1 Terrifically Positioned Company for Your Portfolio

"The Great Recession" had a big impact on the United States. The stock market lost over half its value from late 2007 to early 2009. Gas prices doubled, and oil spiked to $147/barrel in the summer of 2008. Higher gas led to inflation in other areas such as food. The speed of these spikes had a profound impact on Americans. People began to drive less. Companies like Wal-Mart and McDonald's saw an earnings boost as consumers were driven to their value prices.

Some companies are simply better positioned than others to thrive during rough times. Is Panera Bread terribly positioned? Some analysts feel this company is in a difficult situation. If the economy improves, consumers will leave for more upscale options. If the economy weakens, consumers will flee for more affordable prices. Should investors start worrying?

Really??

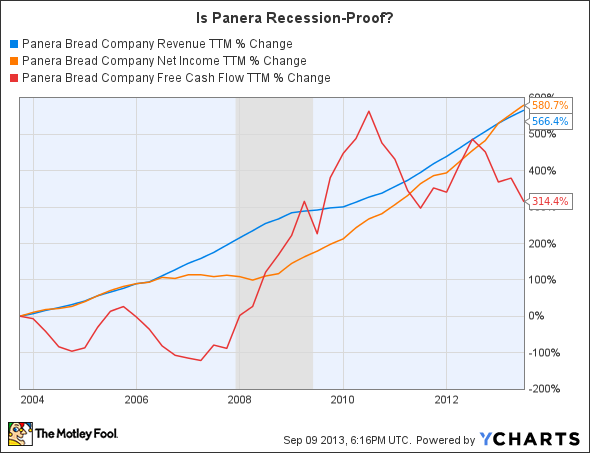

At first, this premise seems logical, but the data doesn't back it up. Below is Panera's chart with the recession highlighted in purple.

PNRA Revenue TTM data by YCharts

As it turns out, Panera has consistently grown revenue, net income, and free cash flow over the past 10 years. Most of these increases were driven by new units as the chain expanded. But perhaps more relevant, same-store sales increased 5.5% in 2008, the heart of the recession. Last year, a good year for the economy, same-store sales were up 6.5%.

History shows us that Panera's customer base grows during hard times, and it grows even faster during good times. Maybe Panera isn't terribly positioned after all.

It's the Segment

Panera operates in the uber-hot fast casual segment. Many fast-casual chains are able to expand at extraordinary rates thanks to the popularity of the segment, and Panera is no exception. At the start of 2009, the company operated 1,252 locations. At the end of last year, it operated 1,652, an increase of 32% in four years. This year the company expects to open 115 to 125 more.

Starbucks is also growing like crazy, not just in the U.S., but around the world. At the start of fiscal 2009, the company operated over 16,600 locations. At the end of fiscal 2012, it operated over 18,000 locations, an increase of 8% in four years.

Yet during this season of growth, Starbucks shut down under performing stores in a repositioning effort. These efforts have brought the company from a dismal 2009, to three straight years of same-store sales increases of 7% to 8% annually. Now positioned for better growth, it expects to operate 20,000 locations by 2014.

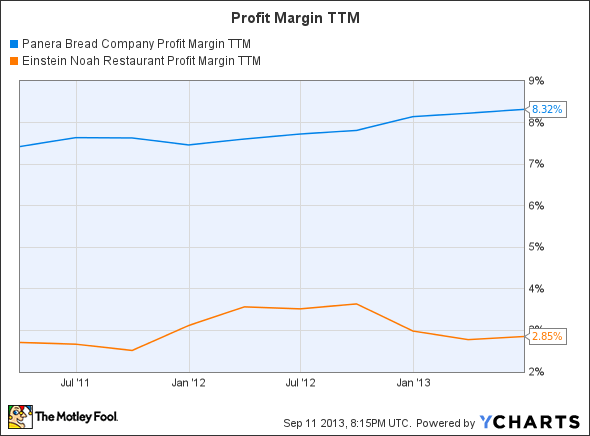

Competitor Einstein Noah Restaurant Group is also growing with plans to expand 10% annually, but same-store sales have been flat. In reality, restaurant traffic was down in the most-recent quarter, but balanced out with a 3% rise in average tickets.

PNRA Profit Margin TTM data by YCharts

With a razor-thin profit margin, Einstein Noah can't afford a decrease in traffic. Medium-term revenue and net income will keep climbing with new units, but over the long term, the company needs same-store sales to improve.

The Balance Sheet

One often overlooked advantage of Panera is its zero-debt position. Not only is the company expanding at an impressive rate, it is doing so with free cash flow. This may not seem significant, but consider that Einstein Noah is projecting interest expenses on its debt to be around $6 million for 2013. Interest expense (just last quarter), affected earnings by about $0.06 per share, or 35% considering earnings per share landed at $0.17.

PNRA EPS Diluted TTM data by YCharts

I see a zero-debt position as a common factor among companies that are creating shareholder value. This strong balance sheet frees Panera from worries such as rising interest rates and dwindling liquidity. In exchange, the company can focus on shareholders by growing earnings and buying back shares.

Conclusion

Economic conditions do impact consumers, but Panera has shown it is not in a terrible position. Rather, it is a terrifically positioned company. It is increasing in popularity, expanding its chain, and has a strong balance sheet, making this company an investment-worthy restaurant. There will always be temporary pressures and moments for concern, but Panera has positioned itself for success for years to come.

Looking for More High-Growth Stocks?

Tired of watching your stocks creep up year after year at a glacial pace? Motley Fool co-founder David Gardner, founder of the No. 1 growth stock newsletter in the world, has developed a unique strategy for uncovering truly wealth-changing stock picks. And he wants to share it, along with a few of his favorite growth stock superstars, WITH YOU! It's a special 100% FREE report called "6 Picks for Ultimate Growth." So stop settling for index-hugging gains... and click HERE for instant access to a whole new game plan of stock picks to help power your portfolio.

The article 1 Terrifically Positioned Company for Your Portfolio originally appeared on Fool.com.

Jon Quast has no position in any stocks mentioned. The Motley Fool recommends Panera Bread and Starbucks. The Motley Fool owns shares of Panera Bread and Starbucks. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.