Is Ford Hypocritical for Lashing Out at Japanese Policy?

Last week, Ford stepped up its criticism of Japan's monetary policy. Ford's North American chief, Joe Hinrichs, told Bloomberg Businessweek that the weak yen is supporting auto exports from Japan to the U.S., benefiting competitors such as Toyota Motor and Honda Motor .

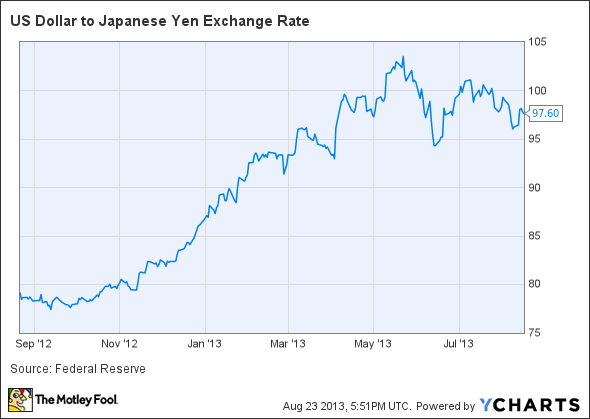

US Dollar to Japanese Yen Exchange Rate data by YCharts

Indeed, over the past year, the yen has lost more than 20% of its value with respect to the dollar. This change in the exchange rate benefits Japanese exporters. However, when you look at the yen-dollar exchange rate in context, it's hard to argue that the yen's recent drop is unfair in any way.

First, the yen-dollar exchange rate has remained well within the normal historical range this year. Second, one of the main factors that drove the yen to record highs against the dollar (before the recent correction) was the Federal Reserve's quantitative easing programs. Indeed, loose U.S. monetary policy has been a major factor in improving the competitiveness of the U.S. auto industry. In this context, Ford executives seem downright hypocritical.

Ford's case

Hinrichs alleges that Japanese automakers maintain approximately 2 million units of excess capacity, whereas auto production capacity is very tight in North America. Hinrichs thinks Japanese automakers like Toyota should be forced to restructure (i.e., cut) their excess capacity. Otherwise, excess demand in the U.S. might ultimately be met by Japanese exports, rather than additional U.S. capacity.

This represents the second time this summer that a Ford executive has criticized Japanese trade policy. Back in late June, Ford CEO Alan Mulally called Japan a "currency manipulator" and argued that Japan is a "closed market" where foreign automakers can't compete.

The threat from a weaker yen to Ford and General Motors is very real. With lower costs, Japanese automakers can ramp up incentive spending to stimulate demand, meeting any excess demand with exports from Japan. Indeed, Nissan cut prices for many of its models earlier this year, and Toyota recently cut the price of the Camry -- the top seller in the critical midsize car market.

So far, Ford and GM have seen no ill effects from this stepped-up price competition. However, as the Japanese automakers begin to promote their price leadership, Ford and GM may need to up their incentive spending as well, crimping margins.

This is how free trade works

Currency movements are a natural part of a globalized economy with floating exchange rates. The Japanese economy has been significantly weaker than the U.S. economy over the past 20 years. Japan's GDP peaked at more than 70% of U.S. GDP in 1995; today, Japan's GDP is just 40% of U.S. GDP.

While many factors have played a role in Japan's long economic slump, uncompetitive exchange rates have created a huge headwind for Japan. According to economic theory, a country with a relatively weak economy should see its currency fall compared with those of stronger economies. This mechanism acts as an "automatic stabilizer," because as a country's currency falls, it makes exports more competitive and imported goods less competitive.

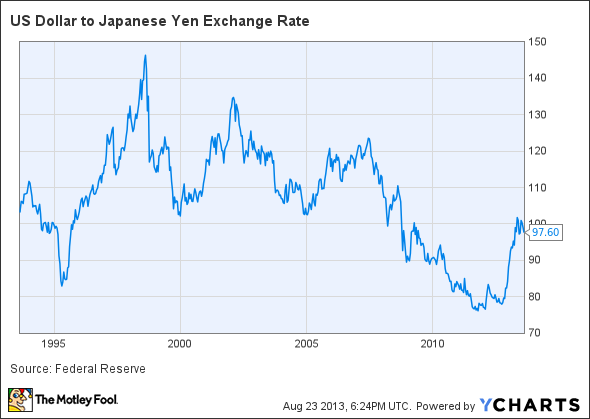

If we zoom out from the one-year snapshot of the yen-dollar exchange rate, it becomes clear that the yen has actually appreciated against the dollar over the past 20 years. In other words, Japanese exports have become less competitive vis-a-vis products "made in the USA," even though Japan's economy has been much weaker over that time period.

US Dollar to Japanese Yen Exchange Rate data by YCharts

Looking at the past six years, U.S. monetary policy has probably had a bigger impact on the yen-dollar exchange rate than Japanese monetary policy. The yen went into freefall against the dollar from mid-2007 until the beginning of 2012. That movement correlates closely with a dramatic loosening of U.S. monetary policy. First, the Federal Open Market Committee rapidly cut the federal funds rate from 5.25% to approximately 0 between September 2007 and December 2008.

The Fed's first quantitative easing program came directly on the heels of these rate cuts and continued into 2010. Later in 2010, the Fed initiated a second round of quantitative easing that continued until June 2011. A third round of quantitative easing followed in 2012.

These policy actions helped drive the yen-dollar exchange rate from around 115 in mid-2007 to a low of 76 in early 2012. That drop vastly improved the economics of U.S.-produced autos over Japanese imports. While Ford and GM primarily used cost cuts to return to profitability since the Great Recession, the strong yen gave them a big assist.

Hot air

Ford has benefited greatly from the Fed's loose monetary policy over the past six years. Ford executives never expressed concerns that they were profiting from an "unfair" advantage. Now that the yen and dollar are moving back into a more rational equilibrium, it seems pretty hypocritical for Ford executives to complain about exchange rates. Japan is simply following the same strategies the U.S. has used to recover from the Great Recession.

Ford has benefited from monetary-policy driven exchange rate fluctuations more than it has been hurt over the past several years. People who live in glass houses shouldn't throw stones.

Ford may be starting to feel the heat from Japanese automakers in the U.S., but its market position in China has never been better. Indeed, the growth of the Chinese auto market will benefit many automakers with exposure to the region. In The Motley Fool's new special report, our analysts get out in front of this trend by identifying two automakers that are poised to surge along with China's middle class. If you want to be among the smart investors who get rich from this growing trend, you can instantly download our free report on the topic by clicking here now.

The article Is Ford Hypocritical for Lashing Out at Japanese Policy? originally appeared on Fool.com.

Fool contributor Adam Levine-Weinberg has no position in any stocks mentioned. The Motley Fool recommends Ford and General Motors and owns shares of Ford. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.