Is DIRECTV Stock Destined for Greatness?

Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does DIRECTV fit the bill? Let's look at what its recent results tell us about its potential for future gains.

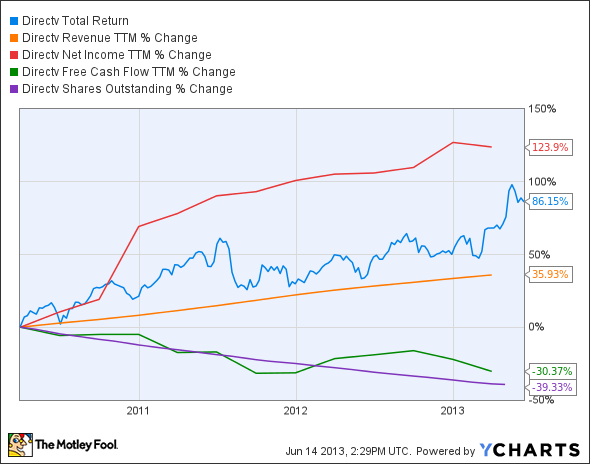

What we're looking for

The graphs you're about to see tell DIRECTV's story, and we'll be grading the quality of that story in several ways:

Growth: are profits, margins, and free cash flow all increasing?

Valuation: is share price growing in line with earnings per share?

Opportunities: is return on equity increasing while debt to equity declines?

Dividends: are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's look at DIRECTV's key statistics:

DTV Total Return Price data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 35.9% | Pass |

Improving profit margin | (8.5%) | Fail |

Free cash flow growth > Net income growth | (30.4%) vs. 123.9% | Fail |

Improving EPS | 253.1% | Pass |

Stock growth (+ 15%) < EPS growth | 86.2% vs. 253.1% | Pass |

Improving return on equity | Negative equity | Fail |

Declining debt to equity | Negative equity | Fail |

Source: YCharts.

*Period begins at end of Q1 2010.

How we got here and where we're going

DIRECTV's massive debt load, which currently stands at over $18 billion, is certainly weighing on the company's score (a meager three out of seven) today. Since the company went into negative equity territory at the start of 2011, its debt has continued to rise, and is over 30% higher now than it was at that point. DIRECTV's declining free cash flow is also a bit worrisome, as it was once well above the company's net income on a nominal basis. What is this satellite service provider doing to slim down its debts and improve its cash flow? Let's take a closer look.

The company's latest earnings report brought nods of approval from Fool contributor Michael Lewis, who pointed out strong earnings and strong growth in Latin America as key reasons why DIRECTV is set to outpace competitor DISH Network , which has been a little distracted with its efforts to buy two debt-laden telecom companies. Neither company has a particularly light debt load, but expanding into a dramatically different (but no less cash-hungry) business could trip DISH up and give DIRECTV the opening it needs to take some of DISH's market share.

It's also undoubtedly true that DIRECTV is less expensive than its peer, and also happens to be growing sales and earnings at a faster rate. The market is apparently discounting DIRECTV's massive debts, which do merit concern, especially if the company seems more interested in buying streaming-video service Hulu than in paying those debts down. Hulu would give DIRECTV exposure to a fast-growing market, and it could be integrated into the company's core satellite offerings, but it would take years for the service to come anywhere near generating the profit necessary to pay down significant chunks of debt.

Putting the pieces together

Today, DIRECTV has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

The television landscape is changing quickly, with new entrants like Netflix and Amazon.com disrupting traditional networks. The Motley Fool's new free report "Who Will Own the Future of Television?" details the risks and opportunities in TV. Click here to read the full report!

Keep track of DIRECTV by adding it to your free stock Watchlist.

The article Is DIRECTV Stock Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter, @TMFBiggles, for more insight into markets, history, and technology.The Motley Fool recommends DIRECTV. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.