Is Chevron Destined for Greatness?

Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does Chevron fit the bill? Let's take a look at what its recent results tell us about its potential for future gains.

What we're looking for

The graphs you're about to see tell Chevron's story, and we'll be grading the quality of that story in several ways:

Growth: are profits, margins, and free cash flow all increasing?

Valuation: is share price growing in line with earnings per share?

Opportunities: is return on equity increasing while debt to equity declines?

Dividends: are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's take a look at Chevron's key statistics:

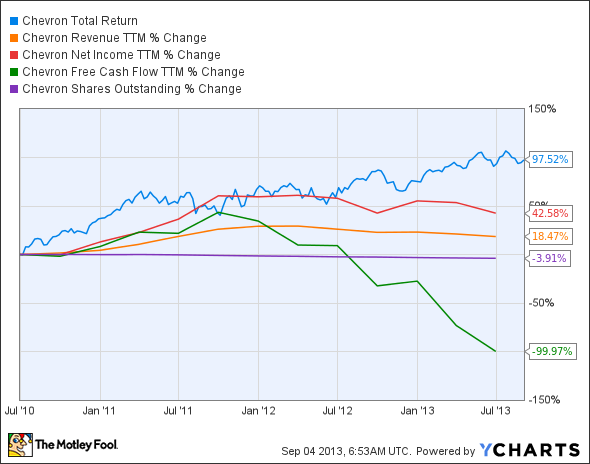

CVX Total Return Price data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 18.5% | Fail |

Improving profit margin | 20.4% | Pass |

Free cash flow growth > Net income growth | (100%) vs. 42.6% | Fail |

Improving EPS | 47.1% | Pass |

Stock growth (+ 15%) < EPS growth | 97.6% vs. 47.1% | Fail |

Source: YCharts. * Period begins at end of Q2 2010.

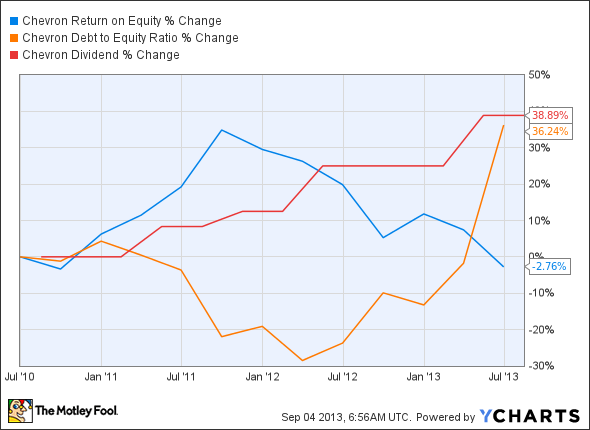

CVX Return on Equity data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | (2.8%) | Fail |

Declining debt to equity | 36.2% | Fail |

Dividend growth > 25% | 38.9% | Pass |

Free cash flow payout ratio < 50% | Really high ** | Fail |

Source: YCharts. * Period begins at end of Q2 2010.

** Chevron's trailing 12-month free cash flow is $3 million, effectively zero at this scale.

How we got here and where we're going

Chevron doesn't come through with flying colors, as it mustered only three out of nine possible passing grades. One main source of that weakness is falling free cash flow, which has diverged significantly from net income over the past three years, and which may not be able to sustain dividends at the present level. In addition, the company raised a chunk of new long-term debt in 2012, which reflects badly in our analysis. Will Chevron be able to move past these weaknesses, or is the oil and gas supermajor drilling a dry hole for investors today? Let's dig a little deeper to find out.

News of a possible military strike on Syria has forced Chevron and other oil companies to abortunder way projects in the region recently. Although Syria is small producer of oil compared to other Middle Eastern countries, rising tensions and potential imbalance are seen as probable disruptions to oil outflow in the Middle East. In the past few days, the anticipated Syrian crisis has already sent crude oil and natural gas prices soaring, which could more than offset the reduced output from aborted projects in the near term.

Fool contributor Dan Carroll notes that Chevron has also recently pulled out a liquefied-natural-gas project in Nigeria after enduring delays. However, the company should continue to expand its geographical presence in resource-rich Africa -- at least once crucial Middle Eastern shipping lanes again appear relatively safe.Chevron isn't alone in its withdrawal from Middle Eastern projects -- rival ExxonMobil recently reduced its stake in an Iraqi field due conflicts between the Baghdad and Kurdish governments.

On the other hand, ExxonMobil recently acquired Celtic Exploration for $2.6 billion, and has bought up 226,000 acres of unconventional oil assets from ConocoPhillips in Athabasca, Canada for a price of $720 million. Going forward, Chevron has also been aggressively leveraging its non-conventional oil reserves, as it made an agreement with Argentine-government-controlled YPF to gain access to shale oil reserves located in Vaca Muerta in Argentina. The race is on to control promising fields in relatively safe locations.

Fool analyst Joel South notes that United States' oil and nat-gas production levels are moving up, but the industry is saddled with high capital expenditures, which crimp even the largest companies' ability to make any big domestic moves. The domestic oil-directed rig count also saw a significant decline due slowing drilling activities in the latest quarter. However, Chevron's efforts to go midstream with its Angola pipeline project should pay off in the near future. The company's Gorgon facility is also 67% complete.

Putting the pieces together

Today, Chevron has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

Imagine a company that rents a very specific and valuable piece of machinery for $41,000... per hour (that's almost as much as the average American makes in a year!). And Warren Buffett is so confident in this company's can't-live-without-it business model, he just loaded up on 2.19 million shares. An exclusive, brand-new Motley Fool report reveals the company we're calling OPEC's Worst Nightmare. Just click HERE to uncover the name of this industry-leading stock... and join Buffett in his quest for a veritable LANDSLIDE of profits!

The article Is Chevron Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes has no position in any stocks mentioned. The Motley Fool recommends Chevron. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.