3 Key Takeaways From This High-Yielding Stock's Earnings

Energy Transfer Partners was the second big-name midstream company to report exceptional second-quarter growth on the back of acquisitions this year. The partnership's EBITDA and distributable cash flow were up $427 million and $126 million, respectively. Kinder Morgan Energy Partners' strong quarter was also powered by acquisitions, as revenue popped more than $1 billion year over year.

1. Distributions

Okay, there isn't much to love about ETP's second-quarter distribution -- it's the same $0.89375 per unit it has been for five years now -- however, management has announced the third-quarter distribution will be $0.01 higher per unit, and the fourth-quarter distribution $0.01 higher than that. No one but Energy Transfer unit holders will get excited about a penny increase on a quarterly distribution, but again, this has been five years in the making.

Management expects to continue to raise distributions in 2014, hopefully by more than a penny, while maintaining a distribution coverage ratio of 1.05 times payouts. The partnership's coverage ratio through the first six months of the year was 0.95 times payouts.

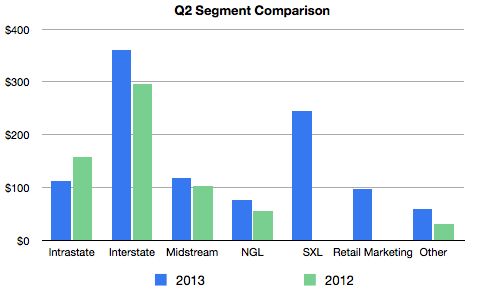

2. Growth

Between the acquisitions and the organic growth, the ETP of today barely resembles the ETP of 2012. You can see this quite clearly in the chart below, which shows the year-over-year adjusted EBITDA comparisons for each business segment.

Source: Company statement

All but one segment is outperforming last year's numbers. On top of that, there are the segments that didn't exist last year: the partnership's stake in Sunoco Logistics and the retail gasoline stations and convenience stores.

One of the real bright spots in the organic growth story is the natural gas liquids, or NGL, transportation and services segment, which had transportation volumes nearly double, and fractionation volumes more than quadruple year over year. This growth came at the hands of pipeline completions and connections at the NGL hub at Mont Belvieu, as well as the start up of a fractionator at the hub.

Also of note, fee-based revenue in the midstream segment increased from $74 million in 2012 to $114 million this year.

3. Cost reductions

It wasn't all sunshine and lollipops at ETP this quarter, however, as commodity prices continued to negatively impact the intrastate transportation and services segment.

On the earnings call, CFO Martin Salinas segued from addressing how commodity prices are beyond management's control to the partnership's plan to reduce costs across the entire organization. It certainly makes sense, given the recent acquisitions, but management is targeting reductions beyond that, aiming to cut $150 million in costs. Investors should have more detail on this initiative by the end of the year.

Forward march

After all of this, Energy Transfer has also announced that it has received approval from the Department of Energy for exporting liquefied natural gas to countries not involved in a free trade agreement with the U.S. It is only the third such approval issued by the DOE, and it means Energy Transfer will move ahead with plans for its Lake Charles liquefaction facility, with an estimated time table of first exports by 2019. In other words, things aren't quieting down at ETP and investors have plenty to think about after all this news.

Energy Transfer is getting killed by low NGL prices, which serves as a reminder of what commodities can do to balance sheets. They can also push those balance sheets up, however, especially when we're talking oil. To help investors get rich off of rising oil prices, our top analysts prepared a free report that reveals three stocks that are bound to soar as oil prices climb higher. To discover the identities of these stocks instantly, access your free report by clicking here now.

The article 3 Key Takeaways From This High-Yielding Stock's Earnings originally appeared on Fool.com.

Fool contributor Aimee Duffy has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.