Is Now the Time to Buy DuPont Stock?

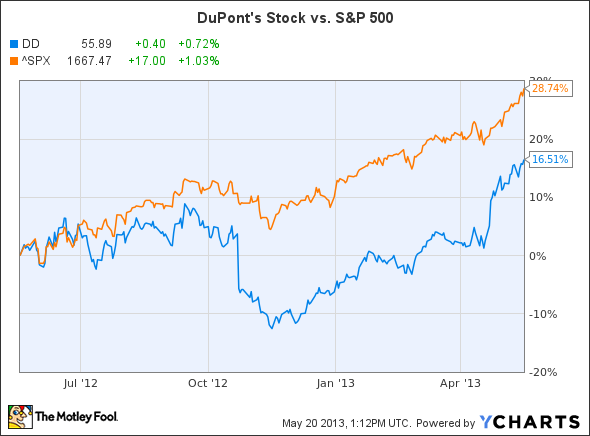

With a market that seems to hit new highs every day, it's getting tougher to find a good business trading at a fair price. One stock that i'm starting to look at is DuPont . Unfortunately, for me at least, so far this year the stock is up just over 24% while the S&P 500 is up about 17%. That's pretty good outperformance, though, if you look out over the past year you'll see a slightly different story:

So, while DuPont's stock has been strong of late, it has lagged the benchmark over the past year. In fact, it's lagged the average over the past five- and 10-year periods as well. Strong past price appreciation can mean business is booming, while a lagging stock price usually means a company has fallen out of favor with investors. Sometimes it can stay out of favor for too long, as investors miss the fact that its business is turning around, which is usually a good opportunity to find a company trading at a compelling price. Let's take a deeper look at DuPont to determine if that's the case.

DuPont has been enhancing its portfolio to pursue growth opportunities that create higher value. That transition has seen the company add Danisco, a global enzyme and specialty food ingredients company, to its portfolio while jettisoning its performance coatings business. Through this transition DuPont has become more focused on science and innovation, which yields higher margins, while exiting a lower-margin commodity business like performance coatings.

This is part of a transition that has the company maximizing its business portfolio around its purpose to be a science company. DuPont's strategy is to build and leverage its science lead in three specific focus areas: agriculture and nutrition, bio-based industrials, and advanced materials. That focus on science and development is starting to bear fruit as you can see in the slide below:

Source: DuPont Investor Presentation

While DuPont has built a diversified business around its three focus areas, it still faces stiff competition. For example its agriculture business, which focuses on seeds, traits, and crop protection puts it up against the likes of Monsanto and Dow Chemical . That competition with Monsanto cost the company a lot of money in legal fees and ended with DuPont agreeing to a $1.75 billion licensing deal with the seed giant. The good news, though, is that now instead of competing against Monsanto, the two will be collaborating as DuPont gains access to some key patents in Monsanto's portfolio.

Despite that monetary loss, DuPont has a vast intellectual property portfolio which provides it with a strong base for future growth. To that end, DuPont has set long-term-growth targets to grow its sales by 7% each year while its operating earnings are expected to grow by a 12% annual clip. That's pretty solid growth and shows how well the company is at turning its innovation into returns.

That being said, if there is a problem with DuPont, it's with the company's stock price. With a price to earnings ratio of around 20 times, it's hard to call the company a value stock as investors are paying nearly twice the earnings growth rate for the company. While it's trading at a cheaper valuation than Dow Chemical for example, analysts expect Dow's earnings to grow much faster over the next two years. Further, Dow's stock pays a higher dividend, which is likely headed even higher in the future.

I like that DuPont has a solid foundation for growth, however, I just don't see a compelling reason to buy its stock at today's price. For it to really beat the market going forward the company will need to exceed its earnings growth targets. Otherwise, the stock price is just too high in my opinion to make it a compelling buy.

On the other hand, and sticking with the agriculture theme, one company that just might be a compelling buy is fertilizer producer PotashCorp. With less and less arable land available around the world, increasing yields from existing plots could become vitally important to keeping up with expected population growth. Cheap and effective fertilizers could be the key to achieving this goal. As the global leader in potash production, PotashCorp has established several barriers to entry that make it nearly impossible for competition to break through. Click here now to access The Motley Fool's premium research report that covers precisely what these barriers to entry are and details several other key reasons why PotashCorp presents such a compelling investment opportunity today.

The article Is Now the Time to Buy DuPont Stock? originally appeared on Fool.com.

Motley Fool contributor Matt DiLallo has the following options: Long Jan 2015 $70 Calls on Monsanto, Short Jan 2015 $70 Puts on Monsanto, and Short Jul 2013 $95 Calls on Monsanto. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.