UPS Fights Against Industry Headwinds

UPS is seeing strength in some areas, but it might not be enough to keep this stock-appreciation machine running.

Strengths and weaknesses

UPS must have at least some love for today's consumer, since buying products online has become so popular. Small package deliveries have been the company's strength recently, with business-to-consumer shipments jumping 5% in the second quarter year over year. With business-to-consumer shipments representing 40% of U.S. domestic packages, this has significantly aided ground operations.

On the other hand, business-to-business volume was flat in the second quarter, and volume for air products declined 5%. With fierce competition, a slow U.S. economy, weak export growth, lackluster industrial production, and low inventory replenishment levels, UPS is having a difficult time on the commercial side.

Internationally, Asia and Europe are showing volume growth, but customers are opting for more affordable delivery products. With austerity in Europe and slowing growth in China, this should come as no surprise. It also tells us that the value-conscious consumer isn't just found in the United States, but in most large economies throughout the world. This, in turn, is what has led many global companies, regardless of the industry, to cut costs and buy back their own shares in order to improve their bottom lines. If top-line growth slows, then it must be made up for in other areas.

UPS is attempting to improve its operational efficiency. One way it's doing so is by taking full advantage of its newly expanded operating facilities through its international package segment. By utilizing these facilities, UPS will have an opportunity to adjust its transportation network while also improving its delivery times in each region.

Top-line performance

Revenue improved 1.2% to $13.51 billion in the second quarter year over year, but operating expenses grew at a faster 1.8% clip to $11.77 billion. All the headwinds listed above combined with fuel pressures makes this a challenging environment for a company like UPS. While you can read all the detailed information above and below, if you would prefer to keep it simple, it comes down to customers choosing more affordable delivery package options because their wallets are tight.

Last December, UPS increased its base rates by 6.5% for UPS Next Day Air, UPS 2nd Day Air, and UPS 3 Day Select, and it upped its base rate for UPS Ground by 5%. It might seem as though this was done on purpose in order to compensate for lower volumes, but these are annual increases. Regardless of whether they're intentional or not, they have the potential to drive revenue higher. The tricky part is whether or not loyal customers will become fed up and opt for another service. Considering that speed is essential in the business world, UPS isn't likely to lose a lot of customers due to base rate escalations.

Bigger is sometimes better

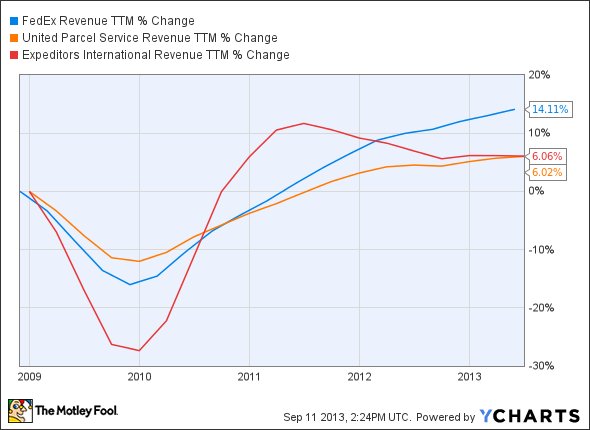

UPS is often compared to FedEx . However, UPS is a much larger company, sporting a market cap of $82.65 billion, versus a market cap of $35.26 billion for FedEx. Despite the differences in size, these two companies tend to perform and trade together. The same can be said for the smaller (market cap of $9.15 billion) and more logistics-focused Expeditors International of Washington . Consider the following revenue growth trends:

FDX Revenue TTM data by YCharts

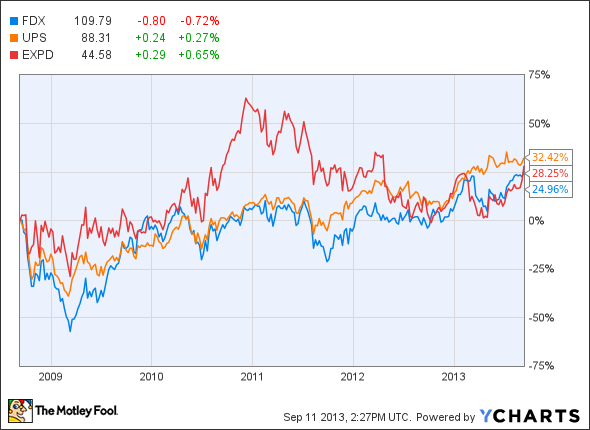

Also take into account the the stock performance comparisons:

Since UPS often trades along with the industry, key metrics and dividends play a big role:

METRIC | Trailing P/E | Net Margin | ROE | Dividend Yield | Debt-to-Equity Ratio | Short Position |

|---|---|---|---|---|---|---|

UPS | 102 | 1.52% | 14.60% | 2.90% | 3.31 | 2.30% |

FedEx | 23 | 3.53% | 9.72% | 0.60% | 0.17 | 2.20% |

Expeditors | 27 | 5.78% | 16.56% | 1.40% | 0.00 | 3.00% |

Source: company financial statements

UPS offers a decent ROE and an impressive yield, but when considering the strong net margins and better debt management of peers, it might not be worth paying up for UPS. Despite Expeditors being the smallest of the three, it's the most impressive on a fundamental basis (at the moment), and it has proven to be the most resilient to market corrections (see chart above).

Conclusion

UPS is facing several challenging headwinds, and this might limit the company's potential in the near future. However, UPS has established a fortified position in the package delivery market, and barring an unforeseen catastrophe, it's going to be around for a very long time. While the stock would suffer if the broader market corrects, you can simply add to your position at lower levels. Since UPS is a shareholder-friendly company, you can also collect dividends in the meantime, but you should use caution if you plan on initiating a position now.

The Motley Fool's chief investment officer has selected his No. 1 stock for this year. Find out which stock it is in the special free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

The article UPS Fights Against Industry Headwinds originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool recommends FedEx and United Parcel Service. The Motley Fool owns shares of Expeditors International of Washington. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.