Is Eaton Stock Destined for Greatness?

Editor's Note: Eaton has denied any planned sale of its auto-parts business, which was not known at the time this article was written. The Fool regrets the error.

Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does Eaton fit the bill? Let's take a look at what its recent results tell us about its potential for future gains.

What we're looking for

The graphs you're about to see tell Eaton's story, and we'll be grading the quality of that story in several ways:

Growth: are profits, margins, and free cash flow all increasing?

Valuation: is share price growing in line with earnings per share?

Opportunities: is return on equity increasing while debt to equity declines?

Dividends: are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's take a look at Eaton's key statistics:

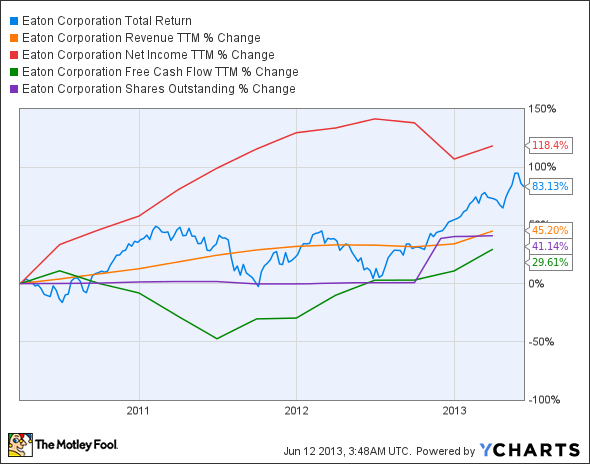

ETN Total Return Price data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 45.2% | Pass |

Improving profit margin | 42.5% | Pass |

Free cash flow growth > Net income growth | 29.6% vs. 118.4% | Fail |

Improving EPS | 94.6% | Pass |

Stock growth (+ 15%) < EPS growth | 83.1% vs. 94.6% | Pass |

Source: YCharts.

*Period begins at end of Q1 2010.

ETN Return on Equity data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 33.1% | Pass |

Declining debt to equity | 29.6% | Fail |

Dividend growth > 25% | 68% | Pass |

Free cash flow payout ratio < 50% | 46.3% | Pass |

Source: YCharts.

*Period begins at end of Q1 2010.

How we got here and where we're going

Eaton crosses the finish line with a strong showing, missing out on only two of its nine possible passing grades. The only real cause for apparent concern is the surge in Eaton's net income relative to free cash flow, but on a nominal basis these two results are nearly neck and neck. The market clearly believes that Eaton has long-term potential, but will it be able to maintain (or improve) this pace the next time we look at it? Let's dig into the possibilities.

Eaton's been moving higher all year, but this is just the continuation of a longer bullish trend that's followed the company's efforts to both deepen and broaden its reach. A $12 billion acquisition last year put Eaton in direct competition with Emerson Electric and ABB in energy infrastructure. That acquisition provided a double benefit for Eaton's bottom line, as the acquired Cooper Industries provided a low-tax domicile in Ireland that's projected to save Eaton many millions each year. Every advantage counts, as Eaton has to contend with super-conglomerateGeneral Electric in several of its most important segments. Eaton and ABB are also both at risk of disruptive innovation from electrical integration systems that could replace several green-car charging components in one fell swoop.

Another potential spark for growth could be Eaton's auto-parts business, which is purportedly on the block. That wouldn't affect Eaton's truck-parts business, which has a major powertrain development deal with Cummins , and which still accounts for more of Eaton's revenue than the auto segment. Reducing its exposure to cyclical industries would improve Eaton's standing in the eyes of many investors, and the cash haul (estimated at $1 billion) from the sale could go toward paying off debt or buying a business more in line with the current electrical focus.

Putting the pieces together

Today, Eaton has many of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

For GE, the recent financial crisis struck a blow, but management took advantage of the market's dip to make strategic bets in energy. If you're a GE investor, you need to understand how these bets could drive this company to become the world's infrastructure leader. At the same time, you need to be aware of the threats to GE's portfolio. To help, we're offering comprehensive coverage for investors in a premium report on General Electric, in which our industrials analyst breaks down GE's multiple businesses. You'll find reasons to buy or sell GE today. To get started, click here now.

Keep track of Eaton by adding it to your free stock Watchlist.

The article Is Eaton Stock Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter, @TMFBiggles, for more insight into markets, history, and technology.The Motley Fool recommends Cummins and Emerson Electric and owns shares of Cummins and General Electric Company. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.