Despite a Mid-Stage Disappointment, This Biotech Stock Is Still in Great Shape

As human beings it can sometimes be difficult for us to see the good in a bad situation. In the biotech sector, where developing a drug can cost hundreds of millions of dollars and some biotechs rest their entire nest egg on the success of one of two compounds, it takes on an entirely new meaning.

Usually the phrase "failed to meet its primary endpoint" or "didn't provide statistical significance from the placebo" with regard to the results of a clinical trial is met with swift and profound selling by investors -- at least this is the case with many biotech companies. Luckily for shareholders in Isis Pharmaceuticals , this isn't just your run-of-the-mill biotech operation.

Yesterday, Isis delivered some rather sobering mid-stage results for ISIS-CRPrx, a compound being developed to treat rheumatoid arthritis. According to the results of the 51-patient trial, ISIS-CRPrx cut levels of the inflammatory C-reactive protein by 67% but was unable to create a statistical separation from the placebo, which also demonstrated significant inflammation-reducing results. Isis made the decision to stop its investigation of ISIS-CRPrx with regard to RA but continue its ongoing mid-stage study of the drug for patients with atrial fibrillation.

Had Isis been a small operation with but a handful of ongoing trials, this news could have been devastating. Instead, its shares ended the day lower by a mere 2%.

"Why is that?" you might be asking yourself. The reasoning behind investors' ability to shrug off Isis' failure has to do with the nature of its research, the scope of its studies, its partners, and its ability to deliver results.

It's about research

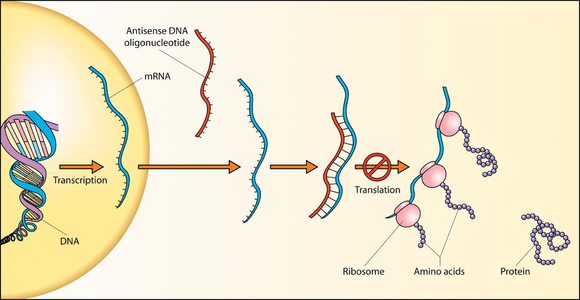

The first unique aspect about Isis is the pathway by which it's developing its drugs. Isis is utilizing antisense technology, which employs antisense molecules to bind with messenger RNA (as opposed to traditional proteins) to block the synthesis of pathogenic cells. Rather than focusing on the result of the faulty RNA sequencing -- the protein -- Isis' solution actually attacks the problem at its point of origin.

Source: Robinson R., Wikimedia Commons.

Specifically, for you science buffs out there, Isis' antisense technology works through the RNase H mechanism that blocks mRNA translation and disallows the formation of new pathogenic proteins without altering the normal genome of a patient. There really are just a handful of companies in the world with an antisense platform, and none appear as advanced as Isis.

It's about the scope of Isis' studies

Including yesterday's disappointing results for ISIS-CRPrx, Isis currently has a product development pipeline complete with seven preclinical studies, six ongoing phase 1 clinical trials, 14 ongoing phase 2 clinical trials, three ongoing phase 3 clinical trials, and one drug approved by the Food and Drug Administration. Add that up and you have 31... you heard me... 31 different potential sources of revenue.

Source: Isis Pharmaceuticals.

And this isn't just a one trick pony, either, like Questcor Pharmaceuticals -- which has one medication, Acthar Gel, indicated for 19 different ailments -- or Alexion Pharmaceuticals, whose entire pipeline revolves around Soliris. This isn't to say that a company like Questcor can't be successful, but it does place a lot of uncertainty around issues that can arise with regard to that one drug. Let's not forget that a U.S. probe into Questcor's marketing practices is still ongoing.

Isis' pipeline features 27 different compounds (a few with multiple indications) across a myriad of developmental areas including the cardiovascular system, severe and rare diseases, cancer, metabolic disorders, and inflammation. The loss of one drug isn't a gigantic problem when you have 31 other possible revenue sources and 27 total compounds in some form of preclinical, clinical, or commercial development.

It's about the partnerships

Nowadays it has become commonplace for smaller biotechnology companies to seek a marketing/licensing partner for its most promising drugs. Rarely, though, do we see the number of partnerships as exhibited by Isis.

If you though having 31 potential revenue-producing compounds was astounding, wait until I tell you that Isis has 12 different clinical partners, ranging from big pharmaceutical juggernauts like AstraZeneca and Sanofi to smaller players like OncoGenex Pharmaceuticals and privately held partners like Atlantic Pharmaceuticals. AstraZeneca and OncoGenex are playing a critical role in partnering with Isis to develop its portfolio of promising cancer products. For instance, ISIS-STAT3rx with AstraZeneca exhibited clear responses in advanced cancer patients in early stage trials. On the other hand, Sanofi's Genzyme unit is the licensing partner for Kynamro, the company's FDA approved injection to treat homozygous familiar hypercholesterolemia, or HoFH. Kynamro is also being tested as a lipid-lowering therapy to help treat cardiovascular disease with late-stage trials currently focusing on lowering apoC-III levels.

In addition, Isis and Alnylam Pharmaceuticals combined their intellectual properties and know-how into a spinoff in 2010 known as Regulus Therapeutics, which supplies both parent companies with supplemental royalties any time it strikes a partnership or licensing deal.

It's about proven results

I would often hesitate to cause one drug approval proof of a pipeline's success, but that's what Kynamro may shape up to be for Isis. Priced at $176,000 annually, Kynamro is one of two newly FDA-approved treatments for HoFH - the other being Juxtapid by Aegerion Pharmaceuticals . On an ease-of-use basis, the orally ingested Juxtapid is certain to be preferred over injectable Kynamro, and the safety profile in trials slightly favors Juxtapid as well. However, physicians who are afraid of being reimbursed, and insurance companies looking to save a lot of money, may consider turning to Kynamro which is nearly $120,000 cheaper on an annual basis than Juxtapid.

Keep in mind that just because I'm extremely optimistic about Isis' future doesn't mean it's not without its risks. Having a vast product portfolio doesn't mean anything if more of its drugs fail in mid and late-stage trials, or if physicians fail to prescribe its FDA-approved drugs. Thus far, Juxtapid has been the HoFH drug of the two that appears to be vaulting out of the gate.

Ultimately, I believe Isis has a lot of potential -- possibly the potential to double or even triple from its current market value -- but it's definitely a company that should be left to biotech-savvy investors who are willing to accept greater risks for a chance at a big reward.

Are you interested in another stock that might have room to run higher? The Motley Fool's chief investment officer recently selected his No. 1 stock pick for this year, and you can find out which stock it is, for free, in the special report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

The article Despite a Mid-Stage Disappointment, This Biotech Stock Is Still in Great Shape originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool recommends Alnylam Pharmaceuticals. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.