The 1 Indicator That Banks Will Soon Outperform

Eventually, and possibly soon, the Federal Reserve will begin unwinding the cheap money and loose monetary policy it put in place in the wake of the financial crisis.

While it can be a fool's errand to try to time the market, you may be able to see this policy change coming by keeping an eye on the bond market. As economic prospects improve, bond investors will start to anticipate the Fed's policy change, and investors who are tuned in to the right places will get tipped off to the coming banking tailwind.

Why is the bond market our indicator?

Bonds and securitized loans make up approximately 50% of the world's total global financial assets, according to McKinsey & Company. The global bond market is a mind-boggling $113 trillion pool of assets from private companies, public companies, governments, and nonprofits around the world. For comparison, the entirety of the Federal Reserve's stimulus programs since 2007 -- an addition of more than $2.5 trillion to its balance sheet -- represents just 2.2% of this sum.

Because of their sheer size, the bond markets are collectively a powerful indicator of sentiment on the state of the U.S. and world economies. Today, bond yields are at historic lows, making bond prices very high. This situation reflects the market's current expectation of a continued low-rate, highly liquid monetary policy. At the first indication of a self-reinforcing recovery, the large, institutional market movers in the bond market will anticipate the change in the Fed's policy and begin moving money into other asset classes, causing yields to rise as prices decline.

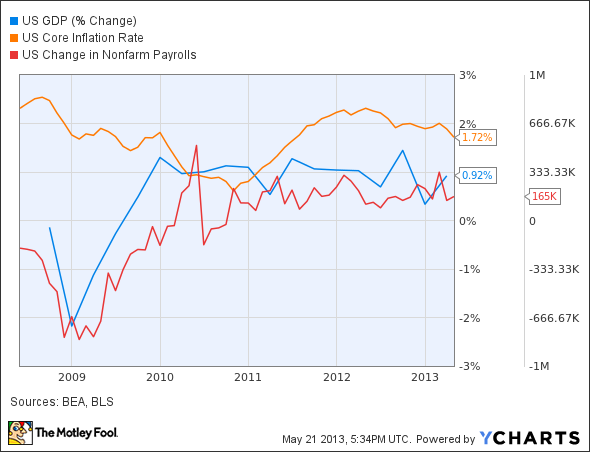

Right now, GDP is steady, employment gains are consistent and positive, and inflation remains in check. As the uncertainty from the fiscal cliff and sequester continues to recede, it's reasonable to expect these trends to continue, and likely improve, pushing the Fed closer to unwinding.

The 3 reasons banks are well positioned to outperform

The end of QE is fundamentally good. It means that the economy is doing well, more people are finding jobs, and businesses are growing again. And as the economy finds its footing, the banks are uniquely positioned to capitalize on both business and consumer growth. Here's why.

1. The end of QE is a vote of confidence in the financial system

Before it removes itself from the markets, the Fed must first be confident that the global financial system is stable enough to avoid another 2008-style crisis. The end of QE would implicitly acknowledge that the banks are healthy, capital is sufficient, and global liquidity needs can be met through traditional channels.

In this event, investors will reassess the risk/reward equation of an equity stake in banks. In general, banks today have market caps below book value. The markets aren't certain about these banks' asset quality, or the stability of the financial system, so they essentially discount the value of these banks' holdings. When confidence returns, expect market caps to rise closer to book value across the board, particularly at banks such as Bank of America(0.67 price-to-book) and Citigroup (0.83 price-to-book).

2. Businesses, large and small, will be growing

To grow, a business needs money to fund additional inventory, expand its facilities, hire more employees, and/or buy equipment to improve productivity. This type of business lending is the bread and butter of banks large and small. Two banks ready to capitalize on broad business growth particularly stand out, one for its strong corporate business unit and the other for its best in class small business programs.

JPMorgan Chase is a leading U.S. provider of corporate banking services for businesses. The company's corporate and investment banking unit, which serves larger clients with more sophisticated banking needs, reported profits in excess of $2.6 billion for the quarter, an increase of more than $500 million year over year.

Wells Fargo was the top small-business lender in the U.S. for 2012, based on Community Reinvestment Act data. Wells is also the leading originator of loans under the Small Business Association's 7a program, originating $456 million of new loans to small businesses year to date in 2013.

When the Fed begins phasing out QE, growth will be stronger and more resilient for businesses across the board. Loan demand will be greater, and as a result, banks will increase growth and earnings.

3. The employment market will drive strong consumer demand

As unemployment improves, consumers have more money to spend, an increased ability to save and invest, and a stable cash flow to obtain and repay loans.

Banks' mortgage arms will benefit most from this greater strength, but so will secondary businesses in wealth management, credit cards, auto loans, and deposit products. In particular, expect Wells Fargo and JPMorgan to cash in here.

Wells is the nation's largest mortgage lender, with JPMorgan second. Despite mixed mortgage results in Q1 at the big banks, encouraging data in real estate prices and new home starts will should continue to strengthen the broad market and mortgage divisions across the board.

Wells and JPMorgan are both well positioned to take advantage of secondary consumer banking needs. JPMorgan has the nation's largest ATM network and the second-largest branch network, and it originated more credit cards in Q1 than any other bank.

Wells is the industry's gold standard for cross-selling products, with the average retail customer using more than six different products. Wells has also invested heavily in recent years to build its wealth-management business. The company reports that it is the third-largest wealth manager based on number of financial advisors, and No. 4 based on assets under management. This investment in infrastructure yielded a 16% year-over-year increase in managed accounts for Q1, which contributed to Wells' 12% increase in trust and investment fee income.

Look to the bond yields

If the economy continues to progress on its current trend, then rising rates in the bond market will indicate broad market agreement that the economy has become self-reinforcing. When that happens, expect banks to benefit, and invest accordingly.

With big finance firms still trading at deep discounts to their historic norms, investors everywhere are wondering if this is the new normal, or if finance stocks are a screaming buy today. The answer depends on the company, so to help figure out whether JPMorgan is a buy today, check out The Motley Fool's premium research report on the company. Click here now for instant access!

The article The 1 Indicator That Banks Will Soon Outperform originally appeared on Fool.com.

Fool contributor Jay Jenkins has no position in any stocks mentioned. The Motley Fool recommends Wells Fargo and owns shares of Bank of America, JPMorgan Chase, and Wells Fargo. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.