3 Big Biotech Buyouts of 2013

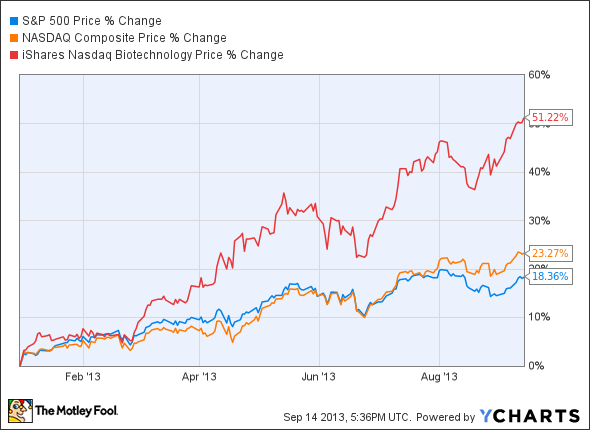

The Chinese calendar says 2013 is the year of the snake, but the market says it's the year of biotech. Major biotechnology ETFs and indices have walloped the broader market by more than 25% since the beginning of the year.

What's fueling the madness? Maturing pipelines, promising late-stage studies, a growing number of IPOs, and, of course, acquisitions. Larger companies looking to replace falling stars in their product portfolios or put their large cash holdings to better use can opt to gobble up a promising firm to inject some optimism into operations for shareholders. We're only three-quarters of the way through 2013, but there have already been several transactions that will have far-reaching implications on the future of the industry.

Acquisition No. 3: Omthera

In May, AstraZeneca bought Omthera for $443 million. AstraZeneca is being hit hard this year by generic competition in various markets to Seroquel, Atacand, and Crestor, so jittery investors are right to worry. After recording total sales of $33.6 billion in 2011, the company notched just $28 billion last year -- and will generate even less this year. Acquiring Omthera gives the company Epanova, a novel fish-oil pill that was shown to lower very high triglycerides and non-HDL cholesterol in combination with a statin, such as Crestor.

If a large-scale cardiovascular trial being planned proves effective in lowering risk of heart attack, AstraZeneca could begin wrestling market share away from Lovaza from GlaxoSmithKline and represent another obstacle for Vascepa from Amarin . Things look promising so far. A 2-gram dose of Epanova has been shown to be comparable to a 4-gram dose of Lovaza.

It may not be that easy, however. There is now a clear path forward for generic versions of Lovaza, which achieved peak sales of more than $1 billion. That could mean trouble for Amarin's Vascepa, which generated sales of just $7.8 million in the first half of this year, and newcomer Epanova. Moreover, several recent studies seem to have found holes in the ability of fatty acid supplements to provide health benefits. Some have even found that the supplements increase the risk of prostate cancer. Will generic competition and new scientific evidence be too much for Epanova to overcome?

Acquisition No. 2: Elan

In July, Perrigo bought Elan for $8.6 billion. While the deal gives Perrigo a big tax advantage each year -- Elan is based in tax-friendly Ireland -- it could also allow the generic-drug maker to expand internationally and even further into biotech. Elan developed Tysabri for treating multiple sclerosis before selling its rights to Biogen Idec earlier this year for $3.25 billion plus royalties of hundreds of millions of dollars per year. Throw in an estimated $150 million in annual tax savings, and Perrigo shareholders could be looking at more than half a billion dollars in extra cash each year for growth initiatives at peak royalties.

The extra loot represents more than 14% of Perrigo's fiscal year 2013 revenue. Unfortunately, outside of tax savings and Tysabri royalties, there are no revenue-generating assets at Elan. That makes the nearly $9 billion deal for just $500 million in annual revenue -- and that's if Tysabri sales continue to ramp -- questionable at best. Such a scenario would represent a 5.8% annual return on the acquisition price, but that puts a lot of faith in Biogen Idec's ability to increase its market share. The likelihood of that occurrence could be why investors sent shares of Perrigo down 7% when the deal was announced. However, assuming Perrigo uses Ireland as a stepping stone for further international expansion, the deal could end up being the most important business decision in the company's history.

Acquisition No. 1: Onyx Pharmaceuticals

In August, Amgen acquired Onyx Pharmaceuticals for $9.7 billion to bolster its oncology program. The deal will also help make up revenue lost from increasing generic competition to Aranesp, Epogen, and Neupogen in the next several years, which could amount to billions in lost revenue for Amgen over the next decade.

The acquisition centers on Onyx's multiple myeloma drug Kyprolis, which is approved for patients who have had at least two prior therapies. Onyx is currently seeking to expand approval to patients who have had just one prior therapy -- a much larger market. Sales of Kyprolis hit $125 million in the first half of 2013, but analysts can see peak sales reaching more than $2 billion per year in the next decade, which would make it well worth the money for Amgen. Think about it: At peak sales, Amgen's nearly $10 billion investment would yield more than 20% per year. I'll go out on a limb and say the company wasn't getting that by just sitting on a pile of cash.

Foolish bottom line

One of the biggest advantages with acquisitions in the biotech industry is the ability to maximize the potential of new products. Investors have to think that larger companies such as AstraZeneca and Amgen can guide Epanova and Kyprolis to more successful futures than the smaller, less-experienced companies that developed them. Moreover, these deals will change the landscape of the industry by rearranging product portfolios, drawing new lines in the sand between competitors, and eventually (that's the hope, anyway) adding to free cash flow -- opening up future growth opportunities.

You may not have billions of dollars to buy your own biotech company, but you, too, can make money by investing in great companies. You have to play to win, though. Millions of Americans have waited on the sidelines since the market meltdown in 2008 and 2009, too scared to invest and put their money at further risk. Yet those who've stayed out of the market have missed out on huge gains and put their financial futures in jeopardy. In our brand-new special report, "Your Essential Guide to Start Investing Today," The Motley Fool's personal finance experts show you why investing is so important and what you need to do to get started. Click here to get your copy today -- it's absolutely free.

The article 3 Big Biotech Buyouts of 2013 originally appeared on Fool.com.

Fool contributor Maxx Chatsko has no position in any stocks mentioned. Check out his personal portfolio or his CAPS page, or follow him on Twitter, @BlacknGoldFool, to keep up with his writing on energy, bioprocessing, and biotechnology.The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.