Are Investors Missing Something With This Company?

By all accounts, Northern Oil and Gas shows no signs of an ailing company. When you look at its operational and financial metrics the company is performing admirably. So why has its share price fallen 20% while the S&P 500 is up more than 20% in the last year?

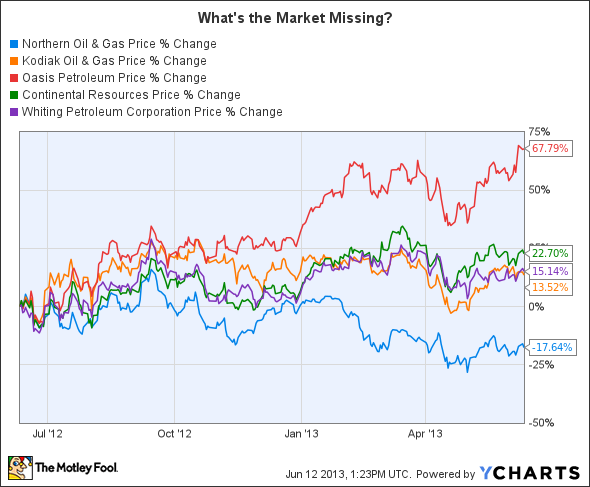

What's even more interesting is that this Williston Basin-focused producer has underperformed virtually all of its peers. Given its unique business model, which we will get to in a moment, you'd think Northern would keep pace with or even perform better than its peers. Instead, over the past year the company's relative performance has looked like this:

As I hinted at earlier, Northern's business model is unique. Instead of drilling its own operated wells in the Basin, the company takes small non-operated positions in Bakken wells. The company's risk is spread across several operators enabling it to leverage the technical and operating staffs of its partners which keeps its costs downs. That's delivered tremendous growth over the past few years.

The company is very diversified across operating partners with no partner more than 22.5% of its net wells. It partners with top operators in the play like Continental Resources , which is 12.5% of its net wells, and Whiting Petroleum , which is 5.5% of its net wells, are two of the top producers in the play. Continental also happens to be one of the lowest-cost producers as well as one of the top leaseholders in the play, while Whiting is a top producer in the play and has a large inventory of future drilling locations. By partnering with these two giants Northern can leverage the expertise as both grow production over the long term.

Not only is Northern partnered with the current top operators, but it has teamed up with some of the fastest-growing operators as well. It counts Oasis Petroleum , with 4.4% of net wells, and Kodiak Oil & Gas , which accounts for less than 2% of its net wells, among its many other smaller partners. Both companies are aggressively growing production out of the Williston Basin, with Kodiak's production projected to double this year, while Oasis has grown its production 71% year over year. In order to keep up the torrid production growth pace both are investing heavily this year with Kodiak and are planning to spend $740 million to drill 75 wells. Oasis plans to spend just under $900 million to drill about 105 wells. These aggressive capital programs are leveraged thanks to Northern's vital capital participation as a non-operated partner in newly drilled wells.

This model has produced substantial growth in production, reserves and cash flow for Northern. The numbers speak for themselves as annual production has gone from 51,500 barrels of oil equivalent, or boe, in 2008 to just under 3.8 MMboe last year. Reserves have jumped from just 800,000 boe in 2008 to 67.6 MMboe last year. Finally, Adjusted EBITDA has grown from only $2.5 million in 2008 to $225.3 million last year.

If there is one concern it is that the company has continued to grow its well count even as average production has remained in neutral. This could be due to the industry-wide switch to mulit-well-pad drilling, as Northern had 12.2 gross wells either being drilled or awaiting completion. With these wells not currently producing production growth is slowing down. Take a look at the chart below and you'll see what I mean:

Source: Northern Oil & Gas Investor Presentation (Opens in a PDF)

Once those dozen wells come on line it should boost production and give investors a clearer picture of its true output potential. The other thing to keep in mind is that production growth won't be as rapid as the company bumps up against well decline rates as well as the law of large numbers. So, while the company won't continue its torrid growth pace forever, it still has tremendous growth opportunities ahead of it because the Bakken is likely just 10% developed at this point.

That's why I think investors are mistaking the recent slowdown in quarterly production as a long-term issue instead of just part of the industry's transition to multi-well-pad drilling. That means investors could be missing out on Northern as a unique way to play the growth in oil production in the Williston; its letting other companies do all the heavy lifting. While there is a lot more to the story, Northern might be a company you'll want to look at a bit more closely if you are interested in profiting from the Bakken.

Another company that's worth a deeper look, and one that's doing a lot of heavy lifting in the play is Kodiak Oil & Gas. The company is a dynamic oil production growth story with average annual production growth in the triple digits. However, while it offers great opportunities, it comes with great risks: Its well costs are very high, meaning that a big drop in oil prices could really crimp its profits. To find out more about Kodiak's opportunities and risks, you're invited to check out The Motley Fool's premium research report on the company, which comes with a full year of updates and analysis as key news breaks. To get started simply click here now.

The article Are Investors Missing Something With This Company? originally appeared on Fool.com.

Fool contributor Matt DiLallo has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.