Is Illumina's Stock Destined for Greatness?

Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does Illumina fit the bill? Let's take a look at what its recent results tell us about its potential for future gains.

What we're looking for

The graphs you're about to see tell Illumina's story, and we'll be grading the quality of that story in several ways:

Growth: Are profits, margins, and free cash flow all increasing?

Valuation: Is share price growing in line with earnings per share?

Opportunities: Is return on equity increasing while debt to equity declines?

Dividends: Are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's take a look at Illumina's key statistics:

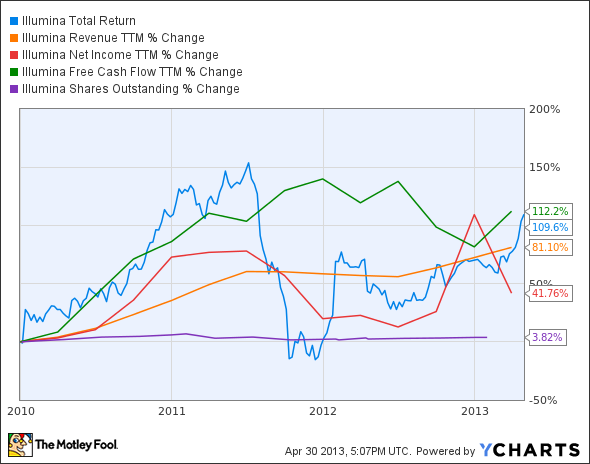

ILMN Total Return Price data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 81.1% | Pass |

Improving profit margin | (205.3%) | Fail |

Free cash flow growth > Net income growth | 112.2% vs. 41.8% | Pass |

Improving EPS | 41.7% | Pass |

Stock growth (+ 15%) < EPS growth | 109.6% vs. 41.7% | Fail |

Source: YCharts. *Period begins at end of Q4 2009.

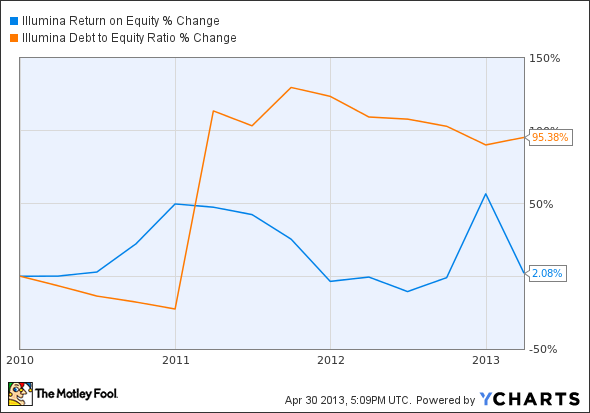

ILMN Return on Equity data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 2.1% | Pass |

Declining debt to equity | 95.4% | Fail |

Source: YCharts. *Period begins at end of Q4 2009.

How we got here and where we're going

Illumina has made some solid strides forward, but its stock is starting to look a little pricey now that share prices have more than doubled the increase in EPS over the past three years. Four out of seven passing grades isn't bad, but over the long term we'd rather see sustainable growth instead of supercharged gains that don't accurately reflect the progress on the income statement. Illumina's profit margin took a dive in its latest quarter, which hinders its score, but what can the company do to bring earnings in line with its stock price? Let's dig into the challenges and opportunities ahead.

It's been only a few trading days since Illumina surged on a strong earnings report, showing that there's still plenty of life in the sequencing sector. However, competition is only bound to increase now that erstwhile rival Life Technologies has found its white knight in Thermo Fisher Scientific . I've been optimistic on Life Tech's prospects for some time -- you can read more about my opinions in an analyst debate I held with fellow Fools Travis Hoium and Sean Williams last year -- and that opinion hasn't changed now that Life Tech has even deeper pockets to dip into for research dollars:

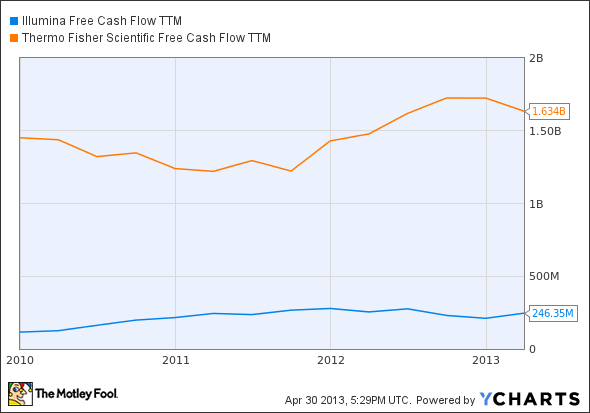

ILMN Free Cash Flow TTM data by YCharts.

While I'd never suggest that you can simply buy innovation, access to greater resources can be hugely impactful in the medical field. Life Tech and Illumina are already pushing the cost of sequencing a full genome down into the three-digit cost range, and when (not if) those costs approach comparable levels to blood work, you can expect to see doctors start making just as much use of genome screening as they do blood work, if not more. The market opportunity is effectively every human being alive with access to medical care, and the company that reaches a wide swath of doc offices first will have a very strong case for market dominance. Will Illumina race ahead of Life Tech when costs drop again? That remains to be seen.

However, Fool biotech expert Brian Orelli points out one big caveat: Once sequencing companies make these tests accessible, margins may collapse beyond the ability of volume sales to make up the difference. At least Illumina (and Life Tech) are in the driver's seat on margins, as it's unlikely that lesser-funded sequencing competitorsAffymetrix and Pacific Biosciences can muster the resources to push out sequencing at cost-effective scale before their peers.

For the time being, Illumina will have to go it alone -- there isn't likely to be a buyout white knight now that Life Tech has taken the big offer, and Roche has long since backed off its pursuit of Illumina over what it felt was too high a price. That might come back to haunt Illumina in the future, but we'll have to wait and see.

Putting the pieces together

Today, Illumina has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

While you can certainly make huge gains in biotech and pharmaceuticals, the best investing approach is to choose great companies and stick with them for the long term. The Motley Fool's free report "3 Stocks That Will Help You Retire Rich" names stocks that could help you build long-term wealth and retire well, along with some winning wealth-building strategies that every investor should be aware of. Click here now to keep reading.

Keep track of Illumina by adding it to your free stock watchlist.

The article Is Illumina's Stock Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more insight into markets, history, and technology.The Motley Fool recommends Illumina, Pacific Biosciences of California, and Thermo Fisher Scientific. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.