Why Ecolab Could Do More With Its Dividend

The Dividend Aristocrats is a list of stocks that have increased their dividends annually for at least 25 years. For dividend investors, it's a hallmark of quality and consistency. Yet a stock doesn't actually have to have a high dividend yield in order to qualify. Some members of the Aristocrats actually yield far less than the market average, having chosen to be conservative in their returning capital to shareholders.

Water and sanitation company Ecolab has raised its dividend every year since 1986, but its share price has risen so rapidly that even with reasonable dividend growth, its payout yield remains a very low 1%. However, with a very low payout ratio, income investors should consider whether Ecolab might accelerate its dividend increases in future years. Let's take a closer look at Ecolab to see whether it's likely to sustain or even improve on its dividend growth.

Dividend Stats on Ecolab

Current Quarterly Dividend Per Share | $0.23 |

Current Yield | 1% |

Number of Consecutive Years With Dividend Increases | 28 years |

Payout Ratio | 32% |

Last Increase | December 2012 |

Source: Yahoo! Finance. Last increase refers to ex-dividend date.

What's driving Ecolab's dividend growth?

Ecolab finds itself in an increasingly important industry to support overall global economic growth. The company helps countries around the world manage their water resources as efficiently as possible, making the most use of available supplies, and ensuring water quality with its cleaning and sanitation services. Given that more than a third of the world's population lives in areas where water is scarce, especially in rapidly growing nations like China and India, Ecolab's opportunity to grow is almost boundless.

In order to take maximum advantage of its opportunity, Ecolab has made several smart strategic moves. Late last year, the company decided to sell off its vehicle-care products division to cleaning-products maker Zep , paving the way for a greater focus on its water-management business.

But a much more important deal for Ecolab involved buying privately held Champion Technologies for $2.5 billion. This added to its 2011 buyout of Nalco Holding, and made Ecolab a market leader in oilfield chemicals.

Alternative production methods like hydraulic fracturing are extremely water- and chemical-intensive, and high energy prices have spurred huge growth in their use. The much-smaller Nuverra Environmental Solutions has become a big player in the fracking water-services niche, helping drillers obtain and recycle water supplies in areas where getting enough water is a major challenge. Its success has spurred competition from more established oil-services playersHalliburton and Baker Hughes , which in time could create overcapacity that would threaten the profitability of the segment.

But at least for now, there appears to be enough business to support growing efforts from Ecolab and the rest of the industry.

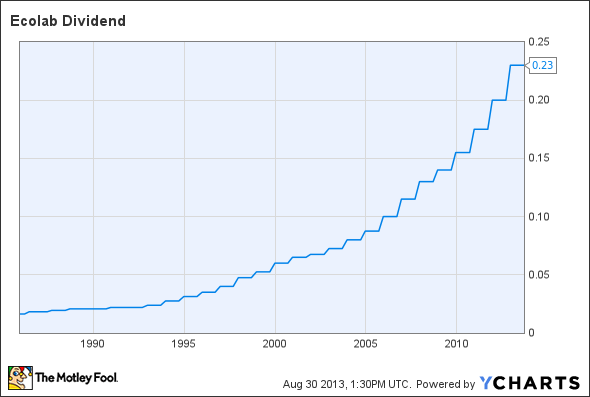

Ecolab Dividend data by YCharts.

As you can see, Ecolab's dividend growth has been steady and substantial for decades. What the chart doesn't show, though, is how much faster Ecolab's share price has risen over that time. As a result, yields have fallen to relatively low levels, even though the company has boosted its dividend payout by double-digit percentage amounts annually since 2009. Given Ecolab's intent to keep expanding around the world, further growth should help bolster dividend payouts in the future.

When will Ecolab boost its payout?

With Ecolab having raised its dividend last December, investors can expect another boost toward the end of this year. A jump to $0.26 or $0.27 per share would be consistent with past increases, though it would only push the yield up to 1.2% or so. Given Ecolab's share-price performance, shareholders probably won't mind the skimpy payout as long as they continue to enjoy big capital gains.

Interested in natural resources? Then you owe it to yourself to discover the most precious resource in the history of the world. It's not gold. Or even oil. But it's more valuable than both of them. Combined. And here's the crazy part: one emerging company already has the market cornered... and stands to make in-the-know investors boatloads of cash. We reveal all in our special 100% FREE report, "The 21st Century's Most Precious Natural Resource." Just click here for instant access!

Click here to add Ecolab to My Watchlist, which can find all of our Foolish analysis on it and all your other stocks.

The article Why Ecolab Could Do More With Its Dividend originally appeared on Fool.com.

Fool contributor Dan Caplinger has no position in any stocks mentioned. You can follow him on Twitter @DanCaplinger. The Motley Fool recommends Halliburton. The Motley Fool owns shares of Ecolab and Nuverra Environmental Solutions and has the following options: long January 2014 $4 calls and short January 2014 $3 puts on Nuverra. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.