Look Who Else Is Flying Delta These Days

Delta Air Lines is one of the largest and most successful U.S. airlines today. In 2012, the company carried more than 100 million passengers on the way to earning an adjusted profit of $1.55 billion. This strong momentum has led to enviable gains for shareholders: Delta stock has nearly doubled since the beginning of December.

Delta Stock Chart, 12/3/12-6/14/13, data by YCharts

Among the many passengers flying Delta last year, one may have escaped notice: top competitor United Continental . United, which has performed far worse than Delta recently -- it earned an adjusted profit of just $589 million in 2012 despite being similar in size to Delta -- has nevertheless managed to ride Delta's coattails to stock greatness in the last six months.

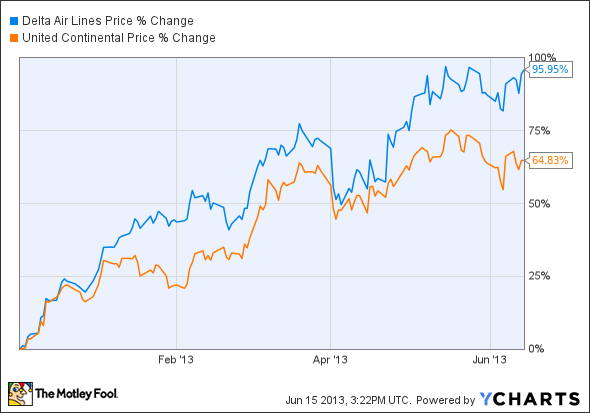

Delta vs. United Continental Stock Performance, data by YCharts

While United's stock has not performed quite as well as Delta's, a 65% gain is nothing to sneeze at. Clearly, Mr. Market is extrapolating from Delta's success and assuming that United will be able to achieve similar profitability soon, particularly now that it has nearly finished integrating United and Continental. However, Mr. Market (and United investors) may be in for a surprise, because while Delta is the real deal, United's results will not be able to support its high stock price.

Disappointment ahead

United's stock has been soaring despite a weak performance in the first half of 2013. The company posted an adjusted loss of $0.98 per share in Q1. Capacity reductions drove a healthy 5.9% unit revenue increase, but this was more than offset by a 6.5% increase in unit costs. Cost growth has moderated in Q2 as jet fuel prices have fallen, but unit revenue has simultaneously taken a turn for the worse, decreasing 0.5% in April and a similar amount in May.

Coming into Q2, industry analysts expected United to return to strong profit growth, but they have since been forced to backtrack due to the company's weak revenue performance. The average analyst EPS estimate for Q2 has dropped precipitously from $1.98 60 days ago (around the time of United's Q1 earnings report) to $1.42 today.

Strangely, while lowering their estimates for this quarter, analysts have actually raised their estimates for Q3 EPS from $2.21 to $2.31 over the past 60 days. Q4 EPS estimates have risen even more sharply, to approximately $0.65, which would be a big swing from last year's $0.58 per share loss in the fourth quarter.

In essence, Wall Street analysts are softening the blow of lower earnings expectations for the current quarter by raising expectations for future quarters. However, this is just likely to lead to an even bigger disappointment for investors down the road. In order to meet full-year earnings expectations, United would need to achieve nearly 500 basis points of year-over-year margin growth in the second half of 2013. This is not likely to happen.

Based on United's cost projections, unit cost growth may reverse in the second half of this year if fuel prices continue to retreat. However, the company would still need robust unit revenue growth to generate 500 basis points of margin expansion. Yet whereas United cut capacity by 4.9% in Q1 and is on pace to cut capacity by more than 2% in Q2, the company plans to increase capacity somewhat in the second half of the year. While this is helping reduce unit costs, it will also create a unit revenue headwind. This will prevent anything beyond modest unit revenue growth.

Be careful out there!

Analysts are still projecting a fairly rosy profit scenario for United this year, despite its continuing weak performance. While Delta recently projected a Q2 adjusted operating margin of 10%-11% -- a healthy improvement from last year's 9.1% result -- United appears poised to duplicate its 7.9% adjusted operating margin from Q2 2012.

Delta's margin advantage of 200-300 basis points over United appears sustainable based on the company's lower, projected-cost growth and its strategic initiatives to boost its corporate revenue share, particularly in New York. That margin advantage is equivalent to roughly $1 billion per year in additional profit for Delta!

United stock has been able to log big gains in the past six months, largely thanks to Delta's success, but ultimately United will have to produce higher profitability to keep the stock afloat. However, the company has no clear path to replicating Delta's superior margins. As a result, United's stock looks very vulnerable over the next year or so.

With the American markets reaching new highs, investors and pundits alike are skeptical about future growth. They shouldn't be. Many global regions are still stuck in neutral, and their resurgence could result in windfall profits for select companies. A recent Motley Fool report, "3 Strong Buys for a Global Economic Recovery" outlines three companies that could take off when the global economy gains steam. Click here to read the full report!

The article Look Who Else Is Flying Delta These Days originally appeared on Fool.com.

Adam Levine-Weinberg is short shares of United Continental Holdings and is long Sep 2013 $33 Puts on United Continental Holdings. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.