ExxonMobil Stock Is Going Nowhere

No two ways about it: ExxonMobil has disappointed investors mightily this past year.

The mere 7% rise in price in the world's premier "oil stock" works out to less than half the gains seen elsewhere on the S&P 500. It's risen less than half as high as archrival Chevron . Indeed, ExxonMobil stock has even underperformed BP -- and last I heard, Exxon hasn't blown up any gulf oil platforms lately.

But why is Exxon underperforming, and why might its laggard performance continue for longer than investors expect? Three reasons.

Exxon costs too much

When you stack up Exxon stock against its somewhat smaller rivals, it's immediately clear that Exxon shares cost more than its peers. Valued on forward earnings, Exxon shares sell for a 15% premium to Chevron's, and cost a whopping 51% more than BP.

The overvaluation is apparent, too, when valuing the shares on trailing earnings, where Exxon's 9.2 P/E ratio tops Chevron's 8.9 and sells for a 53% premium to the 6 P/E at BP.

Exxon grows too slow ...

Now, this higher P/E ratio might be forgivable if Exxon was an obviously superior stock, with obviously brighter prospects than its peers. It's not. Indeed, as this next chart shows, Exxon's projected earnings growth rate over the next five years isn't very much better than what's expected out of Chevron -- and lags BP's projected pace quite badly.

... and it's been growing slow for quite some time

Can we trust these analyst estimates to be accurate? Maybe not entirely. Crystal balls being both expensive, and notoriously hard to read, it's certainly possible the analysts' projected growth rates for BP, Chevron, and Exxon might be off by a point or two.

That said, it's worth pointing out that the projections for the next five years' earnings do line up pretty well with what we've already seen in these companies' sales trends over the past five years.

So if past is prelude, it's not all that hard to believe that the biggest oil company in the world might struggle to get even bigger, faster than its peers.

In defense of ExxonMobil stock

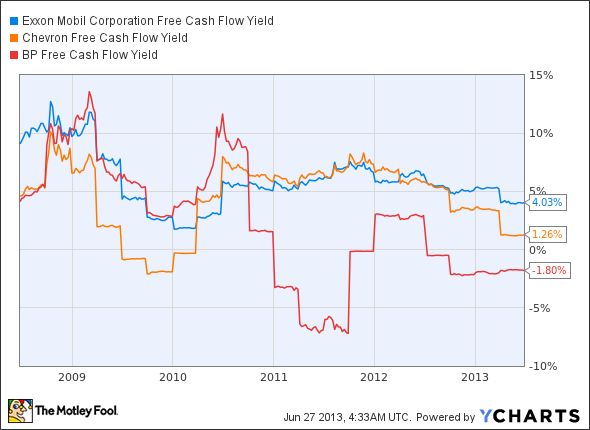

Now don't get me wrong. ExxonMobil isn't all bad. To the contrary, as the following chart shows, when it comes to producing cash from its business, Exxon is actually one of the better performers in the oil industry:

XOM Free Cash Flow Yield data by YCharts

That said, Exxon's only "better" in comparison to the competition -- and "better" isn't quite the same as "good."

Foolish takeaway

Right now, ExxonMobil stock boasts a free cash flow yield (that's the amount of cash profit it produces, divided by the company's market cap) of just 4%. That's a better number than the 1.3% FCF yield at Chevron, and much better than what cash-burning BP reports. But few investors, I suspect, get into this business in hopes of buying a company that can take a dollar of investment and turn it into just four pennies' worth of profits.

If you ask me, the fact that Exxon generates only a 4% free cash flow yield does little to argue in favor of ExxonMobil stock as a good investment. What it really tells you is that if Exxon is the best the oil industry can offer, maybe it's better to stay away from oil companies altogether. Because just like ExxonMobil stock itself, the rest of these companies are also going nowhere.

If you're on the lookout for some better energy plays, check out The Motley Fool's "3 Stocks for $100 Oil." For free access to this special report, simply click here now.

The article ExxonMobil Stock Is Going Nowhere originally appeared on Fool.com.

Fool contributor Rich Smith has no position in any stocks mentioned. The Motley Fool recommends Chevron. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.