Going Into Earnings, 3 Questions for iRobot

Brace yourselves, iRobot investors!

Everyone's favorite robot maker is all set to report earnings on Tuesday, and this quarter should provide plenty of information to help you decide whether iRobot is worth your investing dollars.

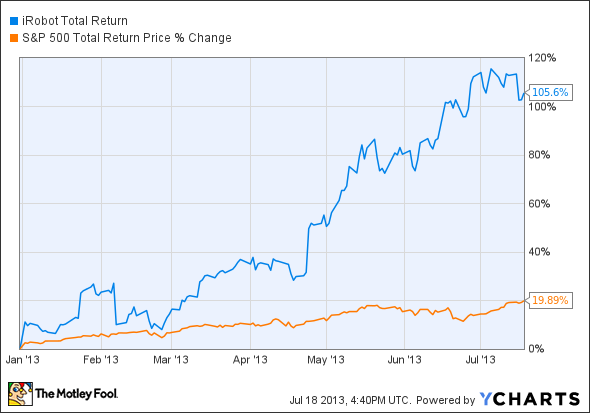

And, considering the stock has more than doubled so far this year, trouncing the broader market's perfectly respectable return, it's quite possible we could see some big price swings next week:

IRBT Total Return Price data by YCharts

Of course, that rise has also prompted valuation concerns, as the stock currently trades at nearly 44 times last year's earnings, and almost 37 times next year's estimates. To be sure, investors who buy now should be aware they're purchasing the stock at a premium.

Then again, I opened my position in iRobot in April 2012, with the intention of holding it at least five years, so I'm not particularly concerned with taking short-term profits. As a result, I already went out on a limb earlier this week to say I likely won't be selling my shares anytime soon.

But that doesn't mean I won't be paying attention to what iRobot has to say next week; to the contrary, here are three questions I have going into iRobot's second quarter report:

1. Can you meet your already-raised guidance?

Remember, back in March, the stock popped 10% in a single day after iRobot raised its quarterly revenue and earnings guidance. Then, when iRobot announced first-quarter earnings in April, it popped another 15% after it beat even its own lofty expectations, and raised its full-year 2013 revenue and earnings guidance, to boot.

Specifically, iRobot told us they expect 2013 revenue of between $485 million and $495 million, a boost over its previous guidance of around just 1%.

What really catalyzed the stock, however, was iRobot's revised earnings guidance, which called for 2013 earnings per share in the range of $0.80 to $1.00. As I noted at the time, those earnings numbers represented a 40% increase on both the top and bottom ranges of iRobot's previous 2013 EPS guidance of $0.57, and $0.72, per share.

Remember, these results were driven largely by domestic Home Robot revenue growth of 44% from the year-ago period, as U.S. consumers increasingly embraced the company's consumer offerings. Even so, international sales still represented around two-thirds of iRobot's overall consumer business.

And that leads me to my second question...

2. Does the world still love your consumer bots?

Keeping in mind the above-mentioned impressive domestic growth, iRobot said earlier this year they expect consumer robot sales to grow another 20% when all is said and done in 2013, at which time they should make up around 90% of iRobot's total business.

This was a direct result of iRobot's previous efforts to scale back its Defense & Security segment last year in the face of unpredictable defense budgets. So far, at least, that move has turned out to be a great one.

As I said earlier this week, however, this also means a turn for the worst in iRobot's now-crucial consumer division would be the one big thing which could entice me to sell my shares.

3. Any progress in your other segments?

Finally, even though iRobot is focusing much of its attention on growing the bolstering consumer robotics market, any success in its other pursuits could end up being icing on the cake for iRobot investors.

And no, I'm not just talking about recent D&S contract wins.

Back in May, for instance, iRobot surprised everybody when it announced seven major hospitals in the U.S. and Mexico have already incorporated its RP-VITA medical telepresence robots into their day-to-day operations.

This is an especially curious win when we remember that shares of robotic surgery specialist Intuitive Surgical fell by as much as 18% last week after the company pre-announced disappointing earnings numbers, primarily due to "weak capital sales in the U.S." Then again, the cost of Intuitive's da Vinci robots can easily run into the seven-figure range, which may be proving a tough sell for cash-strapped hospitals in an increasingly saturated market.

Meanwhile, the RP-VITA is said to be available on a much more affordable leasing model for a reasonable $4,000 to $6,000 per month.

If that sounds expensive, remember that, in addition to the upfront cost of Intuitive's robots, hospitals also must pay thousands for every surgery they perform with them to replace the required instruments for each procedure. RP-VITA, for its part, boasts more intangible benefits, including streamlining hospital operations, and affording specialist physicians the ability of quickly and remotely diagnosing patients, where previously they would have needed to travel.

In addition, just over a month ago, iRobot announced a new partnership with Cisco with another telepresence bot in the Ava 500. This time, however, it was aimed at winning the business of enterprise customers for enabling things like off-site employee participation in meetings, presentations, or site inspections. We haven't heard much about the Ava 500 since then, but it'd be great to get an update on whether it's seeing similar acceptance in businesses as the RP-VITA has with hospitals.

Foolish takeaway

Of course, this isn't an exhaustive list of meaningful things to look for in iRobot's earnings next week, but it's a great place to start.

At the very least, iRobot is definitely worth adding to your watchlist as it expands its reach. In the meantime, we should also remember that profiting from our increasingly global economy can be as easy as investing in your own backyard. The Motley Fool's free report, "3 American Companies Set to Dominate the World," shows you how. Click here to get your free copy before it's gone.

The article Going Into Earnings, 3 Questions for iRobot originally appeared on Fool.com.

Fool contributor Steve Symington owns shares of iRobot . The Motley Fool recommends Cisco Systems, Intuitive Surgical, and iRobot . The Motley Fool owns shares of Intuitive Surgical. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.