This Airline Is Too Risky for a Long-Term Investment

JetBlue investors, remember these names: Albuquerque, Philadelphia, Medellin, Worcester, Port-au-Prince, and Lima. By the end of 2013, JetBlue will have added all these cities to its routes; the first three are already active, alongside new routes to JetBlue's existing cities. All these moves carry great growth potential for the company -- but the other obstacles JetBlue's facing should curb investors' potential enthusiasm.

Increased costs

In addition to a sluggish macroeconomic environment, JetBlue has to contend with increased costs from maintaining and repairing its aging fleet. Assuming fuel prices average $3.13 per gallon, JetBlue expects cost-per-available seat mile to jump 2.5%-4.5% in 2013.

Salaries, wages, and benefits are also expected to increase by approximately 6%. JetBlue's longer-tenured workers demand higher salaries, and the company's trying to keep its pay competitive to retain its best talent.

Between these two factors, JetBlue's total operating expenses jumped 7.5% ($86 million) in the second quarter year over year.

The good news

Before this news gives you the blues, remember to look on the bright side. JetBlue has now delivered 13 consecutive profitable quarters. It also generated $402 million in cash in the second quarter, $152 million of which it used to pay down its debt. By reducing the interest on its debt payments, JetBlue will be able to seize more growth opportunities.

Currently, JetBlue sports a debt-to-equity ratio of 1.46, which is below the industry average of 2.0. This is more impressive than the debt-to-equity ratio of 9.83 for United Airlines , though not quite as impressive as Southwest Airlines' 0.44.

United Airlines and Southwest Airlines seem to be heading in opposite directions. United Airlines might be the largest airline in the United States, but considering how challenging this industry gets, that size and scale only means more problems.

Consider some key metric comparisons for these three airlines:

METRIC | Forward P/E | Net Margin | ROE | Dividend Yield | Short Position |

|---|---|---|---|---|---|

JetBlue | 10 | 1.87% | 5.09% | None | 23% |

Southwest Airlines | 11 | 2.19% | 2.19% | 1.20% | 2% |

United Airlines | 6 | (1.51%) | (-39.41%) | None | 9.83% |

Source: Company financial statements.

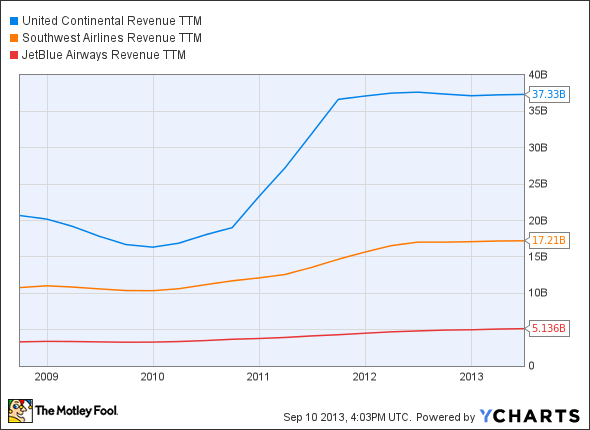

Looking at these numbers, it's clear that United Airlines isn't likely to offer a better investment opportunity than JetBlue or Southwest Airlines at this point in time. If you're still not sold on this point, then consider annual revenue and EPS comparisons.

UAL Revenue TTM data by YCharts

JBLU EPS Diluted TTM data by YCharts

Though United Airlines is the largest of the three, its top-line growth slowed considerably in 2012, and it swung to a loss on the bottom line.

While JetBlue has delivered healthy top-line growth over the past several years, one statement in its last 10-Q was somewhat concerning: "Although we have experienced revenue growth in 2013, this may not continue."

That statement doesn't guarantee anything, and it could just be JetBlue underplaying its potential, but it certainly doesn't exude confidence.

Good news/bad news

In the second quarter, JetBlue's revenue came in at $1.34 billion vs. $1.28 billion in the year-ago quarter. On the other hand, average fare declined 1.3% to $157.51. Average fare is an important metric, since it's similar to comps (or same-store sales) in the retail sector. It indicates organic growth minus any new additions to help aid that growth.

A telling chart

JetBlue and Southwest Airlines are both known for their top-notch customer service and overall positive experiences. However, both are dealing with weak macroeconomic trends and volatile fuel prices, and JetBlue is seeing increased costs. These factors make long-term stock performance trends for airlines even more concerning. Consider the 10-year chart below:

Conclusion

JetBlue is a fundamentally sound and well-run company. It's simply in an industry that must constantly deal with stiff headwinds, making consistent top and bottom-line growth difficult to come by. This, in turn, makes life frustrating for investors. While JetBlue has the potential to reward shareholders via a short-term trade, it's not a route you want to take if capital preservation is one of your top priorities.

This incredible tech stock is growing twice as fast as Google and Facebook, and more than three times as fast as Amazon.com and Apple. Watch our jaw-dropping investor alert video today to find out why The Motley Fool's chief technology officer is putting $117,238 of his own money on the table, and why he's so confident this will be a huge winner in 2013 and beyond. Just click here to watch!

The article This Airline Is Too Risky for a Long-Term Investment originally appeared on Fool.com.

Dan Moskowitz has no position in any stocks mentioned. The Motley Fool recommends Southwest Airlines. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.