These 2 Retail Stocks Are Bucking the Trend

The future of the retail sector has been cast into doubt ever since Wal-Mart and Macy's reported lackluster growth last quarter, with an unexpected decline in consumer sentiment topping off those tepid earnings. However, that doesn't mean that investors should dismiss all retail stocks. In a previous article, I noted that the decline of Wal-Mart and Macy's represents weakened discretionary spending from lower to middle income households, but higher-end retailers, such as Tiffany & Co. and Michael Kors, have been spared thanks to their more affluent customers.

Whereas that disparity can be considered a macro factor, I'd like to take a moment to discuss the micro factors as well, specifically how certain companies have thrived by concentrating on narrower markets. Two companies in particular -- Urban Outfitters and the Estee Lauder Companies -- recently bucked the trend and reported robust top and bottom line growth, surprising investors who had expected consumer weakness to take its toll on makers of kitschy clothing and beauty products.

Urban Outfitters continues to dominate its rivals

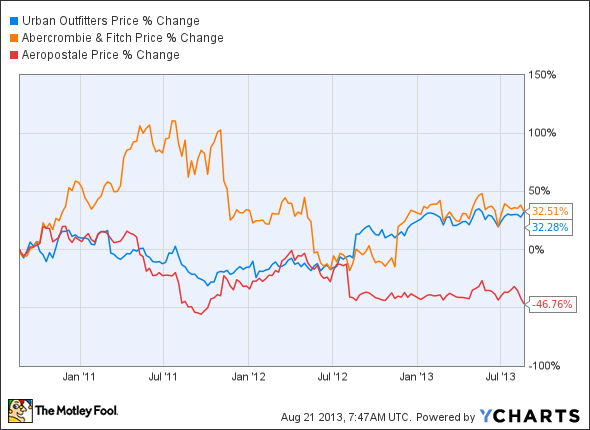

The decline of the apparel retail industry, especially those company's focusing on teens and young adults, has been well documented. Abercrombie & Fitch and Aeropostale have been leading the decline, as their once-popular logo-branded clothing have been overshadowed by the rising popularity of H&M and Forever 21, which offer cheaper, trendier fashions refreshed at a faster rate.

Last quarter, Abercrombie's earnings declined 400% as its revenue slid 8.9%. Aeropostale did just as poorly, reporting a 223% decline in earnings on a 9% drop in revenue. Same-store sales at Abercrombie and Aeropostale both fell 15% from the prior year quarter.

With those bleak numbers overshadowing the retail apparel sector, investors weren't expecting much from Urban Outfitters, best known for its kitschy, humorous clothing and novelty gifts. The company also owns Free People, a Bohemian brand for young women, and Anthropologie, a contemporary female brand.

Yet Urban Outfitters surprised analysts and investors with its second quarter earnings, reporting a profit of $0.51 per share, up from $0.42 per share a year earlier and beating the consensus estimate of $0.48. Revenue climbed 12% to $758.5 million, falling slightly short of the $768.1 million that analysts had expected.

However, same-store sales surged 9% across the board, topping the consensus estimate of 8.1%. Same-store sales rose 5% at its namesake stores, 9% at Anthropologie, and 38% at Free People. Those huge growth numbers made it clear that Urban Outfitters is a survivor in a sea of drowning industry peers. The company's digital initiatives, which I previously discussed, are also far ahead of its industry peers, and are helping it keep in touch with its younger customer base through mobile apps and social connections.

Estee Lauder remains immune to macro trends

Although beauty products are often categorized as discretionary purchases, many women consider them every bit as necessary as groceries and fuel, a fact that was reflected in Estee Lauder's impressive fourth quarter earnings.

Estee Lauder's earnings rose 84% to $0.24 per share, as revenue climbed 7% to $2.4 billion. The company attributed that strong top and bottom line growth to robust sales of skincare and makeup products, along with improving operating margins. Estee Lauder also owns the Clinique, MAC, Bobbi Brown and La Mer brands. The company primarily competes against cosmetics giant L'Oreal and Coty, both of which produce fragrances, cosmetics and skin and body care products. Coty's diverse portfolio of products includes licensed products from Calvin Klein, Chloe, Davidoff, Marc Jacobs, Playboy, and many more.

The company expects its current quarter sales to rise 5% to 7%, although profit is expected to come in below Wall Street expectations for $0.90 per share. Estee Lauder attributes the slower growth to weakness in south Europe, South Korea and the United States, exacerbated by higher promotional and advertising costs. Investors, however, weren't too concerned about that cautious outlook, instead focusing on its impressive top and bottom line growth in the fourth quarter. Estee Lauder is also expanding heavily into emerging markets, most notably in Africa, to offset its weakness in developed markets.

Analysts noted that the company appears immune to both an economic slowdown and competition. Morningstar analyst Erin Lash stated, "Estee Lauder has not been swayed by slowing global economic growth or competitive pressures, as evidenced by its continued top-line growth and margin expansion."

Estee Lauder forecasts that the global prestige beauty market, which includes L'Oreal and Coty, will grow 3% to 4% -- a slow but steady pace that still might be an attractive alternative to the current volatility in other retail stocks.

Don't throw out the babies with the bathwater

Macro-focused investors might believe that the fall of Wal-Mart and Macy's are ominous precursors to a market plunge, but more adventurous investors should really refrain from tossing out the babies with the bathwater.

Urban Outfitters is showing remarkable growth as its primary rivals are marking down prices in their desperation to reduce inventories and generate revenue. Estee Lauder, on the other hand, is showing slow and steady growth, which shows that beauty products should be considered necessary, rather than a discretionary, purchases.

The Motley Fool's chief investment officer has selected his No. 1 stock for this year. Find out which stock it is in the special free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

The article These 2 Retail Stocks Are Bucking the Trend originally appeared on Fool.com.

Leo Sun has no position in any stocks mentioned. The Motley Fool recommends Urban Outfitters. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.