Is This Iconic Company's Moat Disappearing?

Clorox (NYSE: CLX) is home to some of the most profitable brands in the world, but many investors fear that the company's recent revenue weakness is a sign of a worrisome consumer shift toward private-label products. Clorox derives most of its economic profit from brand equity alone, so if consumers decide brands are no longer important, then Clorox's moat is toast.

Can private labels undercut iconic brands?

Clorox, Hidden Valley, and Brita are just a few of the market-leading consumer brands in Clorox's portfolio. The company has historically generated high returns on capital -- in the 20% to 30% range -- because the earning power of its brands now far exceed the necessary marketing and research spending necessary to maintain the brands' value. In a way, Clorox's portfolio of brands is like a stock portfolio that compounds at over 20% each year -- that's pretty valuable.

But competitive forces seek to limit the company's growth and put pressure on its profitability. Private-label products are abundant in the household products market, which means lower-priced products are displayed next to Clorox's higher-priced branded products.

Worried investors point to the company's dependence on just a handful of retail channels; five retailers accounted for 44% of Clorox's revenues in 2012, including 26% through Wal-Mart. If any of its top five retailers were to drop Clorox's brands entirely, the company's value would be significantly impaired.

However, a large abandonment of Clorox's products is unlikely. Strong brands drive traffic to stores, and stores that do not carry certain brands will get less traffic. If a customer cannot buy Clorox bleach at Target, that customer may go to Wal-Mart for bleach and the rest of her shopping items.

More likely, shelves will become more and more crowded with private-label products receiving more prominent placement than they were traditionally given. Clorox has taken steps to reduce exposure to product categories -- like trash bags -- where consumers care more about price than brand.

But the majority of the company's brands should remain relatively immune to the private-label trend. Since 2005, the company has aggressively raised prices across the board, with nearly all of the price increases still in place today. This would not be possible if the company's brands were under fire from knock-offs.

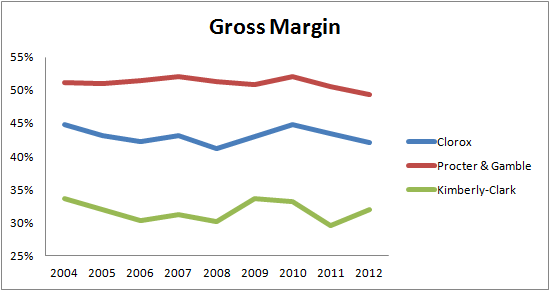

Margins are under pressure, but not from private labels

Private-label products are a minor annoyance for Clorox, not a moat destroyer. The real pressure on margins comes from rising input costs, which have also affected rivals Procter & Gamble and Kimberly-Clark .

P&G's brands include Tide, Charmin, and Iams. Its brand portfolio is much larger than Clorox's; it has $84 billion in sales compared to Clorox's $5.6 billion. P&G also has a much larger geographic footprint, but is now regretting its aggressive expansion into emerging markets and is backtracking to refocus on developed economies with more brand-conscious consumers.

In addition to rising input costs, P&G's margins are under pressure from its bloated cost structure due to the company's over-extension, but its retreat from emerging markets will enable the company to trim a lot of fixed costs. As a result, P&G is in the same boat as Clorox -- strong brands under temporary profitability pressure.

The story is different for Kimberly, however. Like Clorox and P&G, Kimberly owns a portfolio of market-leading brands, including Kleenex, Huggies, and Kotex. However, the company has struggled to maintain its margins more than Clorox and P&G because consumers are more willing to buy off-brand tissues and similar items during periods of economic distress. The protracted high underemployment rate causes additional strain on the company's profitability.

Kimberly's margins are already much lower than Clorox's. This is the difference between brand loyalty and brand preference -- consumers demand Clorox's brands, but only prefer Kimberly's. As a result, consumers will continue to purchase higher-priced products from Clorox and P&G, but Kimberly's margins will come under pressure from private-label products.

Bottom line

Despite recent weakness in revenue and margins, Clorox's moat remains intact due to strong consumer loyalty to its brands. Few moats last forever, but Clorox's will not disappear any time soon.

If you're looking for some long-term investing ideas, you're invited to check out The Motley Fool's brand-new special report, "The 3 Dow Stocks Dividend Investors Need." It's absolutely free, so simply click here now and get your copy today.

The article Is This Iconic Company's Moat Disappearing? originally appeared on Fool.com.

Ted Cooper has no position in any stocks mentioned. The Motley Fool recommends Kimberly-Clark and Procter & Gamble. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.