Statistically You Already Own at Least 1 of These Kitchen Stocks

Peter Lynch's most famous investment principle is to "invest in what you know." New investors always hesitate to make their first stock purchases when the answer is often staring right at them, right in their own kitchens. The kitchen is the perfect place to start because there is a very good chance that what's in your kitchen is not the exception, but the norm. The cyclic and predictable nature of kitchen-related purchases also provides a reliable revenue stream for the top companies in this segment.

Statistically, you already own at least one of the following 'kitchen stocks,' either through direct purchase, your company's 401K plan, or one of the hundreds of S&P 500 mutual funds. These are safe picks, but they are also not dinosaurs since they are still growing.

On your kitchen counter tops...

Do brands like Sunbeam, Oster, Mr. Coffee, Crock-Pot, or FoodSaver ring a bell? These are some of the 100-plus brands within the portfolio of global consumer- products company Jarden (NYSE: JAH).

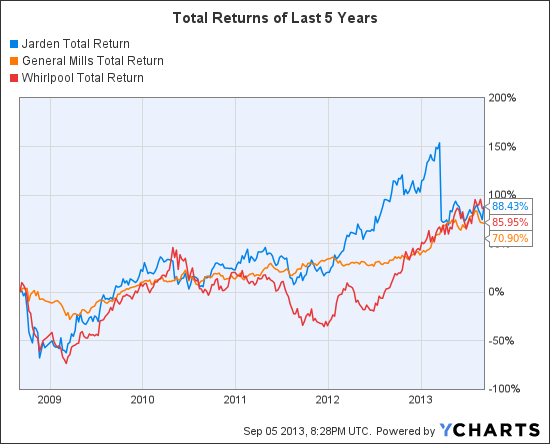

The company did a three-for-two split in March and is up 32% year-to-date. Despite the countless number of kitchen-appliance accessory infomercials that create the illusion of a fragmented and competitive market, Jarden has dominated the industry for over a decade. Jarden's 34% compound annual growth rate in net sales and 350%-plus stock appreciation has put the company in the 15th spot in the Fortune 500 for total rate of return to shareholders over the last 10 years.

Jarden's second-quarter earnings revealed record net sales of $1.8 billion, although net income declined to $76.4 million from $83.2 million a year ago. The company is susceptible to changes in its leading outdoor segment, where it currently targets sporting and camping opportunities. Football and baseball accessories, for example, may be negatively affected in the coming years as more safety is required for each sport, which may open the door to improved helmets and bats from Jarden's competitors. Camping may also be affected, because younger people are becoming increasingly sedentary with social networking, video games, and other indoor activities.

Nevertheless, Jarden still has opportunity in several areas. It has been growing globally over the past decade, now with 39% of sales currently outside of the US. It has no direct competition despite private companies like Hamilton Beach competing in the kitchen-consumables segment.

Last quarter, Hamilton Beach's net income was just $2 million on revenue of $110.7 million. Additionally, successful brands like Mr. Coffee can accelerate sales as Jarden can now offer K-Cup-machine alternatives at prices much lower than Green Mountain Coffee Roasters' Keurig products.

In your kitchen cupboards...

General Mills (NYSE: GIS)has beaten the S&P 500 consistently in the past five, 10, 20, and 30 year periods by a significant margin. Not many companies have been this consistent for this long. General Mills has also delivered regular dividends to shareholders for 114 years and counting, without interruption or reductions. After existing for over a century, General Mills is often considered a boring stock with no growth potential. However, there is more to General Mills than colorful cereal boxes.

The FY 2013 earnings showed that net sales grew another 7% to $17.8 billion, with new businesses contributing much of the gains. I believe General Mills has more room to run and is one of, if not the best, defensive plays in your kitchen.

Wal-Mart Stores reported disappointing earnings last quarter, which affected big-ticket items. Wal-Mart is by far General Mills' largest retail purchaser, accounting for 31% of all U.S. sales. The silver lining is that Wal-Mart's poor earnings did not affect General Mills' bottom line.

General Mills' opportunities go beyond international growth. I believe a big acquisition is due since its last large purchase/merger was with Pillsbury back in 2001 despite gaining a controlling stake in Yoplait in 2011. I wouldn't be surprised if General Mills adds a ready-to-eat meat company or healthy drink brand to its portfolio.

Stoves, refrigerators, dishwashers, oh my!

Whirlpool's (NYSE: WHR) biggest competition for years was Maytag, until it bought the appliance giant in 2006. Since then, Whirlpool's stock has nearly doubled despite the 2009 Great Recession. Within the U.S. market, Whirlpool has been a consistent leader with over 40% market share and 2012 sales of nearly $18 billion.

Whirlpool also has a solid brand name and reputation, in addition to growing net earnings and revenue. It holds a top-10 spot in J.D. Power and Associates' ranking for overall customer satisfaction in dishwashers and refrigerators. The trends that favor the appliance powerhouse are even more important than customer rankings.

First, Whirlpool's sales are increasing in every region of the world because of improved margins. On a historical basis, it actually saw less revenue last year than in 2008 ($4.7 billion versus $4.9 billion), but net earnings improved due to margins nearly doubling. Surging construction in the housing market will also benefit Whirlpool as new major appliances are installed. Construction of new apartments surged 26% in July. I wouldn't be surprised if this surge shows up on Whirlpool's bottom line in the next few quarters.

JAH Total Return Price data by YCharts

Final thoughts

"Investing in what you know" should be taken one step further. Instead, "invest in what you use often." The kitchen is a great place to start. Whether you eat out most of the time or don't eat much at all, there is a good chance you have a toaster or an oven -- used or unused.

At least one of your kitchen appliances is likely made by either Jarden or Whirlpool. While General Mills is usually seen as a one-dimensional cereal company by the general public, its portfolio includes much more. In the end, all three companies are great starting points for the novice investor.

Dividend stocks can make you rich. It's as simple as that. While they don't garner the notoriety of high-flying growth stocks, they're also less likely to crash and burn. And over the long term, the compounding effect of the quarterly payouts, as well as their growth, adds up faster than most investors imagine. With this in mind, our analysts sat down to identify the absolute best of the best when it comes to rock-solid dividend stocks, drawing up a list in this free report of nine that fit the bill. To discover the identities of these companies before the rest of the market catches on, you can download this valuable free report by simply clicking here now.

The article Statistically You Already Own at Least 1 of These Kitchen Stocks originally appeared on Fool.com.

Michael Carter has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.