Near a 52-Week High, Ford Is Still a Buy

I read pretty regularly that investors believe Ford as well as General Motors are undervalued looking at the price-to-earnings ratio. While they do trade at low forward P/Es of roughly 9.5 and eight, respectively, we have to keep in mind that Ford and GM both historically trade at lower P/Es. After Ford's roughly 90% run-up from around $9 to over $17 recently, I'm not shouting that Ford is drastically undervalued anymore - but that doesn't mean Ford isn't still a buy, because I believe it is.

The road ahead

There are many reasons to remain optimistic about Ford as an investment - sit back and take a look and it's easy to see where Ford aims to make improvements. Ford wants to continue to improve its financial stability, which would make it an even safer and more valuable investment opportunity. There are three key points to focus on: automotive debt, pension funding, and cash flow.

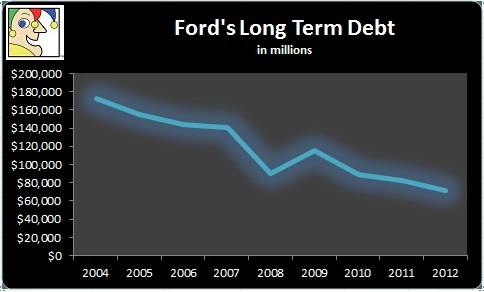

Automotive debt

As of last week, Ford's automotive debt was at $15.8 billion, not including the roughly $90 billion from Ford Motor Credit, a figure that should lower in the years ahead. Ford's been vocal about wanting to reduce its automotive debt level to about $10 billion. It shouldn't have any problem reaching this goal: Consider that Ford's already paid off the roughly $23 billion in loans it received in 2006 to fund the restructuring of the company. The company stays on top of its debt payments, easily seen in the trend of its total long-term debt:

Graph by author, information via Morningstar.com

Pension funding

Underfunded pensions are plaguing many large corporations, and Ford is no different. Because interest and discount rates are so low, companies must increase the amount they're obligated to pay into the fund - rapidly ballooning the underfunded pension figure. Ford's pension plan is underfunded by $18.7 billion, which is still better than crosstown rival GM's staggering $27.8 billion. Ford's pension is underfunded by an amount that is larger than its automotive debt, and just as important.

Fortunately, this year Ford has witnessed discount rates increasing between 70 and 80 basis points, drastically reducing the underfunded figure. An increase toward the high end of that range would reduce Ford's pension gap by 42%, down to $10.8 billion by the end of this year, said Matthew Stover, an auto analyst with Guggenheim Securities, according to Automotive News.

That's an absolutely huge swing and, in combination with Ford's pledge to pay in $5 billion, will put the company in a much more financially stable position and free up even more cash - giving investors just one more reason to buy in.

Cash flow

One problem with Ford has been a decline in free cash flow over the last three years. While Ford spent billions in capital expenditures its free cash flow declined from $7.3 billion in 2010 to $5.4 billion in 2011, and slid down to $3.5 billion last year. This is one reason why Ford's second-quarter report was so great: Its operating related cash flow for the first half of 2013 came in at $4 billion, more than double last year's result. Its gross cash has also been trending upwards recently as well.

Graph by author, information via Ford SEC filings.

For investors this is a great development because it means Ford has plenty of capital to pay down its debt, fund its pension, and continue developing a strong lineup of vehicles - redesigns of the Mustang and F-150 are due out next year. It also means that Ford has plenty of cash available to continue its plan to expand and catch up in China, where it's introducing 15 models by 2015 to double its market share to 6%. Even better for investors, it means there is cash available for share buybacks - to reverse previous share dilution - and possibly even an increased dividend.

It's easy to see where Ford is going as an investment. It's improving its financials, and planning sustainable and very profitable growth - and I'll stay along for the ride.

Ford's use of cash to expand into China is a huge development for investors. Success in China - the worlds largest and fastest growing auto market - will define which automakers will make you the biggest profits. But which automakers are best positioned? A recent Motley Fool report, "2 Automakers to Buy for a Surging Chinese Market", names two global giants poised to reap big gains that could drive big rewards for investors. You can read this report right now for free - just click here for instant access.

The article Near a 52-Week High, Ford Is Still a Buy originally appeared on Fool.com.

Fool contributor Daniel Miller owns shares of Ford and General Motors. The Motley Fool recommends Ford and General Motors. The Motley Fool owns shares of Ford. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.