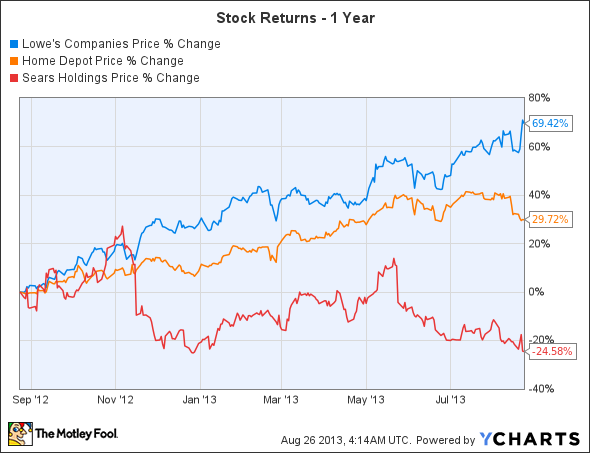

As the chart below shows, Lowe's has had an incredible 70% return in the last year.

The returns easily exceeded the gains from both market leader Home Depot and struggling Sears Holdings. Could anything have predicted these returns? The much-overlooked metric is the net buyback yield. Even with a dividend-focused market over the last couple of years, the lower-yielding Lowe's has easily outperformed the solid dividend of Home Depot. As the chart below shows, Lowe's had a significantly higher net buyback yield during mid-year 2012, but now that yield is shifting back toward an equal rating with Home Depot, suggesting a shift could be taking place.

LOW Net Buyback Yield TTM data by YCharts.

Research shows that the largest net buybacks can outperform the market. Why not glean insights from management's potential signals with share repurchases? The key is that the net buyback has to be of enough scale to signal the value of the stock. The buyback needs to provide a meaningful reduction of shares in the 5 to 10% range to be worth following.

Surprisingly strong results

Aftermarket leader Home Depot reported comps of 10.7%, investors were caught off guard that Lowe's was able to nearly match it with an incredible 9.6% increase in comp sales. Earnings increased an even more incredible 38% as improved margins combined with a lower share count helped boost earnings.

The more crucial part is that Lowe's bought back $1 billion worth of stock in both quarters this year. While solid amounts, the 70% gain in the stock over the last year makes it difficult for the current buybacks to match the greater than 10% net buyback yields from last year. The buybacks would have to increase 70% to keep up with the increased market cap to obtain the same yields.

Home Depot is no slouch

The home improvement retail leader has 2,258 stores and saw revenue increase 9.5% and earnings per share surge 22.8%. Similar to Lowe's, Home Depot is spending a significant amount of capital on share buybacks. However, the company really relaxed the amounts at the end of 2012, with only a net of $1.1 billion spent during the last two quarters. Now though, the company has spent an impressive $4.3 billion in the first two quarters of the year, with the intention of adding another $2.2 billion over the remainder of the year. In total, the buyback yield would equal nearly 6.5%, and combined with the 2.1% dividend yield, it creates an impressive 8.6% returned to shareholders during 2013.

The impressive buyback plan in the first six months of 2013 suggests that Home Depot might be in a financial position to outgain Lowe's over the next year. The lower stock gains during that period and apparent better cash position make the stock more attractive, in my opinion, in comparison to Lowe's.

Reduced buyback signaled Sears weakness

As the net buyback yield chart above showed, Sears had to cut back a significant buyback program that signaled eventual weakness in the stock. Now Sears does compete in other sectors such as clothing that isn't part of the business at Lowe's or Home Depot, but it competes in some of the primary sectors of lawn equipment and appliances. The company though hasn't benefited from the home improvement surge and the cutting of the buyback plan during 2012 was probably the first signal of impending stock weakness.

Clearly, Sears is more of a mixture between a Target and a Lowe's. The recent results suggest it isn't going to benefit from a rebound in housing as originally hoped. The comp sales for second-quarter 2013 were negative and nowhere resembled the strong 10% gains of the home improvement stocks.

Bottom line

Investors not paying attention last year would've missed the huge net buyback yield of Lowe's. A buyback that helped propel the stock 70% higher. Instead of focusing on home sales and economic numbers, investors could let management tell them when a stock is undervalued via a massive buyback. When a company the size of Lowe's can repurchase 10% of the outstanding shares within a year, investors need to consider that the stock is possibly undervalued compared to the cash being generated by the company.

Now the buyback yield is shrinking at Lowe's while Home Depot is gaining altitude just as investors are shifting into Lowe's stock. The sell off in Home Depot presents a buying opportunity and investors should keep an eye on where the yields shift in the next quarter.

Don't Miss These Winners

The retail space is in the midst of the biggest paradigm shift since mail order took off at the turn of last century. Only those most forward-looking and capable companies will survive, and they'll handsomely reward those investors who understand the landscape. You can read about the 3 Companies Ready to Rule Retail in The Motley Fool's special report. Uncovering these top picks is free today; just click here to read more.

The article How Investors Missed the Run in Lowe's originally appeared on Fool.com.

Fool contributor Mark Holder and Stone Fox Capital Advisors own shares of Lowe's and Sears Holdings. The Motley Fool recommends Home Depot and Lowe's. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.