Pizza Hut Business Lacks Spice

No two ways about it: Yum! Brands stock has disappointed investors mightily this past year. The owner of perhaps the world's best-known pizza brand -- Pizza Hut -- Yum! shares have gained barely 8% in value this year.

That's less than half the rise of the broader S&P 500 index of companies. It's four times less than the 37% gain seen at Papa John's , and less than a tenth of the gains at skyrocketing Domino's Pizza . But why is Pizza Hut's owner underperforming, and why might its laggard performance continue for longer than investors expect?

Three reasons.

Pizza Hut grows too slowly...

According to analysts who track the prospects of these businesses, Yum! Brands -- the owner of not only Pizza Hut but also KFC and Taco Bell -- has the worst prospects to grow its businesses over the next five years of any of the three pizza chains named so far.

...and it's been growing slowly for quite some time

Worse, this is no recent phenomenon, or easily reversed. It's the continuation of a trend of substandard profits growth at Yum! that's gone on for quite some time. Despite being diversified across three separate kinds of fare, Yum!'s performed poorly for five years straight, relative to its pizza-prepping peers:

Pizza Hut looks like a bargain...

Granted, weak performance and weak prospects do appear to be helping to keep Yum!'s stock price down. When you stack up the stock of Pizza Hut's owner against its smaller rivals, at first glance Yum! Brands almost looks like a bargain. Valued at 22 times earnings, Yum! shares look cheaper than Papa John's (at 23.9 times earnings), and cheaper still when compared to the 27 times earnings valuation at Domino's Pizza.

...but really isn't

And yet, closer examination of the "profits" that contribute to Yum!'s relatively low P/E ratio suggest the company's not really doing as well as it looks.

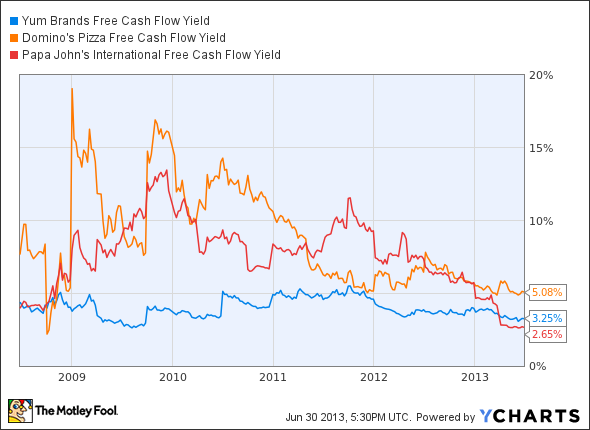

Indeed, if you evaluate Yum! on the amount of cash it produces divided by its market cap (a concept stock investors call the "free cash flow yield"), the company actually only places in the middle of the pack... and toward the bottom. Yum!'s free cash flow yield trails that of industry leader Domino's by a good 183 basis points (36%), yet sports only a 60 basis-point advantage over Papa John's.

YUM Free Cash Flow Yield data by YCharts.

Foolish takeaway

Weaker-than-average growth prospects, combined with a long-term record of undergrowing the competition, suggests the apparent bargain in Yum! Brands stock isn't all it's baked up to be. Opinions may differ on the quality of its pizza pies. But strip away the layer of cheese covering up its cash flow, and Pizza Hut just isn't as good a business as meets the eye.

Not all Fools agree that Yum! Brands is a poor investment. Read The Motley Fool's free report "3 American Companies Set to Dominate the World," and find out why some investors believe Yum! is still a bargain, despite what the naysayers say. Click here to get your free copy before it's gone.

The article Pizza Hut Business Lacks Spice originally appeared on Fool.com.

Fool contributor Rich Smith has no position in any stocks mentioned. The Motley Fool owns shares of Papa John's International. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.