General Dynamics Stock Looks Ripe for Repurchase

Faced with the prospects of slowing revenues and declining profits for the foreseeable future, defense contractor Northrop Grumman recently announced a plan to boost its earnings -- by buying back its own stock. But Northrop's hardly the only defense contractor facing a tough spending environment. And this raises the question: Could General Dynamics stock be next in line for a big buyback?

Where Northrop treads...

Northrop upped its planned stock buyback program to $5 billion, effectively assuring investors that even if its earnings as a company should decline, it can still make its earnings per share grow.

How? Well, assume that Northrop earns (hypothetically) $1 million and divides this profit among (still hypothetically) 1 million shares. This results in $1 profit for each Northrop share outstanding. But if you shrink the share count to 750,000 -- on the same $1 million, firmwide profit -- then each remaining share owns $1.33 of the profits. Presto change-o -- Northrop produces 33% profits growth!

... should General Dynamics follow?

In Northrop's case, this makes sense. Analysts think Northrop's profits will decline by about 2.6% on average over the next five years. But a 33% boost to per-share earnings could cancel out these declines and even get Northrop growing again.

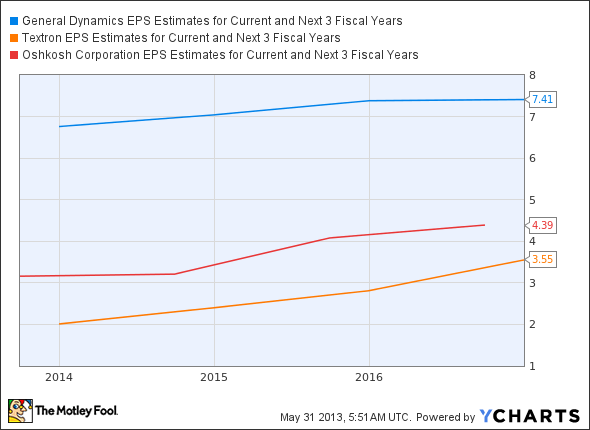

In the case of General Dynamics stock, though, a big buyback could do even more good. Right now, you see, General Dynamics shares are expected to earn more than peer armored vehicle manufacturers:

GD EPS Estimates for Current and Next 3 Fiscal Years data by YCharts.

And yet, this picture isn't really as pretty as it looks, because if General Dynamics stock earns more per share than its peers, it also carries a higher price per share.

Don't get me wrong -- on a forward earnings basis, General Dynamics stock is still cheaper (11.1 times earnings) than either Textron at 11.4 times earnings or Oshkosh at 12.2 times earnings. That being said, General Dynamics stock isn't quite as great a bargain relative to its rivals as first meets the eye. But a big stock buyback could change that equation.

General Dynamics can and should follow Northrop's example

General Dynamics is also in a better position -- financially -- to fund a big stock buyback. Of the three big armored vehicle manufacturers, GD has the least net debt on its balance sheet. Oshkosh's balance sheet shows a bit more than $500 million more debt than cash, while Textron has more than $3 billion more debt than cash in the bank.

General Dynamics stock, in contrast, shows a net cash deficit of only $170 million.

Cash is king

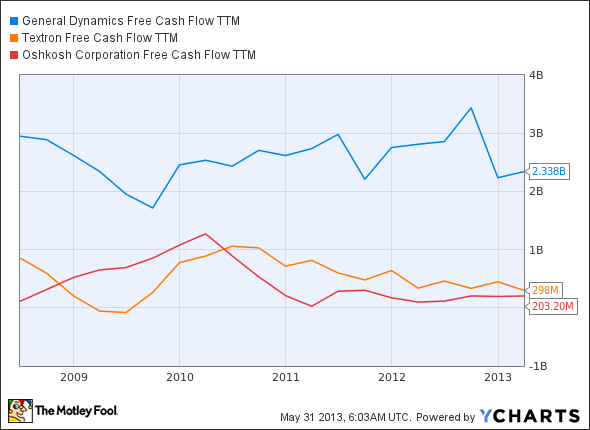

GD is also doing the best job of these three companies at generating cash from its business -- cash that can be used to pay a big dividend, to pay off debt, and yes -- to do a big buyback. Again, putting things in perspective:

GD Free Cash Flow TTM data by YCharts.

Foolish takeaway

As it turns out, of course, General Dynamics is buying back stock. In fact, just last month the company confirmed that it repurchased 1 million shares in Q1. But it can do better. Ample free cash flow and a robust balance sheet -- plus modest growth prospects that could benefit from a boost to per-share earnings -- all argue in favor of upping the tempo of General Dynamics' stock repurchases.

It's time to buy back some (more) General Dynamics stock.

The article General Dynamics Stock Looks Ripe for Repurchase originally appeared on Fool.com.

Fool contributor Rich Smith has no position in any stocks mentioned. The Motley Fool owns shares of General Dynamics, Northrop Grumman, and Textron. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.