Can This British Dividend Stock Bring You Royal Returns?

British-American utility PP&L reported earnings this week, beating on both top and bottom lines. With solid regulated earnings and a brighter forecast, investors are wondering whether it's too late to get in on this dividend stock's profits. Here's what you need to know.

Number crunching

On the top line, PP&L powered past analyst expectations. The utility pulled in $3.45 billion in sales, 35.4% higher than Q2 2012 and a whopping 31.2% above Mr. Market's predictions.

Although revenue rocketed, the utility's bottom line registered more modest growth. Adjusted EPS clocked in at $0.49, falling 3.9% from last year's Q2. But with analyst expectations of $0.46 adjusted EPS, PP&L beat on both lines.

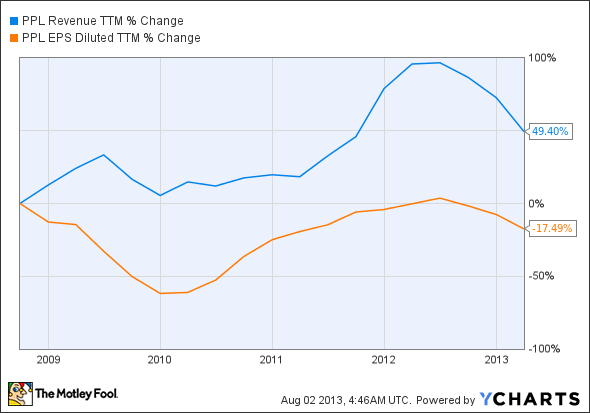

For a peck of perspective, here's how PP&L's trailing-12-month sales and adjusted EPS have fared over the last five years (essentially since the bottom of the Great Recession). While sales have headed up nearly 50%, earnings have tapered off around 18%.

PPL Revenue TTM data by YCharts

Focusing on fundamentals

In the words of PP&L chairman, CEO, and president Bill Spence, "[W]e're pleased with our year-to-date results and feel good about our ability to deliver strong results for the full year." The company's regulated earnings grew across the board, from Kentucky to Pennsylvania to the United Kingdom. The company's British operations account for more than half of overall earnings, and PPL made positive progress with 7.6% EPS gains.

Another stock reporting progress from across the pond is National Grid . The Britain-based utility announced this week that it plans to increase its regulated assets by 6% per year over the next few years. Since utilities' earnings are (roughly) regulated as a percentage of total sales, more regulated assets ideally translates directly to more earnings.

Utilities rocking regulation stand in stark contrast to Exelon's tough quarter. With 65% of its generation fleet reliant on PJM auctions for pricing, cheap power has pushed down the utility's sales expectations. Although Exelon beat on sales and missed by just $0.01 on EPS this quarter, $750 million in new expected sales reductions over the next two years dropped share prices this week.

Probably the biggest news from PP&L's quarter hasn't even happened yet. The utility is upping its ongoing operations earnings expectations for fiscal 2013. Previously in the range of $2.15-$2.40 per share, PPL is edging expectations upward to $2.25-$2.40.

Those predictions are further supported by a solid 7.9% compound annual growth base rate expectation for the next five years. Compared to NextEra Energy's 5%-7% range through 2016, it seems Florida regulators might have more of a stiff upper lip than their British counterparts. And like PP&L, NextEra needs those rates to rise, with regulated earnings accounting for 63% of total earnings this quarter.

Looking ahead

With solid sales expectations, income investors shouldn't be worried about a dividend dip. PP&L share prices have edged down 3.8% over the last three months, putting the dividend stock's current yield at 4.6%.

An upcoming major market mover for PP&L will be the outcome of a recently proposed eight-year plan for its U.K. operations. Regulators are expected to deliver their verdict by March 2014, and a thumbs-up would go a long way to improving the sustainability of PPL's bottom line.

Can PP&L pull profits?

With a solid quarter, dynamite dividend, relatively low price, and focus on the future, PPL has what it takes to put profits in your portfolio. I've already made an outperform call on my Motley Fool CAPS page, and continue to look forward to seeing where share prices head over the next year and beyond.

PP&L offers geographic diversity for your dividend stock portfolio, but wise investors aren't relying on the energy sector alone for profits. With this in mind, our analysts sat down to identify the absolute best of the best across the entire stock market when it comes to rock-solid dividend stocks, drawing up a list in this free report of the only nine that fit the bill. To discover the identities of these companies before the rest of the market catches on, you can download this valuable free report by simply clicking here now.

The article Can This British Dividend Stock Bring You Royal Returns? originally appeared on Fool.com.

Motley Fool contributor Justin Loiseau has no position in any stocks mentioned, but he does use electricity.The Motley Fool recommends Exelon and National Grid plc (ADR). Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.