Higher Oil Prices Will Not Help Everyone

The energy world is fixated on the price of oil, but not all upstream firms benefit from price increases. Between futures, options, swaps and other techniques, there are many ways that a firm can remove pricing volatility from its bottom line. In the long run higher oil prices help the industry by making more expensive fields worth developing, but in the short run there are only a limited number of firms that benefit from volatile prices.

The volatile players

Smaller upstream companies are often the first firms to be affected by higher prices. Chesapeake is a good example of what can happen when you try to play the energy market. In 2011, they decided to remove a number of their natural gas hedges in anticipation of higher prices. In the end higher prices did not come when management expected. A lack of effective hedges helped to drive Chesapeake's 2012 earnings per share down to a loss of $1.45 and cause difficult asset sales.

Hindsight is 20-20, but the company's large debt load should have obvious that it was making a very imprudent decision. After firing its CEO and organizing a number of management changes, it appears that Chesapeake has grown up. In the second half of 2013 it has around 94% of its oil production hedged to the downside at $95.64 per barrel and 79% of its natural gas production at $3.70 per million British thermal units, or mmbtu.

If the oil market temporarily crashes, the firm's downside hedges will protect its income and dividend payment. A longer term price decline is a different story. The company still has high a total debt to equity ratio of 1.02, meaning that a sustained downturn would force further asset sales and put its dividend in danger.

EOG Resources is a major shale driller with operations in the Permian Basin, Eagle Ford and the Bakken region. This company is a strong producer of oil, allowing it to avoid much of the pain that Chesapeake had to endure in recent years. Being active in a number of Texan fields allows EOG to save on transportation costs and get a better bang for its buck.

A quick look at EOG Resource's latest 10-Q shows that based on its crude and condensate production levels, it is around 58.8% hedged with crude oil futures until the end of September at $98.80 per barrel and 55% hedged from the beginning of October until the end of 2013 at $98.84 per barrel.

On the surface the company looks like it is in a riskier position than Chesapeake, but it is important to take into account both firms' debt loads. EOG Resources has a total debt to equity ratio of 0.44, substantially less than Chesapeake's. EOG Resources is also able to endure more volatility without worrying about meeting interest payments. Not only is the company in a better position to profit from rising oil prices, it is already profitable thanks to oil-rich acreage.

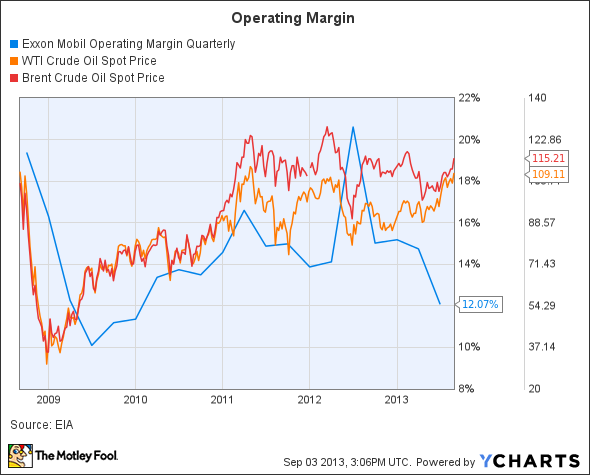

XOM Operating Margin Quarterly data by YCharts

ExxonMobil makes an effort not to use derivatives. Being the large integrated oil company that it is, it can use its downstream and upstream operations in tandem to stabilize cash flow. After the crash in 2008, oil prices only had to reach $70 before the company's margins went back up.

The above chart shows that while ExxonMobil's operation margin has usually stayed within 14% to 16% over the past couple years, it recently took a turn for the worst. Its downturn to 12.07% was driven by increased refinery maintenance. While the firm is used to having 4% to 5% of its refinery capacity offline for maintenance, in the last quarter it reached 9%. Management expects this to be a onetime event, so in the next quarter's margins should be back to the historical norm.

Don't expect recent price volatility to have a big impact on ExxonMobil. Even if the price spikes above $130, its refineries will be stuck paying for more expensive crude and cancel out most of the increased downstream income. On the positive side its debt load is very low with a total debt to equity ratio of 0.12, meaning that the company can easily endure short term volatility.

Conclusion

Instability in the Middle East is sending oil prices upward, but it is hard for big companies to benefit from such short-term price increases. ExxonMobil's refining operations face higher crude oil costs, putting a damper on profits. Chesapeake is working hard to boost its crude oil and NGL output, but its high debt load means that it cannot afford to truly expose itself to price volatility. EOG Resources is another story. It has a smaller debt load, and only a portion of its crude production is hedged. If you are looking for a safer way to profit from rising prices, EOG Resources it is a better bet.

Think the days of $100 oil are gone? Think again. In fact, the market is heading in that direction now. But for investors that are positioned to profit from the return of $100 oil, it can't come soon enough. To help investors get rich off of rising oil prices, our top analysts prepared a free report that reveals three stocks that are bound to soar as oil prices climb higher. To discover the identities of these stocks instantly, access your free report by clicking here now.

The article Higher Oil Prices Will Not Help Everyone originally appeared on Fool.com.

Joshua Bondy has no position in any stocks mentioned. The Motley Fool has the following options: long January 2014 $30 calls on Chesapeake Energy. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.