Should Boeing Shrink Its Stock?

Faced with the prospects of slowing revenues and declining profits for the foreseeable future, defense contractor Northrop Grumman has announced a plan to boost its earnings dramatically -- by buying back its own stock. But Northrop's hardly the only defense contractor facing a tough spending environment. And this raises the question: Could Boeing stock be next in line for a big buyback?

What Northrop did

In a bold move, Northrop upped its planned stock buyback program to $5 billion last week, in effect declaring to Wall Street that even if earnings decline, the company will shrink its share count by 25% and forceits per-share earnings to grow.

How? Simple math tells you that if Northrop earns (hypothetically) $1 million and divides this profit among (still hypothetically) 1 million shares, this results in $1 per share in profit. But if you shrink the share count to 750,000 -- on the same $1 million, firmwide profit -- then each remaining share can lay claim to $1.33 of the profits. Presto change-o -- Northrop produces 33% profits growth!

Why Northrop did it

In Northrop's case, this makes sense. Analysts think Northrop's profits will decline by about 2.6% on average over the next five years. But a 33% boost to per-share earnings could cancel out these declines, and even get Northrop growing again.

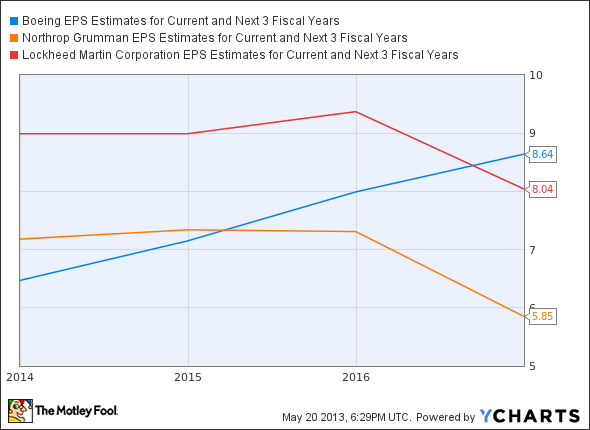

In the case of Boeing stock, a big buyback could do even more good, turbocharging earnings growth that -- at 14% estimated over the next five years -- already outclasses its rivals in the defense sector:

BA EPS Estimates for Current and Next 3 Fiscal Years data by YCharts.

Why Northrop can do it

Northrop's plan to buy back $5 billion in shares over the next three years hinges upon its ability to come up with enough cash to fund the buyback. With $2.45 billion in annual cash profits, it's got more than enough cash for the purpose.

But if Northrop can do a buyback with $2.45 billion in free cash flow, the case for buying back Boeing stock looks even stronger. Again, putting things in perspective here:

BA Free Cash Flow TTM data by YCharts.

First things first

If there's one argument to be made against Northrop doing a big buyback, it's that the contractor already has a big slug of debt on its books and probably should think about paying that down. In contrast, Boeing stock looks mighty fine in the debt department. Given its ample cash cushion, Boeing should have no problem putting its prodigious cash flows to work buying back Boeing stock:

Foolish takeaway

As it turns out, of course, Boeing is buying back stock. Back in December, it announced plans to resume stock repurchases that it suspended in 2009. But with only $3.6 billion in the buyback kitty, management's plans for Boeing stock are both smaller absolutely and much smaller in scope relative to the company's market cap, than the buyback that Northrop envisions.

Given Boeing's superior financials, management should jump at the chance to turbocharge growth with a big buyback announcement. It's time to buy back some Boeing stock.

Boeing operates as a major player in a multitrillion-dollar market in which the opportunities and responsibilities are absolutely massive. However, emerging competitors and the company's execution problems have investors wondering whether Boeing will live up to its shareholder responsibilities. In our premium research report on the company, two of The Motley Fool's best minds on industrials have collaborated to provide investors with the key, must-know issues surrounding Boeing. They'll be updating the report as key news hits, so don't miss out -- simply click here now to claim your copy today.

The article Should Boeing Shrink Its Stock? originally appeared on Fool.com.

Fool contributor Rich Smith has no position in any stocks mentioned. The Motley Fool owns shares of Northrop Grumman. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.