This Best of Breed Stock Looks Set to Scale Greater Heights

Apparel retailers have been in the midst of a bloodbath of late, but Urban Outfitters has stood tall. While others such as Abercrombie & Fitch and teen retailer Aeropostale have been facing stiff competition from cheaper and more trendier brands, Urban Outfitters' strategy of listening to the consumer and promoting sales through various channels have helped it perform well.

Swimming against the current

The company saw an impressive 9% increase in same-store sales in the second quarter. More importantly, Urban Outfitters' revenue increased 12% from the year-ago period while net income jumped 25%. These results are very impressive as both Abercrombie and Aeropostale had seen substantial drops in both earnings and revenue in their respective quarters.

Urban Outfitters saw growth across all its brands and gross margin improved 169 basis points in the previous quarter. This is undoubtedly a strong showing by the company, but given the expansionary moves and sales-driving strategies that Urban has in place, it can continue to pull ahead of peers.

Expansion on the cards

Urban Outfitters plans to open 35 to 40 new stores during the year and it has also been opening branded shops at Nordstrom stores. After its first branded shop at Nordstrom's downtown Seattle location turned out to be a success, Urban Outfitters has opened another nine stores this year.

The advantage with these branded shops is that they carry a wider product assortment. They have delivered productivity increases as well and that's why Urban Outfitters has lined up several such stores for the remainder of the year.

Apart from opening physical stores, Urban Outfitters' focus on strengthening its direct-to-consumer business has also been reaping results. Direct-to-consumer traffic grew 16% in the previous quarter while conversion rate of visitors also improved 51 basis points. Direct orders grew 40% in the previous quarter and there's huge potential going forward as well.

Urban Outfitters now ships to more than 120 countries from its distribution centers in the U.S. and the U.K. Hence, the company has a pretty big market to explore and management stated that they are investing in this channel to drive further gains.

Smart strategies

Apart from expanding its reach, Urban Outfitters is also focused on staying up to speed with fashion trends. The company is looking to expand its offerings to offer more choices to customers and also plans to enter into licensing partnerships to boost sales. Management is already in negotiation with several companies regarding a partnership.

Urban Outfitters also has a well-laid out strategy of keeping customers engaged. For instance, for its Free People brand, the company regularly updates its female customers regarding the latest products through its blog, catalogs, website, events, videos, and social media. These strategies seem to be working well for the company as same-store sales at Free People had jumped 38% in the previous quarter.

A justified premium

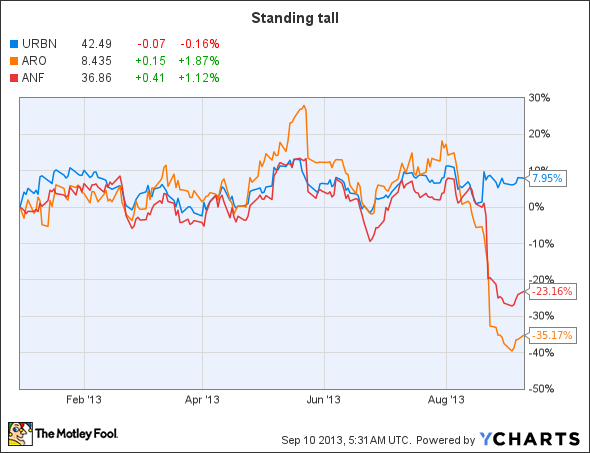

Considering Urban Outfitters' recent performances and robust growth plans, it isn't surprising to see that the company commands a premium over its peers. A trailing earnings multiple of 23.5 is no doubt expensive when stacked against Abercrombie's trailing P/E of 12 while Aeropostale isn't profitable on a trailing twelve month basis. A comparison of stock price performances so far this year shows that Urban Outfitters is the best of the lot.

Buying Urban Outfitters is probably the best option here as there's not much sense in buying companies that have been beaten-down badly and whose recent results are a red flag. Abercrombie had crashed 18% after the company's earnings and revenue dropped in the previous quarter. The decline in same-store sales stood at an ugly 10%.

Abercrombie management expects same-store sales to decline further in the ongoing quarter. This doesn't make for a good reading since the company has seen comps decline for six quarters on the trot.

On the other hand, Aeropostale has been the worst performer of the lot this year. The company's same-store sales had declined a staggering 15% in the previous quarter.

Aeropostale struggled due to what it called a "challenging teen retail environment with weak traffic trends and high levels of promotional activity." In simple words, the company is struggling to attract teens to its stores as its merchandise has failed to click.

The bottom line

Given the challenging situation faced by peers, Urban Outfitters' performance is undeniably terrific. That's the reason why the company's shares command a premium. Considering the growth strategies that Urban Outfitters has in place, its string of impressive performances would most likely continue.

Tired of watching your stocks creep up year after year at a glacial pace? Motley Fool co-founder David Gardner, founder of the No. 1 growth stock newsletter in the world, has developed a unique strategy for uncovering truly wealth-changing stock picks. And he wants to share it, along with a few of his favorite growth stock superstars, WITH YOU! It's a special 100% FREE report called "6 Picks for Ultimate Growth." So stop settling for index-hugging gains... and click HERE for instant access to a whole new game plan of stock picks to help power your portfolio.

The article This Best of Breed Stock Looks Set to Scale Greater Heights originally appeared on Fool.com.

Harsh Chauhan has no position in any stocks mentioned. The Motley Fool recommends Urban Outfitters. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.