Bernanke's Boogeyman: The Japan Scenario

On the back of yesterday's drop, U.S. stocks opened up this morning, with the and the narrower, price-weighted gaining 0.49% and 0.38%, respectively, by 10:05 a.m. EDT.

The , Japan's most widely known stock index, fell by more 5% today. Last Thursday, it dropped 7.3%. This is nerve-racking for Japanese investors, but it should also give pause to Federal Reserve Chairman Ben Bernanke.

So far, the Fed's monetary alchemy, including its zero-interest-rate policy and repeated rounds of quantitative easing (i.e., bond-buying), has been a success, at least insofar as it has raised asset prices, whether it be bonds or equities (which was one of the Fed's explicit goals). The following chart shows the performance of both asset classes beginning on Dec. 17, 2008, the day after the central bank lowered the federal funds rate to between 0% and 0.25%:

Perhaps emboldened by the Fed's success, Japan has embarked on a similar program under the new leadership of Prime Minister Shinzo Abe. Last month, the Bank of Japan launched a massive new quantitative-easing plan with the aim of doubling the monetary base by the end of next year in order to permanently break the country's deflationary cycle.

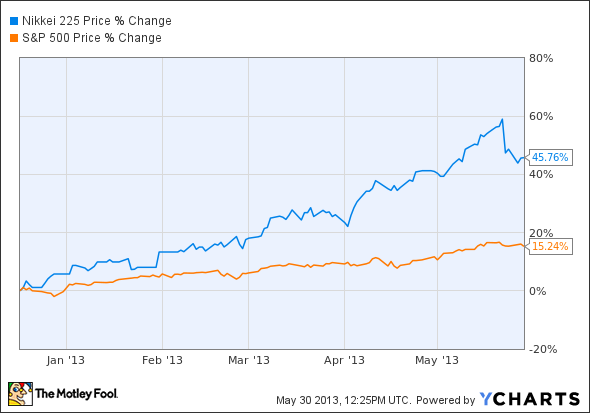

The effects have not been long in coming, and they are spectacular. The following chart shows the Nikkei 225's remarkable resurgence from Dec. 17, the day after the general election that swept Mr. Abe into office:

But while both countries have experienced strong appreciation in equity prices, there is one major difference between the policies' effects in the two countries. In the U.S., the Fed has managed to flatten volatility (the VIX Index , orange line, is a measure of investor expectations for 30-day volatility in the S&P 500):

In Japan, however, the volatility of interest rates and stocks has increased markedly. As mentioned above, we've witnessed two significant declines in the stock market in the past week. Meanwhile, according to a recent report from JPMorgan's Flows & Liquidity team, the 60-day standard deviation of daily changes in the 10-year Japanese Government Bond yield is now at its highest since 2008.

The U.S. and Japan are not identical environments for monetary experimentation: The U.S.' structural growth factors -- including its fiscal position, regulatory environment, and demographics -- are superior. All the same, while Bernanke's trip has been smooth so far, Japan is a reminder of the sort of speed bumps that could crop up once the Fed begins to raise rates and exit quantitative easing.

If you're ready to invest with a multiyear horizon, based on company fundamentals instead of macro headlines, The Motley Fool's chief investment officer has selected his No. 1 stock for the next year. Find out which stock it is in the brand-new free report "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

The article Bernanke's Boogeyman: The Japan Scenario originally appeared on Fool.com.

Fool contributor Alex Dumortier, CFA has no position in any stocks mentioned; you can follow him on LinkedIn. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.