A Disastrous Deal and the End of Cheap Oil

On this day in economic and business history...

"Heralding a new era for industry worldwide, Daimler-Benz AG said it will merge with Chrysler. in a $38 billion deal," read the first sentence of a CNNMoney article about the merger, announced on May 7, 1998, that stunned the auto world. The hyperbole flew fast and furiously around the proposed DaimlerChrysler. Daimler CEO Juergen Schrempp said the two companies would "create the world's leading automotive company for the 21st century ... combining the two most innovative car companies in the world."

For Daimler, the move offered a way to make greater inroads to the lucrative American market. For Chrysler, the prospect of taking on the much stronger Ford and General Motors in Europe was tremendously enhanced by Daimler's home-field advantage. It was at the time the largest industrial merger in history, although the combined company would still be only the fifth-largest automaker in the world, behind both Ford and GM. When combined, the two companies had more than 440,000 employees and a market capitalization nearing $100 billion.

The deal became a fiasco faster than anyone could have expected. Some German executives openly scorned Chrysler vehicles, and some (rightly) offended Chrysler execs shot back with barbs of their own. The "merger of equals" became an example of domineering German management railroading American executives with directive after directive, so straining relations between the two halves of DaimlerChrysler that most of the Americans were replaced by a German management team within two and a half years. By that point DaimlerChrysler's stock had shed half its value. The Chrysler brand took a lot of damage in the process: Its earnings dropped by 20%, returning the former cash-bleeder to deep red territory. A duplicitous campaign by the Germans to present the deal as a "merger of equals," despite their intentions to subsume Chrysler beneath Daimler leadership, led to investor lawsuits when it came to light.

DaimlerChrysler stood for nine years. In the summer of 2007, Daimler sold Chrysler to private-equity firm Cerberus Capital, although it retained a minority stake. This lasted until 2009, when a diminished and dented Chrysler filed for bankruptcy and wiped out its shareholders. By that point, only General Motors was one of the world's top three automakers; Ford was firmly ensconced in fourth place, and neither Daimler nor Chrysler made it into the top 10. The merger had damaged both companies to a greater extent than anyone could have expected.

The price of oil isn't high enough

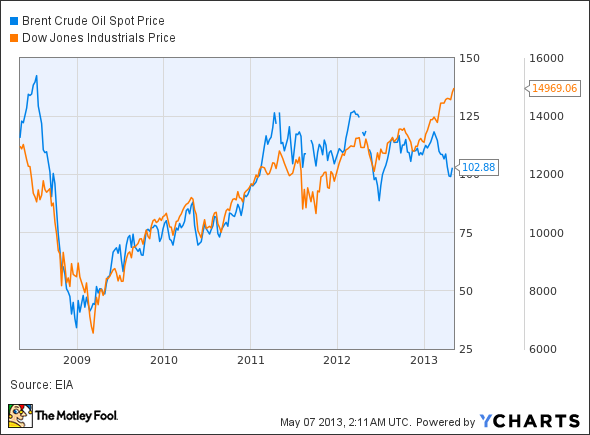

Goldman Sachs energy analyst Argun Murti doubled down on predicting a "super spike" in the price of oil, which he claimed would surpass $200 per barrel within two years, on May 7, 2008. At the time, it seemed that he might be right; the price had soared past $100 per barrel earlier that year, and for the five years preceding his prediction, both oil prices and the Dow Jones Industrial Average had marched steadily higher.

Brent Crude Oil Spot Price data by YCharts.

Murti had made headlines before, most notably for predicting in 2005 that oil prices would reach $100 per barrel. There seemed no stopping oil's wild rise, which had made a barrel 400% costlier in the spring of 2008 than it had been just five years earlier. The New York Times devoted a feature to Murti's call two weeks later, in which it pointed out:

Mr. Murti, 39, argues that the world's seemingly unquenchable thirst for oil means prices will keep rising from here and stay above $100 into 2011. Others disagree, arguing that prices could abruptly tumble if speculators in the market rush for the exits. But the grim calculus of Mr. Murti's prediction, issued in March and reconfirmed two weeks ago, is enough to give anyone pause: in an America of $200 oil, gasoline could cost more than $6 a gallon.

Of course, there remained substantial disagreement over where oil prices would ultimately end up. Few analysts foresaw the looming financial crisis, which crushed everything -- the Dow, oil, commodities, real estate, and more. The five years following Murti's astronomical prediction undermined his credibility: After peaking near $150 per barrel in the summer, oil prices paced the Dow's collapse through the fall and into 2009, but they also followed the Dow's rebound afterwards. Each period bears remarkable similarity in movement, as you can see here:

Brent Crude Oil Spot Price data by YCharts.

Murti's employer didn't seem to mind the ultimate inaccuracy of his 2008 prediction. Goldman Sachs made him the co-head of its research division in early 2011, when the price of a barrel of oil held at about $90. In this position, Murti steered Goldman away from huge price predictions as the organization shifted to predicting an end to the oil super-cycle and a return to long-term market stability toward the end of 2012.

If you're on the lookout for some currently intriguing energy plays, check out The Motley Fool's "3 Stocks for $100 Oil." For free access to this special report, simply click here now.

The article A Disastrous Deal and the End of Cheap Oil originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more insight into markets, history, and technology.The Motley Fool recommends Ford, General Motors, and Goldman Sachs. The Motley Fool owns shares of Ford. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.