Weak Prices Have This Hedged Producer Over the Barrel

Linn Energy's (NASDAQ: LINE) current predicament is a conservative investor's worst nightmare. This is after all, a company often bought for long-term income and preservation of capital. Linn sports an excellent track record of value creation, but keeping up growth is becoming more and more of a challenge. Recent events starkly highlight the depth of that problem. One obvious cure for what ails Linn is closure of the BerryPetroleum (NYSE: BRY) deal. Unfortunately, dollars shed from LinnCo (NASDAQ: LNCO) shares make that deal look more and more tenuous by the day. Absent Berry, Linn faces serious challenges.

Posts, blogs and articles regarding the accounting peculiarities at the center of this maelstrom litter the Internet. However, relatively few focus on the immediate cause of Linn's predicament. That seems to have been lost in the tide of articles passionately debating the legitimacy of Linn's non-GAAP put accounting.

It's as simple as the numbers.

Linn's real problem is more mundane and perhaps more serious than the sensationalized accounting controversy. At the heart of the matter is a straightforward hedging deficiency. That's ironic for a company that's hedged more fully than any of its peer group.

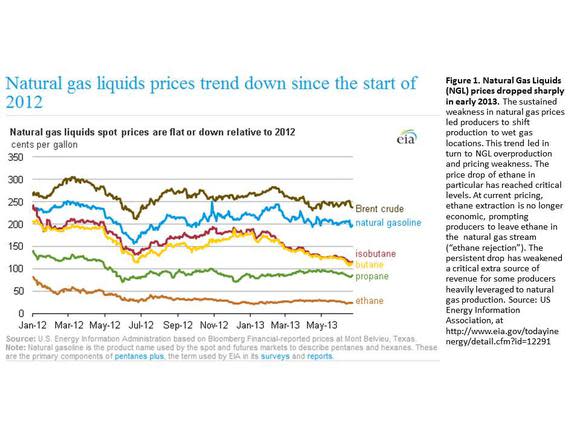

In a nutshell, the problem is that natural gas liquid (NGL) prices collapsed on Linn (see Figure 1 for a recent price chart of NGL constituents). Hedging NGL prices is more complicated than natural gas and oil. It requires separate contracts for individual hydrocarbons and few upstream producers bother given the complexity. In the absence of NGL hedges, a collapse of ethane prices caught Linn with its pants around its ankles.

NGLs were a godsend for the large natural gas producers of the mid-continent (mid-con) region like Devon and Chesapeake. As natural gas prices cratered, drillers shifted rigs to wet gas locales that were still profitable given the liquids they produced. Just like the larger independents, Linn ramped its liquids production on the back of solid results from its mid-con Granite Wash acreage. Much of that liquids growth came in the form of NGLs and not oil.

The Nat Gas solution bred an NGL problem.

Gas wells are "wet" when they're relatively rich in larger alkanes. When natural gas is processed, any larger alkanes are removed and sold separately. These larger alkanes (ethane, propane, butane, isobutane and pentanes) are collectively reported as NGLs by producers. Value added through fractionation is significant.

While NGLs boosted revenue at a badly needed time, in many ways producers just kicked the can down the road. What began as a dry gas oversupply blossomed into an NGL oversupply. Ethane supplies in particular have reached critical levels, as Linn and others now face ethane rejection.

It takes energy to fractionate natural gas. At some point, it becomes economically infeasible to extract ethane if prices can't support that cost. When this critical price is reached, processors stop removing ethane from the gas stream, extracting only larger hydrocarbons. Current pricing puts us in this ethane rejection territory, an environment that's persisted since the end of 2012. That has producers feeling the pinch.

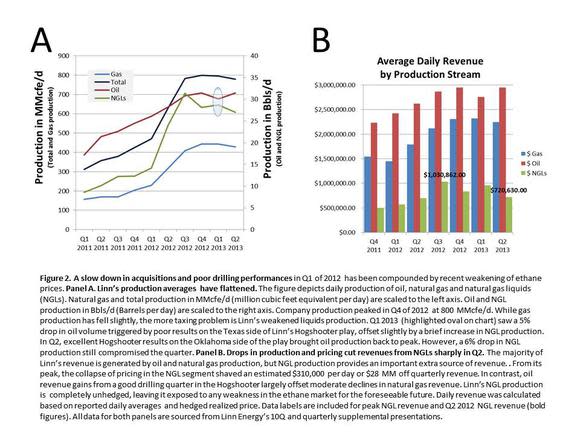

For Linn, the problem exhibits itself in two ways. The first is that rejected ethane is lost to the gas stream, cutting NGL production levels. That's a contributing factor to Linn's reduced Q2 NGL numbers. NGL production was off 6% from the linked quarter (see Figure 2A). Second, lower pricing dragged revenue down yet another notch.

While Linn derives only a small portion of its revenue from NGLs, their contribution remains significant (see Figure 2B). Its importance becomes clear when you consider the size of the hole in Linn's coverage ratio. The single most germane issue brought up by shorts is that Linn's distribution exceeds its own distributable cash flow metrics. In Q2, Linn paid out $170 million to unitholders, but recorded only $152 million in distributable cash flow (DCF). That's an $18 million shortfall .

Management expected to fill that hole by increasing liquids production in the back half of 2013. Excluding the NGL problem, they almost got that done. Linn boosted oil revenue almost $17 million in Q2. Unfortunately, gas revenue receded some $6 million and NGL revenues fell over $20 million linked quarter (numbers are estimated off daily production and pricing averages.). Linn patched its Texas Hogshooter problem, only to encounter a new one at an inopportune time.

Is relief on the horizon?

Signs are that the problem will persist. ONEOK Partners (NYSE: OKS) operates one of the largest NGL midstream operations in the US, serving the mid-con and Rockies region. That's Linn's sweet spot. ONEOK lost about a fifth of its market cap since earlier in the year on the same sticky issue. A recent S&P downgrade of ONEOK debt highlights the severity of the problem.

On its quarterly call, ONEOK management suggested that ethane rejection will persist longer than it originally forecast, lasting well into 2014 and perhaps even 2015, albeit at lower levels. Bakken rejection may subside earlier in 2014, but mid-con and Rockies rejection could extend into 2015. That's bad news for Linn's NGL revenue shortfall given Linn's operating footprint.

On the plus side, ONEOK expects deflated propane prices to increase, helping it through this rough patch. ONEOK can divert its underutilized ethane transport capacity to propane, offsetting some of the revenue drop. Propane price increases would be good news for Linn as well, helping to partially buoy NGL prices. Regardless, ethane rejection should continue to pressure NGL production levels well into 2014 and perhaps, 2015 if ONEOK is correct. That should concern LINE and LNCO holders.

The furor over Linn's accounting is certainly a factor in LINE and LNCO weakness. Conservative investors will sometimes exhibit weak hands when confronted by these kinds of issues. The numbers are usually more critical, though. Linn's real problem is an operational problem. Absent the Berry acquisition, Linn's up against a poor pricing trend in NGLs that's justifiably squeezing shares.

Since relief from that NGL issue does not appear to be on the horizon, the best road forward is to boost oil production. First quarter attempts failed as the Hogshooter came up lame in Texas. In Q2, just as the Hogshooter came through strongly in Oklahoma, weakening NGL prices wore another hole in Linn's pocket. For now, I remain cautiously long. The Berry acquisition is dominating the news, but keeping a close eye on Linn's drilling program in the back half of the year could be just as critical.

There are many different ways to play the energy sector, and The Motley Fool's analysts have uncovered an under-the-radar company that's dominating its industry. This company is a leading provider of equipment and components used in drilling and production operations, and poised to profit in a big way from it. To get the name and detailed analysis of this company that will prosper for years to come, check out the special free report: "The Only Energy Stock You'll Ever Need." Don't miss out on this limited-time offer and your opportunity to discover this under-the-radar company before the market does. Click here to access your report -- it's totally free.

The article Weak Prices Have This Hedged Producer Over the Barrel originally appeared on Fool.com.

Peter Horn owns LINE units. The Motley Fool recommends ONEOK Partners, L.P.. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy. Is this post wrong? Click here. Think you can do better? Join us and write your own!

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.