This Railroad Company Is Chugging Along Nicely

Railroad company CSX has done very well this year, with its stock gaining around 27% year to date. Its recent second-quarter results were also robust, trumping consensus estimates. The company has delivered a string of solid performances over the past four quarters, but will it be able to continue the same going forward? Let's take a brief look at its performance in the quarter, then analyze the prospects.

A good performance

Merchandise revenue, which includes shipments of agricultural, industrial, and housing & construction products, jumped 4% year over year. Growth in revenue from train-to-truck (intermodal) transport, along with merchandising gains, helped the company to offset declines from coal.

CSX's revenue came in at $3.07 billion, slightly higher than the year-ago quarter's revenue of $3.01 billion. It beat consensus estimates of $3.02 billion, fueled by higher volumes and favorable rail industry pricing, combined with improvements in operating efficiency and services.

Operating income increased 2%, helping the company earn $0.52 per share, exceeding the consensus estimate of $0.47 per share. This was also better than the year-ago earnings per share of $0.49.

Chugging ahead

Industrial (31%) and coal (25%) are the company's two major segments. Cheaper natural gas has led to a decline in the coal business, with erstwhile users of coal switching to natural gas because of its lower cost. Coal might perform better in the future, however; a recent report suggests that natural gas could lose market share to coal as the latter becomes relatively cheaper. A resurgent demand for coal could spell better times for CSX.

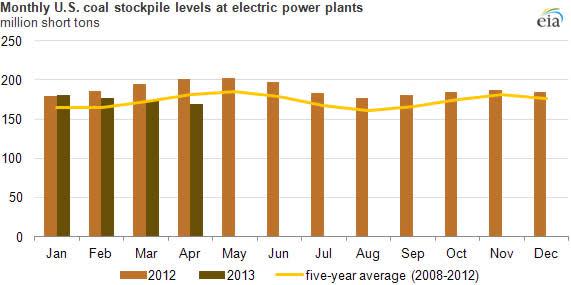

The coal inventory pile up at utilities happened mostly throughout 2012. This is already coming down in 2013 (as shown in the two graphs below) as a result of shift from natural gas to coal as fuel.

Source: eia

Going forward, one can expect increases in volumes and revenue from coal transportation. In the long term, the eastern railroads should also benefit from longer haul lengths as supply is sourced beyond Appalachia.

Acquisitions and mergers are also part of the company's expansion and diversification plans. CSX recently announced the purchase of the Eastern Associated Terminal in Tampa, FL, from the Ingram Barge Company. The capacity of combined terminals allows for fast and scalable expansion, and a capacity for an additional 1 million export tons.

In 2008, CSX embarked upon an ambitious $850 million "National Gateway" infrastructure initiative aimed at improving its freight transport between the Mid-Atlantic ports and the Midwest. It is expected that this will bring down transportation costs, increase haul lengths, and allow CSX to better compete with its rivals.

This project is slated for completion in 2015 and is expected to provide a substantial boost to intermodal volumes. These network improvements should allow the eastern railroads to gain some market share from their western peers.

CSX should also benefit from the woes of the trucking industry. Increases in fuel prices, a shortage of long-haul drivers, and highway congestion are the industry's biggest headwinds. This creates the perfect environment for railroads to gain market share, as shippers start opting for rail transport over trucking to cut down on transportation costs.

CSX also aims to bring down its operating ratio to the high 60s by 2015, and subsequently move further down to the mid-60s in the long term. This target seems achievable, given that many infrastructure initiatives are slated for completion in 2015. The company hopes that greater efficiency will help it meet the challenges posed by a sluggish economy and a volatile coal market.

Other players

Union Pacific links 23 states in the western U.S. by rail. It recently posted second-quarter results and saw growth in earnings and revenue. Going forward, there are a few factors that should act as tailwinds for the company.

As Valero's crude-by-rail project awaits approval, Union Pacific is already making the necessary moves of beefing up its tracks; these improvements began in June of this year. This is just a small part of a mammoth $3.6 billion initiative spread across 23 states with the aim of improving network efficiency, adding new business avenues, and enhancing safety, reliability and productivity.

With the increase in natural gas prices, utility companies are switching over to coal; this is also enabling Union Pacific to increase coal carloads. Coal shipment grew 12% year-over-year in the second quarter, and as the demand for coal increases (as shown in graph below), this is bound to benefit the company.

Kansas City Southern also recently reported its second-quarter results. Its revenue increased 6% from the same quarter a year ago to $579.3 million. This was helped primarily by a 3% increase in carloads and significant improvements in the company's energy segment. Adjusted earnings also increased by around 9% from the year-ago quarter to $0.96 per share. This increase was driven by favorable rail industry pricing and volume improvement.

The recovery in the housing sector should also help the company as forest products make up 46% of its industrial and consumer products division. Kansas City also expects a growth in crude-by-rail to Texas and remains committed to building a new crude terminal in Port Arthur; once completed, the terminal will enable its crude-by-rail business to grow in the future.

Kansas City is estimated to see a 48% growth in sales through 2016. This beats peer for whom estimates are available, according to data compiled by Bloomberg. The increase is facilitated by the company's operations in Mexico, where the economy is growing almost twice as fast as in the U.S.

Conclusion

CSX has been chugging along nicely and enjoying higher pricing, just like the rest of the railroad sector. But unlike the other companies discussed in this article, it has 2.4% dividend yield, while Union Pacific has a 2% yield and Kansas City has an almost negligible of 0.80%. Investors looking for decent dividend income and stable price appreciation should consider CSX as an investment.

With the American markets reaching new highs, investors and pundits alike are skeptical about future growth. They shouldn't be. Many global regions are still stuck in neutral, and their resurgence could result in windfall profits for select companies. A recent Motley Fool report, "3 Strong Buys for a Global Economic Recovery," outlines three companies that could take off when the global economy gains steam. Click here to read the full report!

The article This Railroad Company Is Chugging Along Nicely originally appeared on Fool.com.

ANUP SINGH has no position in any stocks mentioned. The Motley Fool owns shares of CSX. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.