Salesforce Stock Is Going Nowhere. Here's Why.

In a buoyant, bullish stock market, it's been pretty strange to watch how the tech-heavy Nasdaq Composite Index has underperformed the Dow Jones Industrial Average by more than a full percentage point since the year began. One tech stock in particular that's been failing to pull its weight is salesforce.com , whose stock has lost a percentage point's worth of market cap since early January. But why?

Three reasons.

Salesforce stock is all bark ...

When you stack up Salesforce stock against two of its larger, incumbent rivals in database software -- SAP and Oracle -- there's plenty of reason to expect the former to outperform the latter. For example, according to the smart folks at finviz.com, who keep track of these kinds of things, Salesforce boasts a better record of sales growth than either of its rivals:

With a historical sales-growth rate more than twice that of Oracle, and more than three times SAP's plodding pace of 9.6% growth, Salesforce stock should be running away from its rivals. And it is ... sort of. Both Oracle and SAP shares are down more than Salesforce since the year began, so Salesforce is outperforming the competition -- yet the stock's still not growing by the leaps and bounds that you might expect a 32% growth rate to produce.

Salesforce stock is also expected to turn in stronger earnings growth than either SAP or Oracle over the next five years:

Yet once again, despite its boasting both strong past performance and strong future prospects, investors continue to treat Salesforce stock like a dog with fleas.

... but no bite

So the question again is "why?"

If you ask me, there's one key problem with Salesforce, and it's the reason the stock isn't performing as well as you might expect a company with these kinds of numbers to its credit would perform. That reason is free cash flow -- or rather, the near lack thereof.

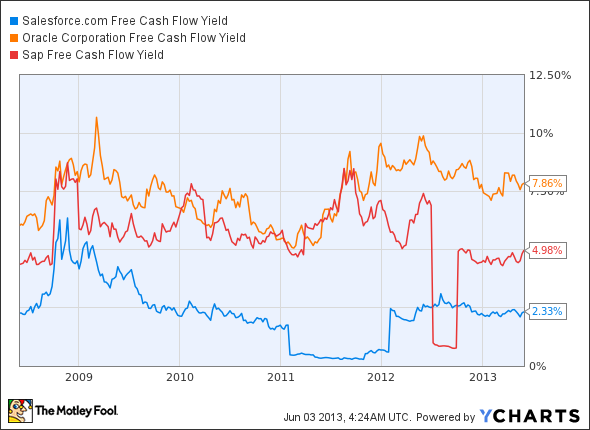

Take a lookcat how these three companies stack up in the race to turn GAAP sales and profits into real, cold, hard cash, relative to their market caps (a concept known as free cash flow yield):

CRM Free Cash Flow Yield data by YCharts

What you see here is that of the three main companies competing in the database software sphere, Salesforce is the least successful in terms of generating real cash profit from its business. When you pair that with Salesforce stock's high valuation relative to the cash it produces -- at a price-to-free cash flow ratio of 40.2, it's the most expensive stock on the list by a factor of 2 -- it's not hard to see why investors are shunning Salesforce stock.

Foolish final point

One last observation I'd like to make, and then I'll let you go. One way you can quickly "quality" check a company's earnings -- before you even get down to crunching free cash flow yield -- is to check and see whether the company makes enough cash profit that it can write its shareholders a quarterly dividend check and be sure it won't bounce.

Both Oracle and SAP can write dividend checks, and in fact they do pay their shareholders a dividend -- 0.7% for Oracle, and a full 1.1% for SAP. That's something Salesforce.com can't claim, and it's one final reason to stay away from Salesforce stock.

If you're looking for some better long-term, dividend-paying investing ideas, you're invited to check out The Motley Fool's brand-new special report "The 3 Dow Stocks Dividend Investors Need." It's absolutely free, so simply click here now and get your copy today.

The article Salesforce Stock Is Going Nowhere. Here's Why. originally appeared on Fool.com.

Fool contributor Rich Smith has no position in any stocks mentioned. The Motley Fool recommends salesforce.com and owns shares of Oracle. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.