TTM Technologies Shows Its Cyclical Side Again

TTM Technologies makes the circuit boards in your favorite electronics. The company dips into every market from smartphones and tablets, to enterprise-class networking gear, to military hardware. You need a high-quality board done fast? TTM is there. On an anecdotal level, you'd think a company like this should be swimming in money. I mean, take a look around you and count the electronic gadgets. This stuff is everywhere.

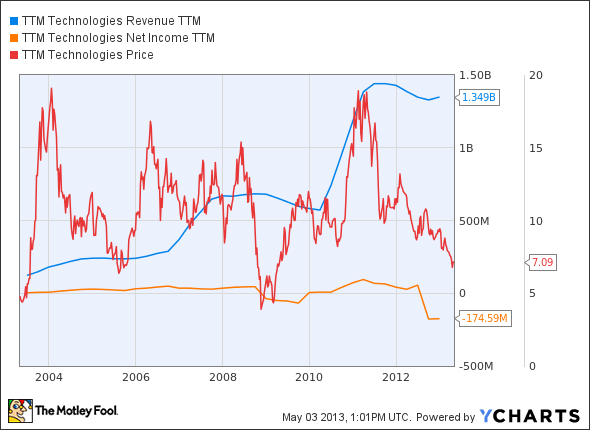

But somehow, TTM never got that memo. The company has resorted to growth by acquisition in recent years. Profit margins are both slim and unstable. The stock is a neurotic mess, and in most cases dead money even for very patient shareholders.

TTMI Revenue TTM data by YCharts.

The company reported first-quarter results last night. Sales increased 8% year-over-year to $325 million, led by strong revenue in the cell phone and networking markets but held back by soft sales to builders of computer systems. Non-GAAP earnings fell 43% to $0.13 per share. Adjusted net margins dwindled to 3.3%, down from 6.2% a year ago.

Wall Street analysts were looking for earnings around $0.09 per share on $320 million in sales, so these results crushed the Street's estimates by a fair margin. But enthusiasm over the beat is tempered by a modest outlook for the coming quarter, where only the very top of management's guidance ranges match the average analyst estimates.

On the earnings call, TTM's leaders discussed signs of recovery in the networking market. Large customers there have started placing orders with longer lead times again, and that's a trend break from several years of shortening order leads. CEO Kent Alder said that "there is overall a tone of more optimism" and "customers are getting a little more confident about the future."

TTM's largest networking customers include Juniper Networks and Cisco Systems, which gives the board maker some unique perspective on the networking market. Both Cisco and Juniper could use a boost these days, as network upgrades have been slow on a global level over the last five years. Alder pointed to 4G LTE network installations as a potential driver of fresh growth in the second half of 2013 and onward.

So TTM remains as cyclical as ever. Share prices jumped 17% in early Friday trading as investors focused on long-term optimism and a proven earnings beat rather than the gloomy next-quarter guidance. Even so, share prices remain firmly in the middle of TTM's 52-week range. I'm starting to think that this stock is better suited for momentum investors and cyclical traders, and best left alone by long-term buy-and-hold owners. My own long-term bullish CAPScall on the stock is up for review the next time I catch TTM exploring 52-week highs.

It's incredible to think just how much of our digital and technological lives are almost entirely shaped and molded by just a handful of companies. Find out "Who Will Win the War Between the 5 Biggest Tech Stocks?" in The Motley Fool's latest free report, which details the knock-down, drag-out battle being waged by the five kings of tech. Click here to keep reading.

The article TTM Technologies Shows Its Cyclical Side Again originally appeared on Fool.com.

Fool contributor Anders Bylund holds no position in any company mentioned. Check out Anders' bio and holdings or follow him on Twitter and Google+. The Motley Fool owns shares of Cisco Systems. Motley Fool newsletter services have recommended buying shares of TTM Technologies. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.