Coming Storm in the Restaurant Sector?

What if one of the simplest sectors, the restaurant sector, was about to be turned on its head? According to the NPD group, in September 2012 there were 616,008 restaurants in the United States. Factor in the US population size and you get roughly one restaurant for every 510 people, seemingly a very saturated market. The entire restaurant sector grew a measly 0.7% year over year, but one segment crushed this statistic. This segment grew near 6%, and in coming years may change the restaurant industry as we know it.

It's called fast casual

It's no secret that I'm talking about the fast casual segment. Fast casual is estimated to account for 27% of total food service sales. Investors have become more familiar with this trend ever since Chipotle went public in 2006. Since the IPO, the company's revenue is up over 300%, and net income over 900%.

Here's the catch: with the restaurant sector as mature as it is, fast casual's success means someone else'sdemise. According to Technomic, two of the fastest fading restaurant segments are diners and buffets. "America's Diner" Denny's has felt this pressure for years.

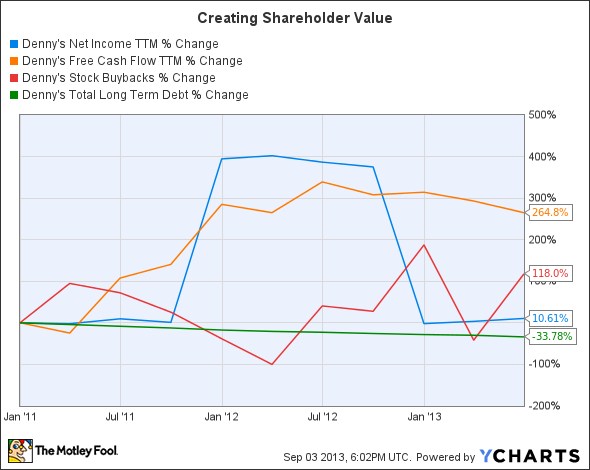

To offset an eroding customer base, Denny's decided to restructure in 2007. At the time the company was 66% franchised and 34% company owned. It has since sold many locations to franchises to make the split 90/10. This restructuring, now complete, has naturally led to a 40% decrease in revenue since 2007, but Denny's net income and free cash flow are improving.

Denny's is using an improved cash position to return value to shareholders.

DENN Net Income TTM data by YCharts

Despite Denny's best efforts, it's tough to remain optimistic about growth. Last quarter, only one franchised restaurant opened (net). Comp-sales were barely positive, and are predicted to be flat going forward. Denny's has done well considering it's in the dying diner segment, but it just doesn't offer investors the same opportunity that some fast casual joints offer.

Open the IPO Floodgates

Tex-Mex chain Chuy's had a very successful IPO in July 2012. Three months ago Noodles & Company debuted with a strong IPO of its own. Both IPOs priced at the top of their range and are currently crushing the S&P 500, up 108% and 150% respectively. While many fast casual chains are still young, these recent successes seem to be luring more chains toward the IPO waters.

On August 29, Potbelly Sandwich Shop, a Chicago-based chain with 286 locations, filed a preliminary prospectus. Focus Brands, parent company to Moe's Southwest Grill, appears to be working toward an IPO also. The uber-popular Smashburger just hired firms to form a strategy for capital growth.

This could be the start of a larger trend: IPOs from fast casual chains with stratospheric growth targets.

Chain | Current Locations | Growth Target | Percentage |

Chipotle | 1,502 | 3,000-4,000 | 99%-166% |

Chuy's | 45 | 500 | 1,011% |

Noodles | 348 | 2,500 | 618% |

Potbelly | 286 | 10%/year | n/a |

Smashburger | 200 | 1,500* | 650% |

*No target has been given by the company. This seems like a reasonable estimate, based on competitor Five Guys' current size.

As these chains expand further, other restaurants are going to start feeling the heat that Denny's has already experienced. Many see quick service as fast casual's natural competitor, but the data doesn't support this.

The same report from the NPD group claimed that of the 4,442 restaurants opened during the year leading up to September, the majority were fast food restaurants. Quick service easily outpaced full service, which leads me to believe the next segment to feel fast casual's pressure is the full service segment.

Leaner and Meaner

As fast casual encroaches on full service restaurant territory, the question becomes who is better positioned for the revenue battle? Increased revenue for existing full service chains is going to come primarily from comp-sales. Increased revenue for newer fast casual chains will come mainly through new locations.

You may be inclined to think that fast casual chains are setting unit goals too high. Yet these chains are growing more popular and they have strong balance sheets coupled with high amounts of free cash flow. With the efficiency of these companies, it becomes difficult to foresee anything that would keep them from hitting their goals.

As fast casual restaurants hit growth targets, full service will likely experience comp-sales pressure. Darden is well aware of the threat these newer chains pose, but a diverse portfolio works in its favor. By being in steak, Italian, seafood, and even beer with the acquisition of Yard House, the company seems to have a large enough moat to weather the storm. Although Darden's earnings per share was down 12.3% for 2012, it still increased its dividend payout by 10%.

Conclusion

Fast casual is taking the restaurant sector by storm. Many segments are already feeling the heat, and will only continue to be pressured as fast casual chains grow at breakneck speed. Some traditional chains, like Darden, will continue to thrive. For others, like Ruby Tuesday, the outlook looks bleak.

Both Noodles and Chipotle are among the best managed in the fast casual segment, but I'm eagerly awaiting Potbelly's IPO. After reading its prospectus, I'm convinced it's a rare opportunity. I intend to buy on the first day if its valuation is reasonable.

Profiting from our increasingly global economy can be as easy as investing in your own backyard. The Motley Fool's free report "3 American Companies Set to Dominate the World" shows you how. Click here to get your free copy before it's gone.

The article Coming Storm in the Restaurant Sector? originally appeared on Fool.com.

Jon Quast has no position in any stocks mentioned. The Motley Fool recommends Chipotle Mexican Grill. The Motley Fool owns shares of Chipotle Mexican Grill and Darden Restaurants. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.