Investing in Underwear Could Help Your Portfolio

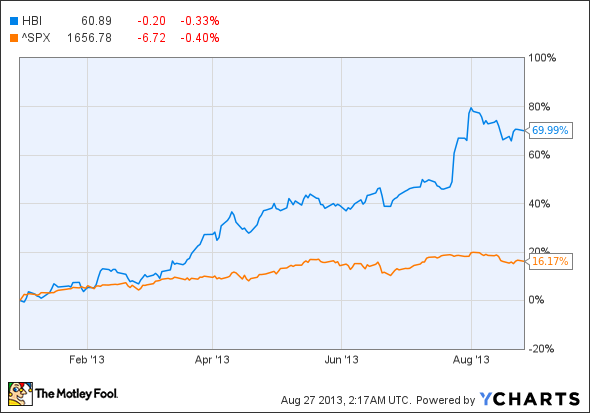

Hanesbrands (NYSE: HBI) owns a number of famous brands and sells its products directly to customers through a chain of more than 200 stores, as well as online. The stock has done well this year, rising almost 70% compared to about a 16% uptick in the S&P 500 index, but it still looks cheap with a trailing P/E of under 17x.

Moreover, given the company's solid strategies and execution, the stock might appreciate further, as evidenced by recently-reported quarterly results. Revenue increased by 2% to $1.2 billion primarily due to increased sales in the inner-wear segment.

The success of Hanesbrands' "Innovate to Elevate" strategy led to a 51% increase in operating profit to $181.4 million, as compared to $119.9 million in the year-ago quarter. In addition, lower cotton costs also helped. As a result, EPS advanced 78% from the year-ago quarter to $1.19 and beat consensus estimates of $0.94.

Another acquisition and a good strategy

Hanesbrands has always eyed mergers and acquisitions for growth. Years ago, it purchased Gear For Sports, and that worked out well for company. It recently acquired Maidenform Brands (NYSE: MFB), which will add brands like Maidenform, Flexees, and Self Expressions to its already comprehensive portfolio. Hanesbrands did well in the inner-wear segment in the reported quarter, and with this acquisition it is expects to keep the momentum intact.

Maidenform delivered a profit but missed consensus estimates on both earnings and revenue in the most recent quarter. Also, analysts have a neutral outlook as far as next quarter's performance is concerned. Maidenform struggled as a result of cheaper competition in the women's underwear business. The company had to resort to discounts and heavy advertising to compete. It is expected, however, that the synergies as a result of the acquisition by Hanesbrands will lead to lower costs and contribute to earnings.

Hanesbrands ranks second in terms of underwear market share, at 14.3% of the market. Maidenform ranks fifth with 2.5%. The combined company will be one of the leading underwear companies. As a result of the acquisition, Hanesbrands gets a big portfolio of brands, which implies more leverage and pricing power with retailers ranging from Wal-Mart to Macy's.

It also expects that the adjusted annual revenue will exceed $5 billion within three years, thereby producing $0.60 per share in earnings going forward. This will also benefit Hanesbrands with a larger market share within the shape-wear industry.

Maidenform currently outsources all of its manufacturing to third parties, whereas Hanesbrands manufactures approximately two-thirds of its own bra products. By plugging all Maidenform brands into its own manufacturing facilities, Hanesbrands can also cut manufacturing costs.

Hanesbrands has also been actively pursuing its "Innovate to Elevate" strategy. These are typical cost-cutting and margin/profit improving exercises, which are necessary to counteract macroeconomic headwinds. It aims to reduce input costs, strengthen its brand value, and thus provide a value-added product with higher margins. It is also exiting non-core businesses, closing under-performing segments, and changing the product mix to enhance performance.

A better buy

One of the main rivals of Hanesbrands is L Brands (NYSE: LTD), the owner of Victoria's Secret. Victoria's Secret is the biggest threat to Hanesbrands and Maidenform, as it has more than 1,000 stores across the globe. L Brands is also expanding its various businesses, such as PINK, Henri Bendel and VSX, which could lead to stiffer competition for Hanesbrands. But Hanesbrands looks cheaper than L Brands on a trailing basis, and that too by some margin.

While L Brands trades at a trailing P/E multiple of almost 23x, Hanesbrands trades at a much cheaper 16.6x. L Brands is expensive on other metrics as well, with a PEG ratio of 1.7, while Hanesbrands has a PEG ratio of just under 1.0. So Hanesbrands trades at a cheaper multiple, but it should also be noted that L Brands is witnessing superior growth. Its comparable-store sales grew 6% in the recent quarter.

But investors looking for a cheaper option might consider Hanesbrands, and they won't be wrong in doing so. Hanesbrands' cost-cutting initiatives and latest acquisition should help it perform better in the future.

Conclusion

After a dazzling performance so far this year, I think that Hanesbrands can do even better as it executes its strategies and benefits from its Maidenform acquisition. The stock is not too expensive either, and it is worthy of further research by investors looking to make a new addition to their portfolio.

The Motley Fool's chief investment officer has selected his No. 1 stock for this year. Find out which stock it is in the special free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

The article Investing in Underwear Could Help Your Portfolio originally appeared on Fool.com.

ANUP SINGH has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.