Is Textainer's Stock Destined for Greatness?

Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does Textainer fit the bill? Let's take a look at what its recent results tell us about its potential for future gains.

What we're looking for

The graphs you're about to see tell Textainer's story, and we'll be grading the quality of that story in several ways:

Growth: Are profits, margins, and free cash flow all increasing?

Valuation: Is share price growing in line with earnings per share?

Opportunities: Is return on equity increasing while debt to equity declines?

Dividends: Are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's take a look at Textainer's key statistics:

Source: TGH Total Return Price data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 103.8% | Pass |

Improving profit margin | 29.4% | Pass |

Free cash flow growth > Net income growth | (1,752.8%) vs. 128% | Fail |

Improving EPS | 109.4% | Pass |

Stock growth (+ 15%) < EPS growth | 163.4% vs. 109.4% | Fail |

Source: YCharts. * Period begins at end of Q4 2009.

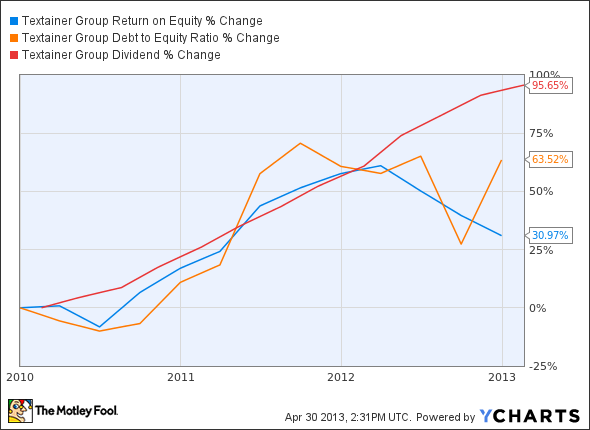

Source: TGH Return on Equity data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 31% | Pass |

Declining debt to equity | 63.5% | Fail |

Dividend growth > 25% | 95.7% | Pass |

Free cash flow payout ratio < 50% | Negatice FCF | Fail |

Source: YCharts. * Period begins at end of Q4 2009.

How we got here and where we're going

Textainer pulls together a reasonable five out of nine passing grades, but its score is definitely hindered by plummeting free cash flow. Building out a big inventory of shipping containers isn't cheap, and Textainer has 1.9 million of them at last count, but at some point investors would probably like to see growth driven by positive cash flow rather than more debt issuance. Can Textainer pull itself out of that cash flow hole? Let's dig a little deeper.

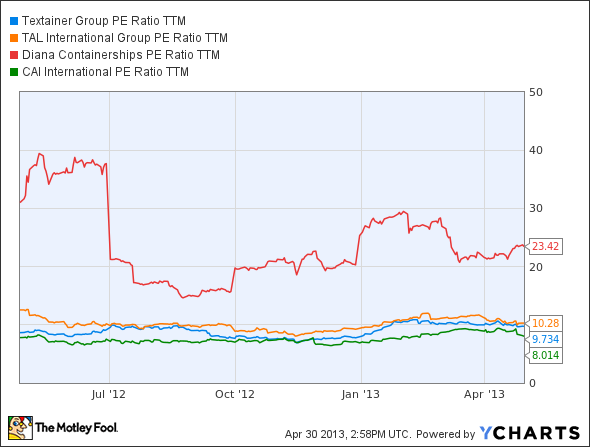

Texatainer's business model, thankfully, has allowed it to avoid the brutal decline suffered in dry bulk shipping, which has devastated investors in a number of companies. However, Textainer stacks up more fairly against a number of its intermodal container peers, particularly TAL International and CAI International , which have both held to roughly similar P/E ratios in recent months:

Source: TGH P/E Ratio TTM data by YCharts.

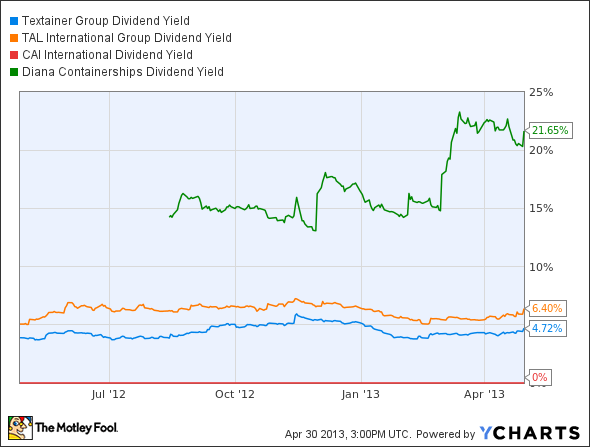

Diana Containerships is the odd stock out here, but there's a reason for that -- its dividend yield is one of the absolute highest you can find on the market:

Source: TGH Dividend Yield data by YCharts.

So what makes Textainer stand out against its peers? Well, let's look at some other metrics to figure out just what's going on and whether this company really is the stand-out best investment in intermodal container shipping:

Company | One-Year Total Return | Operating Margin | Debt to Equity |

|---|---|---|---|

Textainer | 15.8% | 57.2% | 2.2 |

TAL International | 5.5% | 53.9% | 4.3 |

CAI International | 23.4% | 58.1% | 2.9 |

Diana Containerships | 9.8% | 15.8% | 0.4 |

Source: YCharts.

As you can see, there's nothing particularly noteworthy about Textainer over its peers. Even on the basis of revenue growth, Textainer doesn't prove its indisputable superiority (Diana Containerships is omitted from the following graph due to less available financial history):

Source: TGH Revenue TTM data by YCharts.

However, it's important to note that a totality of factors does tip the scales slightly in Textainer's favor. It is the world's largest intermodal container company, so it has scale in its favor. It doesn't have the largest yield, but it does have a lower debt-to-equity ratio than TAL and a much better operating margin than Diana Containerships. Is that enough to push you away from other shipping stocks? It shouldn't be -- but Textainer should be one of the first on your list.

Putting the pieces together

Today, Textainer has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

The Motley Fool's chief investment officer has selected his No. 1 stock for the next year. Find out which stock it is in the brand-new free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

The article Is Textainer's Stock Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more insight into markets, history, and technology.The Motley Fool recommends Textainer Group. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.